Monthly commentary - Mackenzie Fixed Income Team

About the author

IN THIS ARTICLE min read

Key highlights

- Tighter global energy supply chains and elevated oil prices are proving structural rather than temporary, suggesting that both inflation and central bank interest rates will remain "higher for longer" than markets currently expect.

- Economic paths are diverging significantly; a resilient U.S. economy backstopped by a strong labor market contrasts with a fragile Canadian outlook weighed down by weak business sentiment and trade negotiation uncertainty.

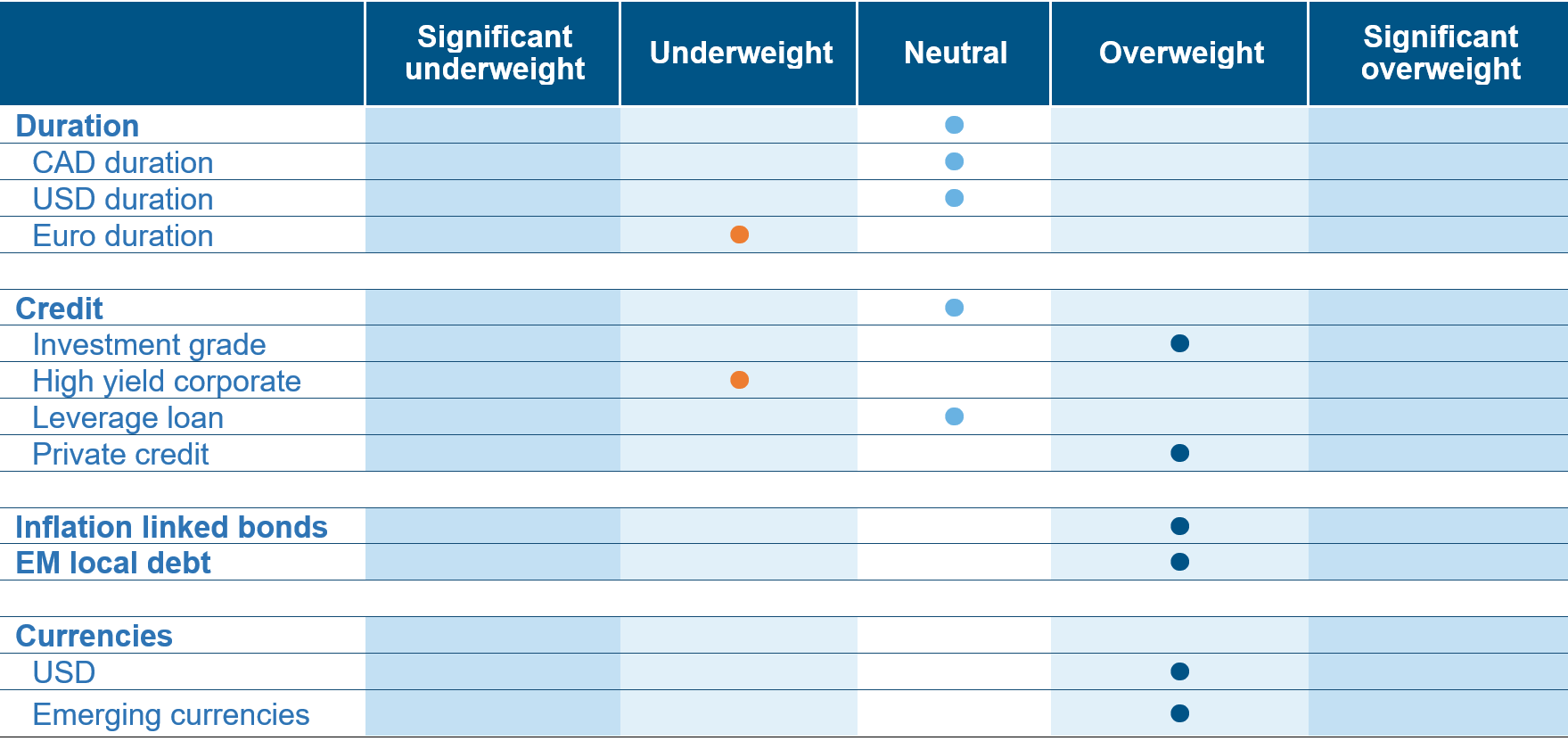

- We maintain a core, long-term overweight position in long-dated U.S. inflation-linked bonds (TIPS) to hedge against ongoing price volatility, while remaining underweight European and underweight Japanese government debt.

