The Chinese word for crisis – 危机 – is made up of two characters: one meaning danger and the other opportunity. Regulatory changes in China over the past year and the subsequent equity downturn have prompted concerns that Chinese equities are simply too risky. We feel that it’s quite the reverse: Chinese equities today offer an excellent opportunity for full-cycle investors to build a more diversified portfolio.

In this blog, we’ll explore why long-term investors should re-examine their views on China and consider a dedicated allocation to Chinese equities.

Revisiting the China growth story

Before looking at the future, it’s worth revisiting how far the Chinese economy has come in just a few decades. Consider from 1979 to 2020:

- GDP per capita has increased by roughly 25 times1

- Approximately 850 million people have been lifted out of poverty2

- Life expectancy in China increased by more than 11 years3

China’s development over the past four decades ranks among the greatest economic achievements in human history. Even in just the last 10 years, the market capitalization of China’s stock and bond markets have both increased roughly four times over.4 Meanwhile, ongoing reforms have made these markets more liquid and accessible to foreign investors.

Why invest in Chinese equities?

Technological advancement

One of the most important long-term developments for China is the transition from an economy reliant on investment to becoming consumption led. Innovation and technology are key to this transition and are closely tied to China’s 2060 net-zero emissions goal. China is already the world leader in renewable energy production,5 second for its number of unicorn companies6 (private companies with a valuation over $1 billion) and is home to the largest e-commerce market in the world.7

China also has more science, technology, engineering and math (STEM) graduates each year than any other nation on Earth.8 This highly educated workforce, along with the scale of its economy, give China a significant edge in the development of the technologies of tomorrow.

Ongoing reforms

Reforms within China’s capital markets are helping to attract greater foreign investor flows (both index and active), which is helping to bring greater professionalism to China’s equity and fixed income markets. Global holdings of Chinese stocks and bonds have increased by roughly US$120 billion in the first three quarters of 2021 alone.9 Meanwhile, China’s new Beijing Stock Exchange started trading in November with 81 companies listed.10 The exchange is intended to help channel financing to small- and medium-sized companies, and further develop China’s technology sector.

Property and/or cash and deposits have functioned as the primary savings vehicles for China’s household assets.11 However, the maturation of China’s capital markets, ongoing reforms (such as the three-pillar pension reform) and policies aimed at moderating the rapid increase in house prices could help to channel more of these assets into China’s stock and bond markets.

Attractiveness of Chinese equities

A growing risk for investors is aptly captured by the acronym “TINA”, as in “there is no alternative” to US equities, even at record prices. Many investors are overweight US equities, which are becoming increasingly concentrated in a handful of mega cap stocks. The China A-shares market (represented by the CSI 300 Index) trades at roughly a 38% discount compared to the MSCI World Index12 and a 54% discount compared to the S&P 500.13

Total portfolio perspective

China A-shares represent one of the best diversification opportunities for Canadian investors. The CSI 300 index, one of the most well-followed broad market indices in China, has had just ~11% correlation to the S&P 500 Index since the beginning of 2005.14 For comparison, the S&P/TSX and the MSCI World indices have had correlations with the S&P 500 of roughly 76% and 93% respectively over that same period.15

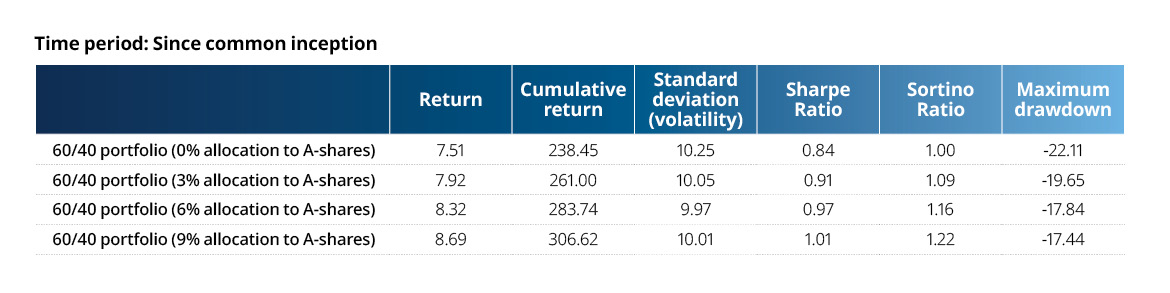

In the chart below, we’ve taken a traditional 60% equity, 40% fixed income portfolio and added an allocation to the CSI 300 Index.

Increasing allocations to China’s onshore equities not only increased the return for the total portfolio, but also helped to lower the volatility and the maximum drawdown experienced over this period. However, Canadian investors on average have just a 0.3% direct allocation to Chinese equities.16

An easy way to have an allocation to China

China faces challenges in the coming years; however, it also offers unique opportunities for full-cycle investors. Theories about the impending collapse of the Chinese economy have a long history now, from a myriad of sources. Thus far they all have one thing in common: they’ve all been wrong.

Canadian investors should look at Chinese equities objectively, with a total portfolio approach in mind.

Mackenzie Investments has the only onshore (A-shares) ETF available in Canada: the Mackenzie China A-Shares CSI 300 Index ETF (QCH), which tracks the CSI 300 – you can find out more about it here.

Investors, for more information read this piece on ‘Why China’ and/or talk to your advisor about increasing your exposure to the huge potential that China offers. Advisors, talk to your Mackenzie sales team for more details.

2. The World Bank: The World Bank in China

3. The World Bank: Open data, as of 2019

4. Mackenzie Investments and Bloomberg

5. Statista: as of 2020

6. CB Insights: The Complete List Of Unicorn Companies, as of September 2021

7. Mackenzie Investments: An on-the-ground view of China

8. Mackenzie Investments: An on-the-ground view of China

9. Financial Times: ”Global holdings of Chinese stocks and bonds rise by $120bn in 2021” as of September 2021

10. Financial Times: ”Beijing Stock Exchange kicks off trading in boost to smaller companies”

11. Financial Times: Wall Street’s new love affair with China

12. Mackenzie Investments and Bloomberg: taken by dividing the CSI300 by the MSCI World P/E Ratio; as of November 12, 2021

13. Mackenzie Investments and Bloomberg: taken by dividing the CSI300 by the S&P500 P/E Ratio; as of November 12, 2021

14. Mackenzie Investments and Morningstar: period: 2005-01-01 to 2021-10-31

15. Mackenzie Investments and Morningstar: period: 2005-01-01 to 2021-10-31

16. Mackenzie Investments: Does China deserve its own allocation?