The ETF Lab

ETF Spotlight:

Three takeaways from markets in 2024

In this week’s spotlight, we’re highlighting three market developments from early 2024, including US earnings growth, Japanese/International equity gains, and a positive set-up for Canadian fixed income.

US earnings concentration

After market behemoth Nvidia posted another strong quarter of earnings growth, its CEO stated that artificial intelligence is at a “tipping point”. This spurred a flurry of commentary as to whether this was the makings of further market gains or an overblown, concentrated bubble – comparable to the dot-com era.

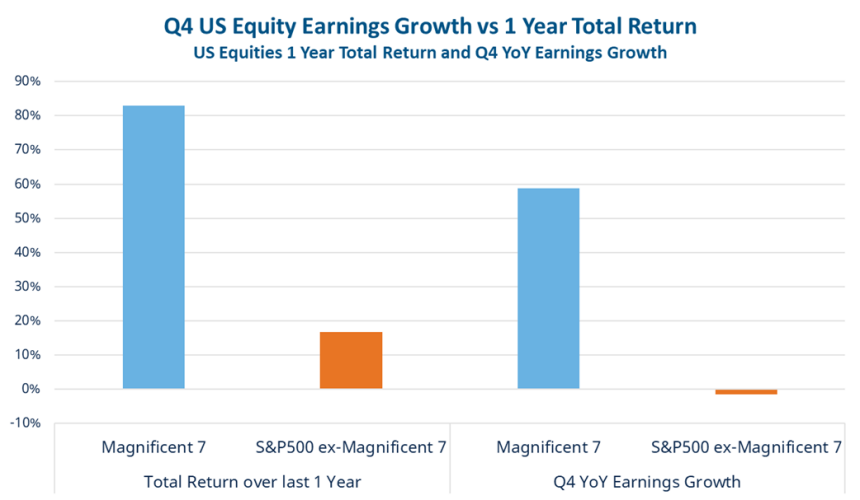

Source: Bloomberg; as of February 23, 2024, returns in local currency.

Source: Bloomberg; as of February 23, 2024, returns in local currency.

Comparisons to the dot-com era made famous by unprofitable companies such as Pets.com are a stretch, even if this rally proves over done. The US large cap equity market is more concentrated today, with over 31% of the market in just the top 10 holdings.1 However, as shown above, YoY % earnings growth in Q4 was markedly different for those of the Magnificent 7 versus those of the rest of the S&P 500 Index.

Year-to-date in 2024, US equities are once again amongst the best performing asset classes and for better or for worse, are once again being led by its biggest components.

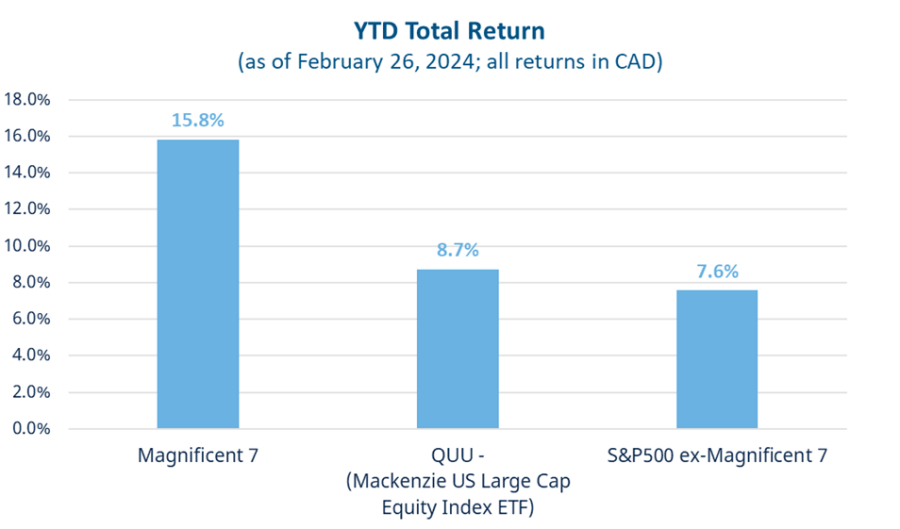

Source: Bloomberg

Source: Bloomberg

Japan surpassing all time highs… 34 years later

The Nikkei 225 Index, Japan’s most famous index, has surpassed its previous record set in December 1989. While the Nikkei’s market cap weighted and more broadly diversified alternative – the Topix Index – still has a little further to go to pass its long-standing record, this current rally marks a milestone for the Japanese stock market.

Source: Bloomberg; as of Feb. 28, 2024

Source: Bloomberg; as of Feb. 28, 2024

Japanese stocks have rallied on the back of a weaker currency, but also growing recognition of corporate reforms and strong earnings growth. These fundamentals have provided some comfort that after many false starts this rally is more sustainable.