- As an expression of our economic divergence view, the team is positioned long in the U.S. dollar versus the Canadian dollar and holds a highly selective emerging market debt allocation that strongly favors Brazil's attractive real yields over Mexico.

- Our broader corporate credit stance remains defensive and focused on earning steady income through high-quality, floating-rate assets that perform well in high-rate environments, while strictly avoiding higher-risk, stressed borrowers.

Fixed Income team views

Source: Mackenzie Investments. As of May 31, 2026.

Source: Mackenzie Investments. As of May 31, 2026.

Fixed Income market update

Fixed income markets continued to navigate a highly uncertain macro backdrop during the period, shaped by persistent inflation pressures, elevated energy prices, and growing divergence between economic conditions in the U.S. and Canada. The team’s view remains that inflation risks are being underestimated by markets, particularly as higher energy prices increasingly appear structural rather than transitory. Ongoing disruptions across global energy supply chains, combined with constrained inventories and geopolitical uncertainty, continue to support a “higher for longer” environment for both inflation and interest rates.

In the U.S., economic data has continued to surprise to the upside, particularly within the labour market. Markets are currently pricing a resilient U.S. economy, and stronger-than-expected employment and growth data could create additional upward pressure on real yields and front-end interest rates. While some market participants continue to debate whether the Fed may eventually shift toward alternative inflation measures such as trimmed-mean PCE, core inflation remains elevated and the Federal Reserve continues to face a challenging balancing act between inflation control and growth risks. The team believes the Fed is likely to remain cautious, with the possibility that policy rates stay elevated for longer than markets expect.

In Canada, the outlook remains more fragile. Economic growth, productivity trends and business sentiment have all weakened meaningfully, while uncertainty surrounding upcoming CUSMA negotiations continues to weigh on corporate confidence and investment intentions. Management teams across Corporate Canada remain hesitant to commit to long-term capital investment until there is greater clarity on trade relations and supply chains. Although inflation remains elevated, the Bank of Canada is increasingly confronted with a difficult trade-off between maintaining price stability and supporting a weakening domestic economy. As a result, the team continues to believe that Canada is more likely to see eventual policy easing relative to the U.S., even if markets are currently reluctant to fully price that divergence.

Fund positioning

Against this backdrop, portfolio positioning remained focused on balancing inflation protection with caution around growth risks. During the period, the team exited its tactical long position in 30-year Canadian bonds after benefiting from the anticipated index extension-related demand and attractive entry levels. Tactical exposure to short-dated U.S. TIPS was also reduced after inflation-linked carry and stronger CPI data helped the position perform as expected.

The portfolio continues to maintain structural exposure to long-dated U.S. inflation-linked bonds, reflecting the view that inflation volatility and structurally higher energy prices could persist over the medium term. Within global rates, the strategy remains underweight European and Japanese duration, supported by the belief that long-end global bond yields still face upward pressure over time. The team also continues to monitor opportunities for yield curve steepening trades, particularly in the U.S., where fiscal risks and persistent inflation may eventually pressure longer-dated yields higher.

Within currencies, the portfolio maintains a constructive view on the U.S. dollar relative to the Canadian dollar, supported by stronger U.S. economic momentum and the potential for Canadian economic weakness tied to trade uncertainty. Emerging market exposure remains selective, with a preference for Brazil due to its attractive real yields and longer-term valuation opportunities, while exposure to Mexico has been reduced. The team also continues to favour differentiated country-specific opportunities within emerging markets over broad-based high yield exposure.

Overall, the portfolio remains positioned defensively while retaining flexibility to capitalize on dislocations created by heightened macro and policy uncertainty. The team continues to emphasize diversification across inflation-sensitive assets, real yields, currencies and selective emerging market opportunities as markets adjust to a structurally more volatile inflation and rates environment.

While pockets of stress remain within lower quality and more structurally challenged issuers, broader corporate fundamentals across credit markets have generally remained stable. This dynamic continues to support carry-oriented fixed income strategies, particularly in floating-rate assets where elevated income levels remain attractive in a higher for longer interest rate environment.

