Building smarter AI exposure

About the author

IN THIS ARTICLE min read

Artificial intelligence is generating one of the most significant reallocations of capital in a generation—cutting across asset classes, industries and the public-private divide. The question for portfolio managers is no longer whether to have exposure, but how to structure it.

Perspectives for modern portfolio construction

Artificial intelligence has become one of the most influential forces in global capital markets. Yet in many portfolios, exposure remains concentrated in a narrow group of large public technology companies.

AI is not just a software story. It is driving a broad expansion of how capital is deployed across asset classes, industries and the economy at large.

More than a stock story:

AI is an economic system

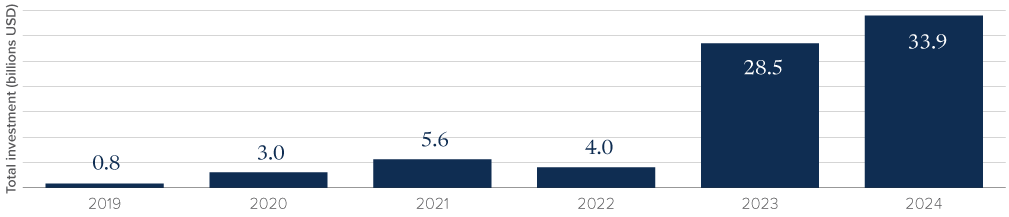

AI development requires substantial investment in physical and digital infrastructure. Private capital has flowed into data centers, semiconductors, fiber networks and related infrastructure to support this demand. Since 2020, private equity firms have invested more than US$200B into data centers, semiconductors and related energy infrastructure,1 as part of a “picks and shovels” strategy focused on enabling capacity rather than predicting individual winners.

Broader investment data reinforces the scale. According to the Stanford Institute for Human-Centered Artificial Intelligence, corporate AI investment exceeded US$252.3B in 2024, with private investment rising 44.5 percent year over year. 2

Figure 1: Global private investment in generative AI, 2019 - 2024

Source: Stanford HAI 2025 AI Index Report; and Quid, 2024.

This capital is not concentrated solely in early-stage venture funding. Infrastructure managers finance data centres and fiber networks. Private equity supports mid-market companies utilizing AI in targeted industries. Private credit structures financing for AI-enabled growth.

Recognizing this scale of investment behind AI shifts the focus from individual stock selection to how portfolios can gain exposure across the broader AI ecosystem.

Diversifying AI exposure beyond mega-cap tech

The economic build-out tied to AI is uneven and multi-layered, with each layer behaving differently within portfolios.

1. Established companies enhancing productivity

Many public companies are integrating AI to improve operational efficiency, pricing accuracy and customer engagement. For example, financial institutions are using machine learning to enhance fraud detection and compliance workflows. Healthcare companies are applying AI in diagnostics and pharmaceutical discovery. In industrial settings, predictive analytics are being used to reduce downtime and optimize maintenance.

Within industrial sectors, manufacturing provides a clear example of this impact. Predictive maintenance has demonstrated significant reductions in unplanned machine downtime, in some cases approaching 50% in large-scale deployments.3

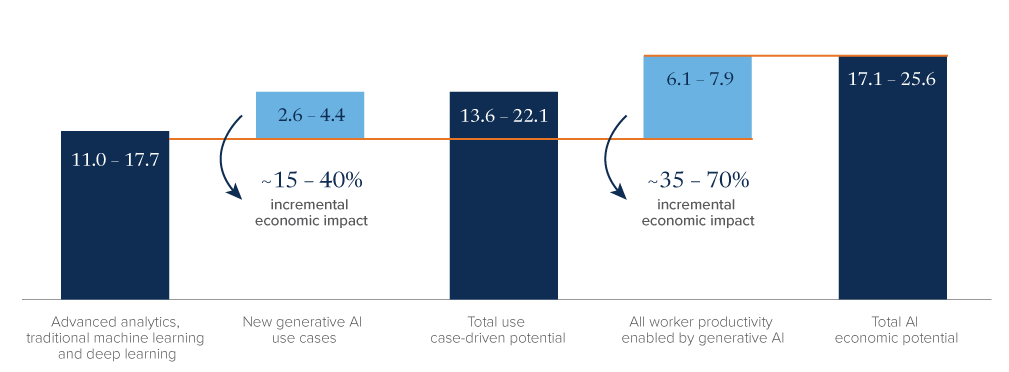

Research from McKinsey estimates generative AI could contribute between US$2.6T and US$4.4T annually in economic value across identified use cases (a targeted application of generative AI to a specific business challenge), when applied across industries. In addition, the research estimates that when combined with overall worker productivity improvements, benefits could reach US$6.1 – 7.9 trillion annually.4

Figure 2: AI’s potential impact on the global economy, US$T

Source: McKinsey, The economic potential of generative AI, June 2023.

In this layer, AI enhances established competitive positions where returns are tied to execution and margin improvements, not thematic multiple expansion. As a result, this layer tends to behave like traditional equity exposure, where AI contributes incrementally to earnings rather than driving valuation alone.

2. Mid-market innovation and application

Beyond large incumbents, AI-driven innovation frequently originates in mid-market companies building industry-specific solutions. These application-layer dynamics can be seen in private market portfolios focused on targeted industry solutions.