As we outlined previously in The ETF Lab: International Equity Investing with ETFs, strong macro tailwinds and a growing valuation gap are reasons investors may want to consider investing outside US and Canadian stocks in 2024.

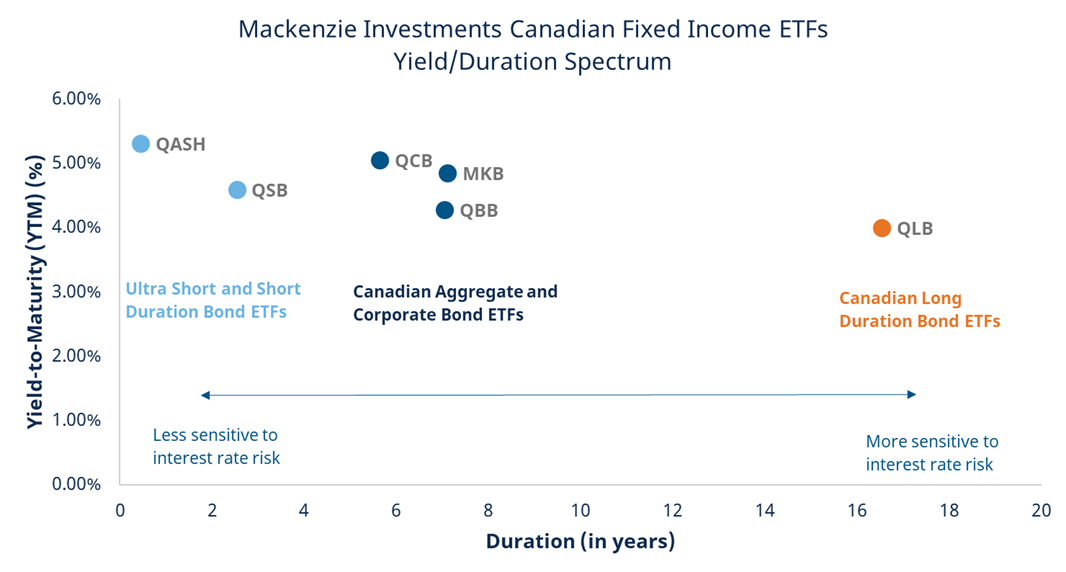

Source: Mackenzie Investments; as of Feb. 26, 2024; **characteristics as of Jan. 31, 2024

Source: Mackenzie Investments; as of Feb. 26, 2024; **characteristics as of Jan. 31, 2024

Positive outlook on Canadian fixed income

Softening inflation and weakening demand in Canada may further erode the case for GICs and/or money market instruments, as forward policy projections adjust to diverging economic data between Canada and the US.

Below are several Canadian fixed income ETFs sorted by duration, or sensitivity to interest rate moves, and yield to maturity.

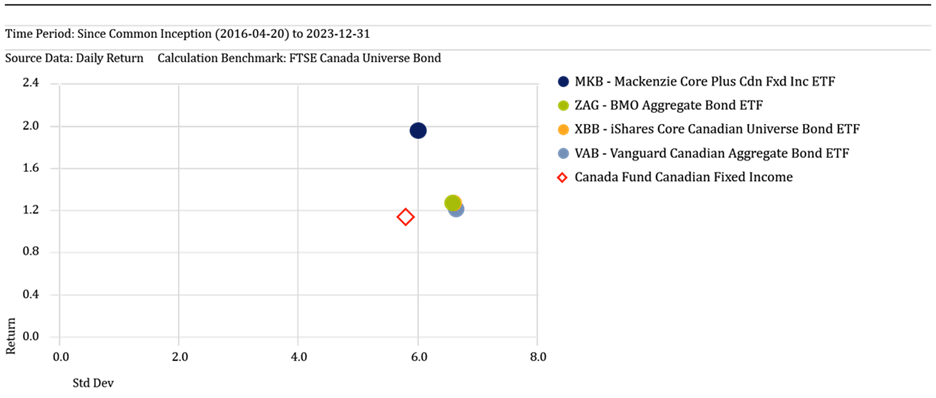

Source: Mackenzie Investments; as of January 31, 2024

Source: Mackenzie Investments; as of January 31, 2024

For a core, actively managed exposure to Canadian fixed income investors can consider MKB (Mackenzie Core Plus Canadian Fixed Income ETF). The core portion of MKB, a minimum of 75% of the ETF, is invested in investment-grade federal, provincial, and corporate bonds, while the satellite portion (roughly 25%) can be allocated to non-investment grade credit, including high-yield bonds, sovereign / quasi-sovereign bonds and leveraged loans from issuers around the world.

