Written by Mackenzie Global Quantitative Equity Team

For many investors, emerging markets may represent an underused opportunity. The growth of the asset class has been rapid, with the category now accounting for 12% of global market capitalization.1 Yet exposure to emerging markets stocks may often comprise only a small fraction of the average investor’s portfolio. In our view, current conditions appear favourable for seeking alpha in this equity asset class – especially through the application of the type of holistic, quantitative investment approach we employ on the Mackenzie Global Quantitative Equity (GQE) Team.

We see three reasons underpinning this belief: relative valuations, market inefficiencies, and asset allocation and diversification.

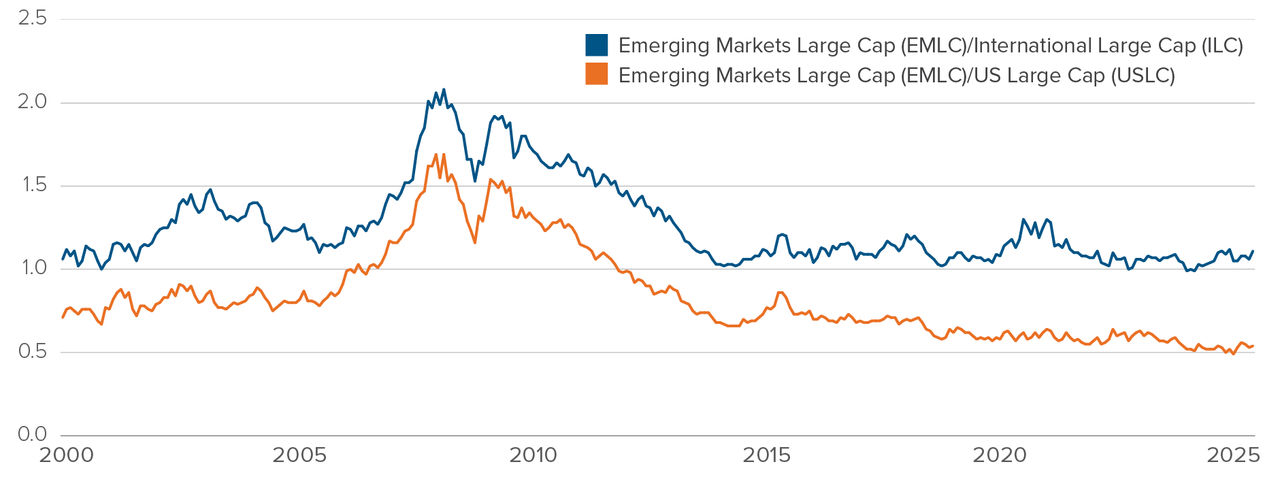

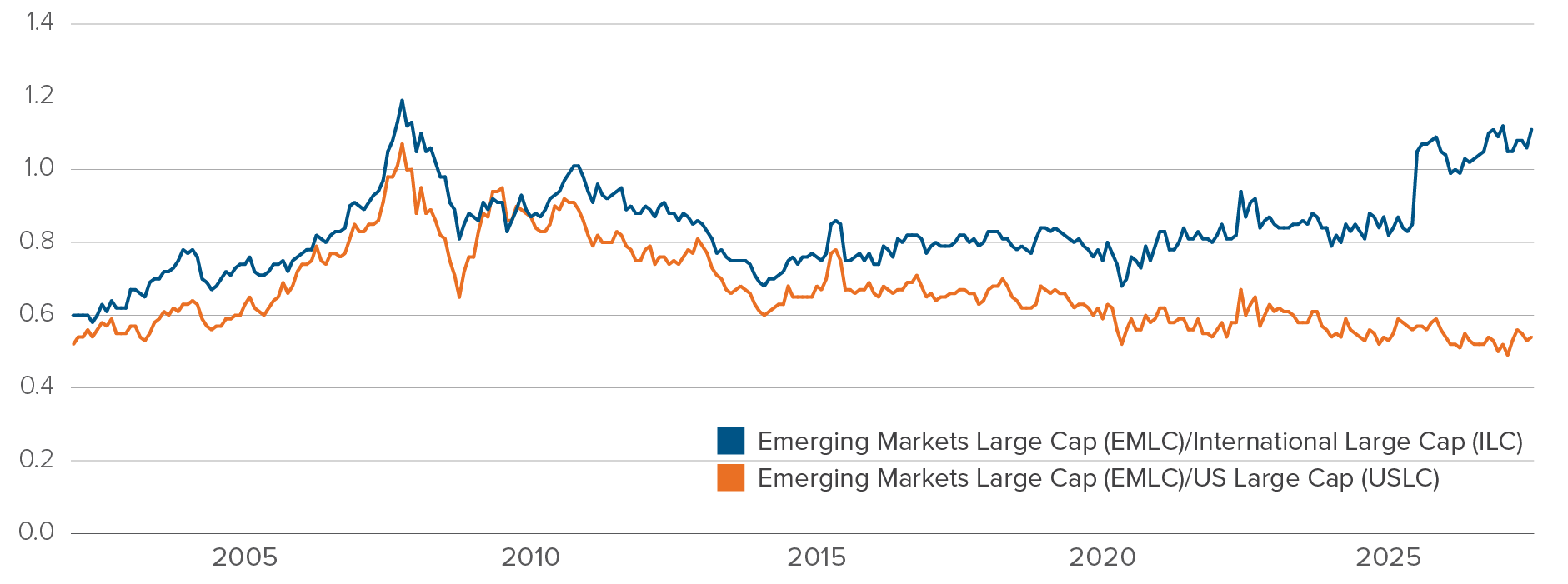

Equity valuations in emerging markets can be more appealing

At the most basic level of consideration, emerging markets equities appear to be attractively valued compared to developed markets, and particularly in relation to US stocks. As demonstrated by the charts below, emerging markets are trading at a significant discount to the US equity markets, with both price-to-sales (P/S) and price-to-forward-earnings (P/FwdE) ratios at historically low levels.