This layer reflects where AI moves from capability to application, often in highly targeted use cases. For instance, Ramp, a leader in finance automation, applies AI to help businesses control spending and automate expense management. The platform's AI analyzes spending in real-time to enforce financial policies and identifies cost-saving opportunities, leading to measurable improvements in operational efficiency. 5

Another example is Gatik, which uses AI to automate 'middle-mile' logistics. By deploying autonomous trucks on fixed, repeatable routes for major retailers, Gatik translates AI-driven precision into more resilient and efficient supply chains.6

3. Infrastructure and the “picks and shovels” strategy

The third layer focuses on enabling infrastructure. Computing, power and specialized chips are necessary inputs for AI scale. Capital is flowing into these enabling layers regardless of which application ultimately dominates.

Data centres provide the compute capacity required for AI workloads. Fiber networks enable high-speed data transmission. Semiconductor manufacturing supports specialized chip demand. One example is Wolfspeed, a silicon carbide producer supplying critical semiconductor materials. In 2023, the company announced US$1.25B of secured financing from a consortium led by Apollo, supporting its broader capacity expansion plans.7

Electricity demand from data centre operations is projected to increase materially over the coming decade. The International Energy Agency estimates global electricity demand from data centres could more than double by 2030 to around 945 terawatt-hours, with AI-optimized data centres expected to be the largest driver of that increase. For infrastructure investors, this shifts attention from data centre demand alone to the quality of power access, grid interconnection, long-term energy contracts and development execution. In the "picks and shovels" layer, power availability can be as important as compute demand.8

Investing in this layer provides exposure to the infrastructure required for AI growth, while reducing reliance on any single application or platform.

Concentration in AI’s most visible names

Market cap-weighted indices can appear diversified while remaining highly concentrated beneath broad sector labels. In early 2026, the ten largest companies in the S&P 500 accounted for approximately 39% of total index weight.9

At the same time, product-level analysis indicates that direct AI-related revenues represent a smaller share of overall index earnings than market capitalization alone might suggest.10

This creates a gap between where capital is being deployed across the AI ecosystem and where portfolios may be most exposed. Structuring exposure across layers broadens participation in that build-out and reduces reliance on a narrow segment of public markets.

Implementation matters:

underwriting and risk discipline

The dispersion of outcomes across these layers is unlikely to be uniform. Exposure to AI-related growth is not only a function of where capital is allocated, but how it is underwritten and managed over time.

In private markets, this places greater emphasis on underwriting discipline, portfolio construction and ongoing monitoring. The impact of AI on a borrower or portfolio company can vary significantly depending on industry dynamics, competitive positioning and the role AI plays within the business. In some cases, AI may act as a disruptive force. In others, it may enhance productivity or remain largely peripheral.

Assessing these dynamics requires a structured approach that considers factors such as integration within core business processes, the essential nature of the service, switching costs and the potential for technological displacement. These frameworks can differ across managers and shape how risk is identified, priced and managed over time. The value of disciplined underwriting is in assessing whether AI represents a material disruption risk, a productivity enabler or a more limited factor for each borrower, portfolio company or infrastructure asset.

Structuring AI exposure in portfolios

Artificial intelligence is reshaping industries, supply chains and capital allocation. Its impact extends beyond a narrow group of public companies and into the broader systems that support and apply it.

Viewing AI as an ecosystem rather than a single equity theme can help align portfolio construction with how capital is being deployed across the economy. It also reduces reliance on any one expression of the AI thesis, whether that is a mega-cap public equity, an application-layer company or an infrastructure asset.

AI is not one trade or a single stock narrative. It is a multi-layered transformation unfolding across industries and asset classes. Because AI introduces different risks across companies, borrowers and assets, manager quality matters. Disciplined underwriting and active monitoring are central to identifying where AI strengthens an investment case, where it creates vulnerability and where the market may be overstating the opportunity. Aligning portfolios with that broader deployment of capital brings exposure closer to where the underlying economic change is taking place.

To learn more about the Mackenzie Northleaf private markets suite, including the new multi-asset fund please visit mackenzieinvestments.com/private markets

1 Private Equity Propels America to the Front of the AI Race - American Investment Council

2 Economy | The 2025 AI Index Report | Stanford HAI

3 The True Cost of Downtime 2024

4 McKinsey & Company. The economic potential of generative AI. 2023

5 How Ramp Secured US$500m to Advance AI Finance Automation | FinTech Magazine

6 Middle-Mile Autonomous Trucking | AI-Driven Logistics Innovation

7 Wolfspeed Announces $1.25 Billion Funded Secured Notes Led by Apollo Credit Funds | Wolfspeed

8 IEA, Electricity 2024 Report

9 These S&P 500 alternatives have shined so far this year | Morningstar

10 Syntax Data, Quantifying the S&P 500’s Exposure to Artificial Intelligence, 2024

For accredited investors only (as defined in NI 45-106). Past performance is not necessarily indicative of any future results.

The content of this web page (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This material is not intended to constitute an offer of units of Mackenzie Northleaf Global Private Equity Fund, Mackenzie Northleaf Private Credit Fund, Mackenzie Northleaf Private Infrastructure Fund, or Mackenzie Northleaf Multi-Asset Private Markets Fund (the “Funds”). The information herein is qualified in its entirety by reference to the applicable Offering Memorandums of the Funds. The OMs contain information about the investment objectives and terms and conditions of an investment in the Funds (including fees) and also contains tax information and risk disclosures that are important to any investment decision regarding such Funds.