This core-plus, active approach has helped MKB, a 5-star Morningstar rated strategy, outperform traditional index ETFs in this category on a risk-adjusted basis.

Source: Morningstar. Period: since common inception to December 31, 2023

Source: Morningstar. Period: since common inception to December 31, 2023

ETF News & Notes

A simple ETF solution for long-term growth in registered accounts

To help provide a single ticket solution for RRSP/TFSA/RESP accounts, we launched a full suite of asset allocation ETFs, including the newest addition MEQT (Mackenzie All-Equity Allocation ETF).

Mackenzie’s suite of asset allocation ETFs (MCON / MBAL / MGRW/ MEQT) provides a range of strategic asset allocations and access to thousands of underlying securities, all for a management fee of just 17 bps. These ETFs can help investors achieve their goals by minimizing the need – and associated costs – of trading multiple ETFs, as well as making the rebalancing process easier.

For more information on MEQT, which invests in 100% equities, see our feature page: Mackenzie Asset Allocation ETFs (mackenzieinvestments.com)

A look at covered call ETFs

Prerna Mathews, VP of ETF Product Strategy, recently wrote a great piece taking a look at covered call ETFs. In this piece, Prerna breaks down how they generate income and outlines some potential drawbacks.

For some further notes on covered call ETFs, read: The ETF Lab: Considerations on covered call ETFs.

ETF Trading Tip: Understanding ETF premiums and discounts

A key advantage of the ETF structure is that the price of ETF units generally trades in line with the market value of its underlying basket of securities (net asset value).

However, ETF premiums and discounts can occur for several reasons. Two primary drivers include:

- If the underlying securities trade on an exchange that is open at a different time than the exchange the ETF trades on, there could be deviations between current and stale security pricing, resulting in possible premiums or discounts.

- If the underlying securities become less liquid or markets are experiencing heavy order flow, the result may mean higher transaction costs, leading to larger premiums and discounts.

For a deeper look into this topic, read our white paper: Understanding Exchange Traded Funds premiums and discounts.

ETF Flows Update

- OSFI’s ruling - that bank deposits from HISA ETFs must adhere to 100% wholesale liquidity treatment – took effect at the start of February. The CAD$ HISA ETFs have lost more than $233M in assets in the first three weeks of February.2

- As yields in GICs and HISA ETFs have started to decline, ultra-short duration bond ETFs have attracted significant inflows. QASH (Mackenzie Canadian Ultra Short Bond Index ETF) now has over $80M in assets since launching in mid-November 2023.3