² Relative to developed international markets, emerging markets valuations can be more attractive, though the discount is less pronounced.

Relative P/S valuation

Relative P/FwdE valuation

Source: Mackenzie Investments. Represents the investable universe by region for Mackenzie Global Quantitative Equity Team. Relative price/forward earnings data from January 2002 to June 2025.

Source: Mackenzie Investments. Represents the investable universe by region for Mackenzie Global Quantitative Equity Team. Relative price/forward earnings data from January 2002 to June 2025.

In short, emerging markets equities appear cheaper relative to global counterparts, which may provide attractive opportunities for investors.

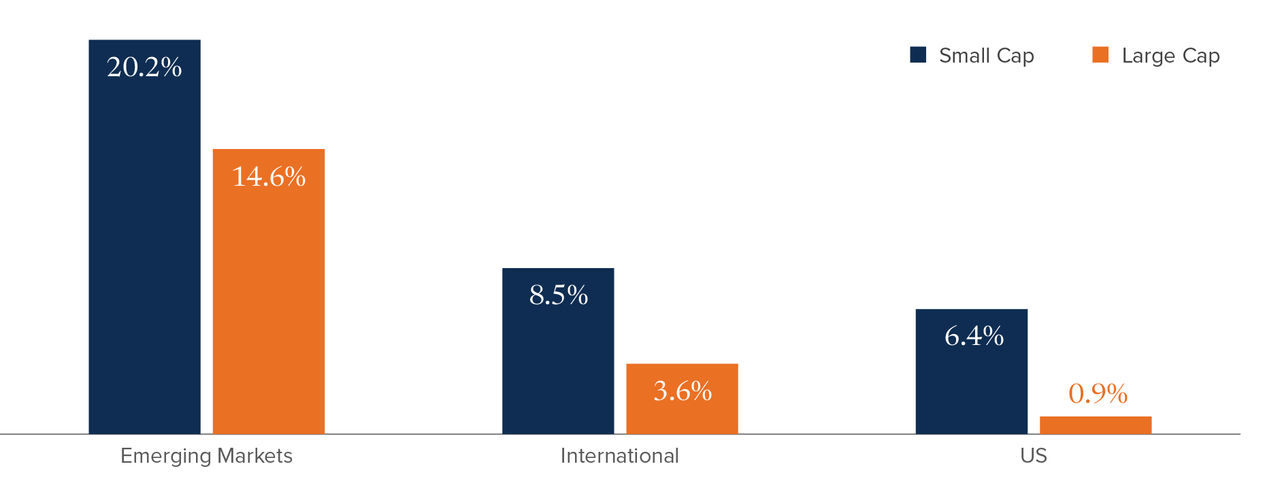

Emerging markets have inefficiencies that can be leveraged

Due to factors such as thinner analyst coverage, weaker disclosure regimes and fragmented liquidity, emerging markets can be less efficient than developed markets, creating opportunities to exploit mispricing – especially through a holistic, quantitative investment strategy.