Central bank watch

Region | Latest CPI Inflation | Policy rate | Latest policy action | Next decision date | Market expectation | Outlook |

Canada | 2.80% | 2.25% | No change | 15-Jul-26 | No change | Neutral |

United States | 4.20% | 3.75% | No change | 17-Jun-26 | No change | Neutral |

Eurozone | 3.20% | 2.40% | 25 bp hike | 23-Jul-26 | Rate hike | Neutral |

Japan | 1.40% | 0.75% | No change | 16-Jun-26 | Rate hike | Underweight |

Australia | 3.20% | 4.35% | 25 bp hike | 16-Jun-26 | No change | Neutral |

Credit market performance

Credit markets remained resilient during the period despite ongoing macro uncertainty and evolving geopolitical risks. Investor sentiment improved as markets responded positively to easing tensions surrounding U.S.-Iran negotiations, solid corporate earnings and continued evidence of economic resilience, particularly in the U.S. Equity markets moved higher over the month, helping support broader risk appetite across both high yield bonds and leveraged loans. While inflation remains elevated and central bank messaging continues to lean cautious, credit markets have thus far remained supported by steady inflows, healthy corporate fundamentals and strong technical demand.

Within high yield, spread tightening continued through May as investors remained comfortable extending risk exposure despite a still uncertain rates backdrop. However, market performance beneath the surface became increasingly selective. Higher quality credit segments generally outperformed, while lower quality credits lagged amid growing investor sensitivity toward weaker balance sheets and more challenged business models. This growing dispersion across credit markets has become an important theme, particularly within sectors exposed to structural disruptions such as technology and software, where investor differentiation between potential long-term winners and losers continues to widen. The leveraged loan market also continued to benefit from strong technical conditions. New issuance activity accelerated over the month, although much of the activity consisted of repricing and refinancing transactions rather than new leveraged buyout activity, reflecting continued caution from corporate borrowers and financial sponsors. Default activity remained relatively benign, with no payment defaults recorded during the month and overall default trends continuing to improve modestly year over year.

Index | Yield | Yield m/m | Spread | Spread m/m | Performance (%) | |||

bp | bp | bp | 1m | 3m | YTD | 1Y | ||

Investment Grade | ||||||||

CA | 4.0% | -16 | 86 | -3 | 1.3 | 0.6 | 2.0 | 4.4 |

US | 5.2% | 0 | 74 | -8 | 0.7 | -0.3 | 0.8 | 6.2 |

High Yield |

|

|

|

|

|

|

|

|

CA | 6.9% | -10 | 253 | -17 | 1.0 | 0.9 | 1.4 | 6.8 |

US | 7.4% | 3 | 274 | -9 | 0.5 | 1.2 | 1.6 | 7.4 |

US Leverage Loans | 8.1% | -1 | 428 | -1 | 0.5 | 2.3 | 1.2 | 5.1 |

Source: Bloomberg, as of May 31, 2026. Performance is reflective of local returns.

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns as of May 31, 2026, including changes in share value and reinvestment of all distributions and does not take into account sales, redemption, distribution, or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated. Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in investment products that seek to track an index.

This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties, and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of May 31, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

The content of this commentary (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

All information is historical and not indicative of future results. Current performance may be lower or higher than the quoted past performance, which cannot guarantee results. Share price, principal value, and return will vary, and you may have a gain or a loss when you sell your shares. Performance assumes reinvestment of distributions and does not account for taxes. Performance may not reflect any expense limitation or subsidies currently in effect. Short-term trading fees may apply.

This material is for informational and educational purposes only. It is not a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. It is not intended to address the needs, circumstances, and objectives of any specific investor. Mackenzie Investments, which earns fees when clients select its products and services, is not offering impartial advice in a fiduciary capacity in providing this sales and marketing material. This information is not meant as tax or legal advice. Investors should consult a professional advisor before making investment and financial decisions and for more information on tax rules and other laws, which are complex and subject to change.

The rate of return is used only to illustrate the effects of the compound growth rate and is not intended to reflect future values of the mutual fund or returns on investment in the mutual fund.