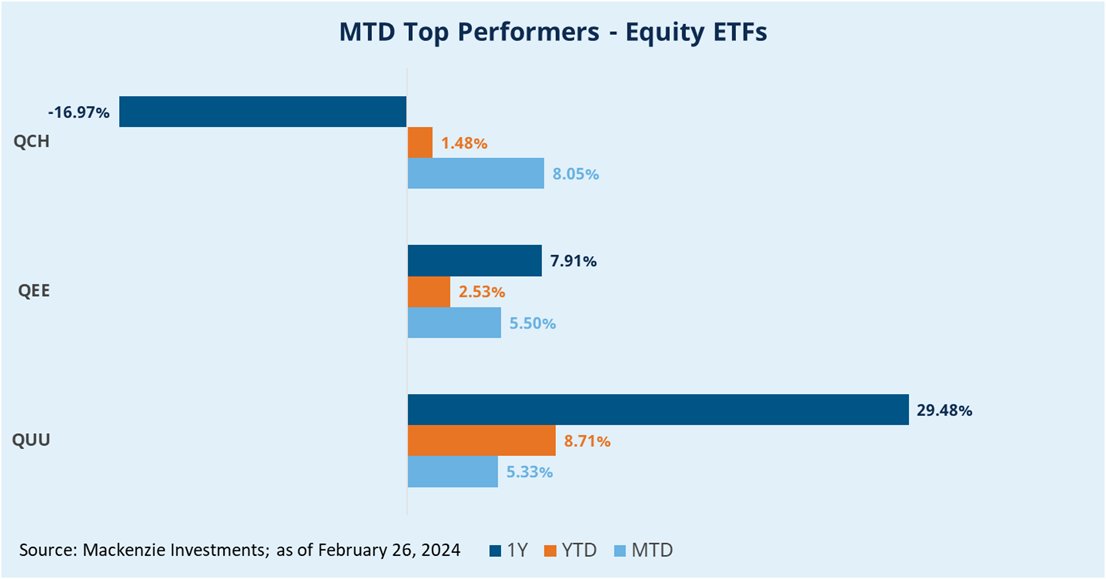

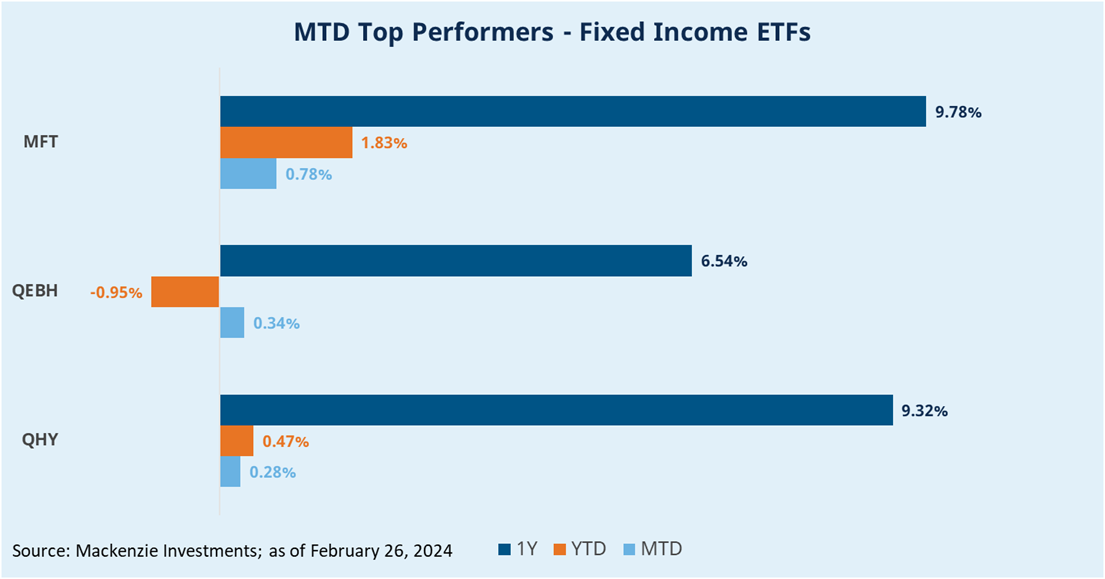

Mackenzie ETF Top Performers

1 Source: Bloomberg, as of Feb. 28, 2024; % of top 10 holdings in QUU – Mackenzie US Large Cap Equity Index ETF

2 Source: Bloomberg, Mackenzie Investments; as of February 27, 2024

3 According to NBF Weekly ETF Flows week ending February 23, 2024

FOR ADVISOR USE ONLY. No portion of this communication may be reproduced or distributed to the public as it does not comply with investor sales communication rules. Mackenzie disclaims any responsibility for any advisor sharing this with investors.

Commissions, brokerage fees, management fees, and expenses all may be associated with Exchange Traded Funds. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns, including in share or unit value and reinvestment of distributions and does not take into account sales, redemption, distribution, or optional charges or income taxes payable by any securityholder that would have reduced returns. Exchange Traded Funds are not guaranteed, their values change frequently, and past performance may not be repeated.

The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This should not be construed as legal, tax or accounting advice. This material has been prepared for information purposes only. The tax information provided in this document is general in nature and each client should consult with their own tax advisor, accountant and lawyer before pursuing any strategy described herein as each client’s individual circumstances are unique. We have endeavored to ensure the accuracy of the information provided at the time that it was written, however, should the information in this document be incorrect or incomplete or should the law or its interpretation change after the date of this document, the advice provided may be incorrect or inappropriate. There should be no expectation that the information will be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise. We are not responsible for errors contained in this document or to anyone who relies on the information contained in this document. Please consult your own legal and tax advisor.

This article may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of February 27, 2024. There should be no expectation that such information will in all circumstances be updated, supplemented, or revised whether as a result of new information, changing circumstances, future events or otherwise.

Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in the investment products that seek to track an index.

The Mackenzie ETFs are not sponsored, promoted, sold or supported in any other manner by Solactive nor does Solactive offer any express or implicit guarantee or assurance either with regard to the results of using the Indices, trade marks and/or the price of an Index at any time or in any other respect. The Solactive Indices are calculated and published by Solactive. Solactive uses its best efforts to ensure that the Indices are calculated correctly. Irrespective of its obligations towards the Mackenzie ETFs, Solactive has no obligation to point out errors in the Indices to third parties including but not limited to investors and/or financial intermediaries of the Mackenzie ETFs. Neither publication of the Solactive Indices by Solactive nor the licensing of the Indices or related trade mark(s) for the purpose of use in connection with the Mackenzie ETFs constitutes a recommendation by Solactive to invest capital in said Mackenzie ETFs nor does it in any way represent an assurance or opinion of Solactive with regard to any investment in these Mackenzie ETFs.