In the chart below, 'quantitative alpha efficacy' - measured using a factor-based stock analysis equally weighted between value and momentum characteristics - highlights opportunities to exploit market inefficiencies and enhance investor returns. In this case, within both the large-cap and especially small-cap universes, the opportunity to leverage market inefficiencies appears greater in emerging markets versus developed markets, with a significant opportunity to deliver higher returns versus the US.

Quantitative alpha efficacy

Data source: Bloomberg: Represents inter-quintile return spreads using 50/50 blend of value and momentum from September 2002 – December 2024.

Source: Mackenzie Global Quantitative Equity boutique proprietary research.

Data source: Bloomberg: Represents inter-quintile return spreads using 50/50 blend of value and momentum from September 2002 – December 2024.

Source: Mackenzie Global Quantitative Equity boutique proprietary research.

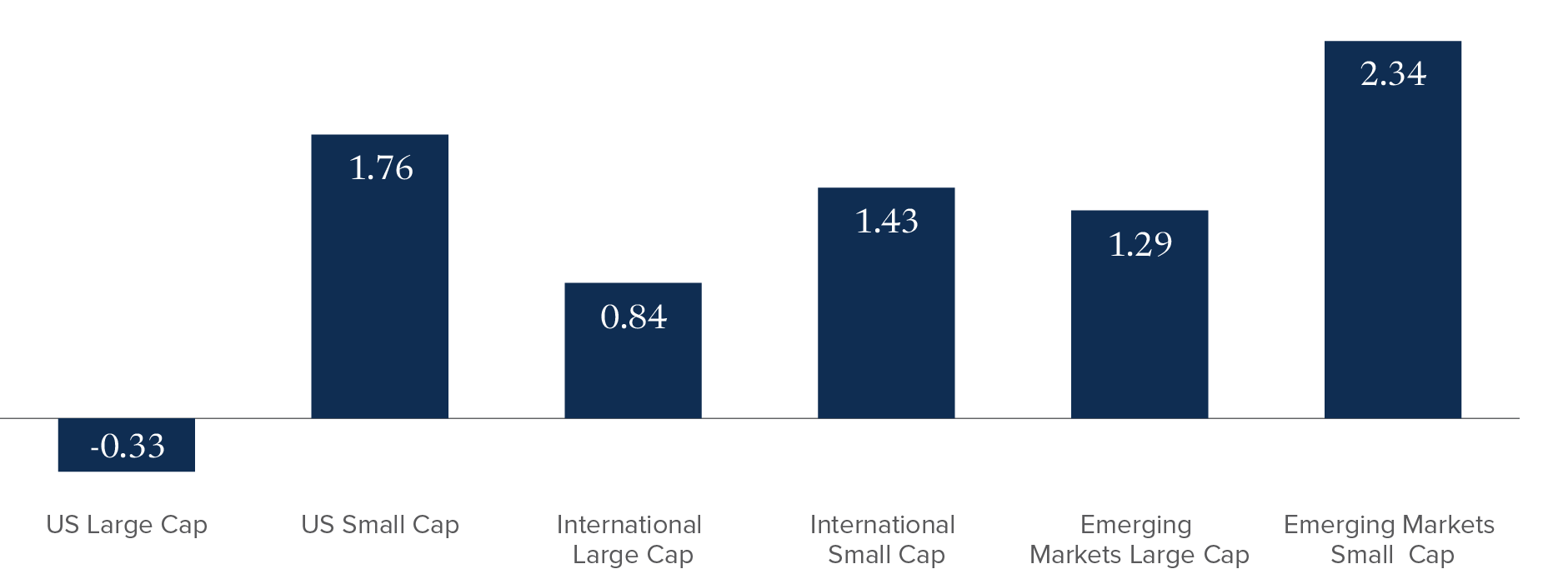

This advantage is borne out by examining the excess return of large-cap and small-cap equities across varying markets. In both asset classes, emerging markets can at times behave differently from developed markets and may enhance diversification within a global equity allocation, as shown in the chart below.

Median benchmark-relative excess return for active managers, June 2015 - June 2025

Source: eVestment

Source: eVestment

Emerging markets can offer asset allocation and diversification benefits

Despite typically representing only a small portion of most investors’ equity allocations, emerging markets should remain a critical component of a well-diversified portfolio. While acknowledging the asset class has historically experienced higher volatility than other markets, we maintain a strong conviction around the long-term growth potential in the constituent companies and countries in this class.

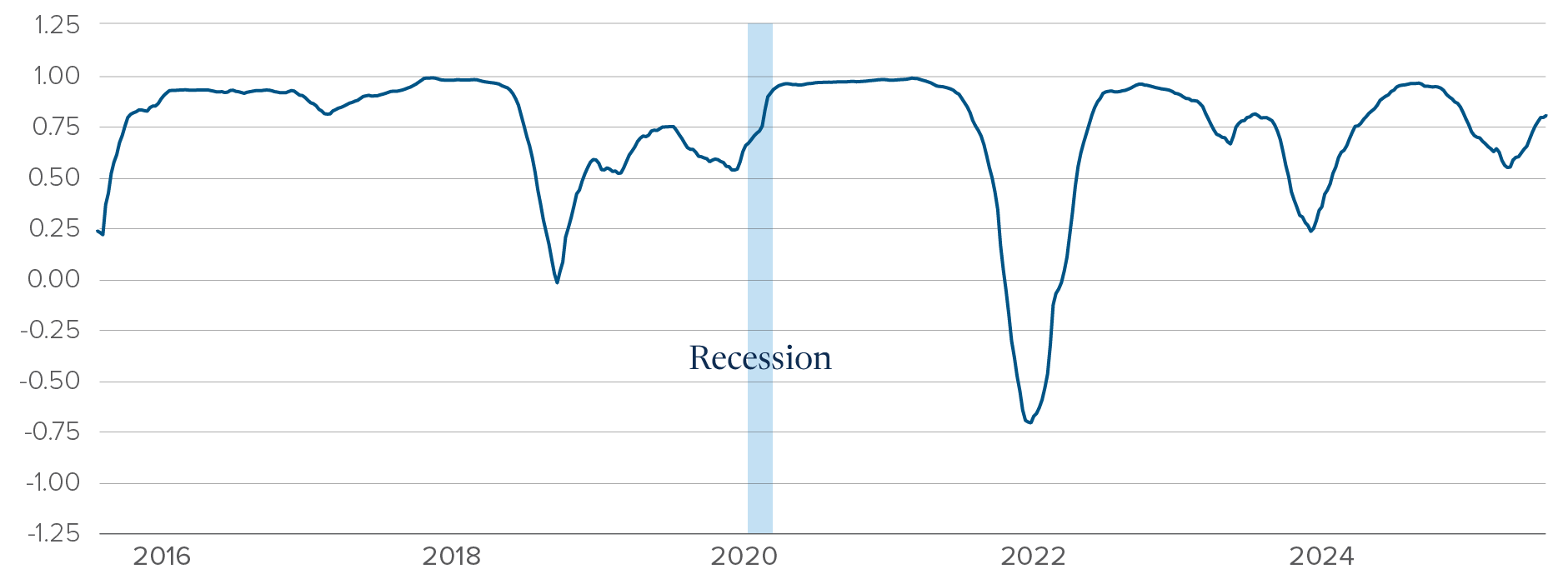

Emerging markets are supported by structural trends such as rising consumption, digital transformation and the rise of green energy that are expected to drive sustained economic expansion. Furthermore, as can be seen in the chart below, emerging markets may be uncorrelated with developed markets over time. For these reasons, we believe that a broad-based allocation to emerging markets equities offers not only attractive return potential, but also meaningful diversification benefits, making it a valuable component of a resilient global equity strategy.

The correlation between emerging and developed markets

Source: Emerging vs. Developed Markets - Updated Chart | Long term trends

We believe the benefits of investing in emerging markets equities far outweigh the challenges – especially when those challenges, such as market inefficiencies, can be leveraged to the advantage of investors through a holistic, quantitative investment approach. Given the valuation discount compared to developed market equities, emerging markets offer further alpha potential. Emerging markets thus remain a crucial diversification tool for investors, with their current attractiveness enhanced by favourable valuations.

Mackenzie Emerging Markets Fund aims to generate alpha in large, mid and small-cap stocks to capture the market inefficiencies within emerging markets.

Sources

1 Source: Bloomberg/Mackenzie Investments as of August 8, 2025.

2 Source: Mackenzie Investments. Represents the investable universe by region for Mackenzie Quantitative Equity Team. Relative price/sales data from December 1996 to June 2025.

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The performance of Mackenzie Emerging Markets Fund Series F for each period is as follows: 1 yr 24.6%, 3 yrs 18.9%, 5 yrs 11.2%. The indicated rates of return are the historical annual compounded total returns as of July 31, 2025 including changes in share value and reinvestment of all distributions and does not take into account sales, redemption, distribution, or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

The content of this page (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document may contain forward-looking information which reflect our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of August 8, 2025. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.