Written by the Mackenzie Fixed Income Team

Key Highlights

- Early 2026 fixed income markets are being shaped by elevated headline risk from the U.S., Japan, and Europe, but recent price action suggests markets are gradually refocusing on economic fundamentals rather than purely political or geopolitical noise.

- Markets are pricing roughly 50 bps of U.S. rate cuts this year, with attention on potential Federal Reserve leadership changes, where policy credibility is expected to be judged through yields and risk premia rather than rhetoric.

- Canada’s economy appears softer, with weakening labour market indicators, ongoing housing sector challenges, and easing core inflation, giving the Bank of Canada greater flexibility and supporting the case for modest rate cuts later in the year.

- Ongoing USMCA discussions represent a meaningful risk for Canada, with the auto sector especially exposed due to complex supply chains and its importance to domestic growth and credit conditions.

- Our strategy remains disciplined and selective, with an overweight in short‑term Canadian bonds, continued focus on emerging market opportunities (notably Latin America), underweight long‑duration U.S. exposure, with emphasis on carry, diversification, and risk management.

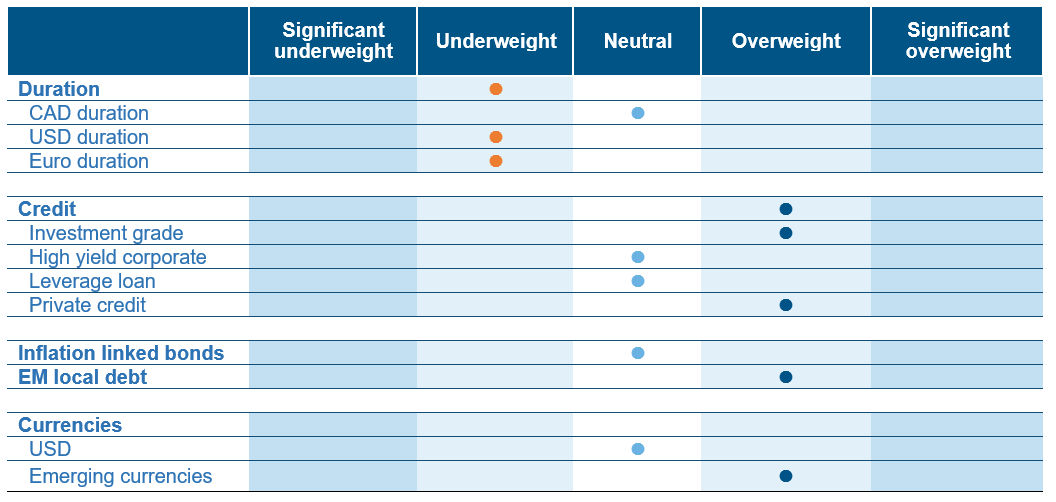

Fixed Income Team Views

Source: Mackenzie Investments. As of Jan 31, 2026

Source: Mackenzie Investments. As of Jan 31, 2026

Fixed Income Market Update

As we move through early 2026, investors are navigating a market environment defined by elevated uncertainty but also by opportunity. The past several weeks has been dominated by headline risk, particularly out of the United States, but also from Japan and Europe. Geopolitical tensions, energy market developments, and political negotiations have all contributed to market volatility. Unlike parts of last year, recent price action has been more two‑sided, reflecting investor caution. While this can feel unsettling, fixed income markets are beginning to find their footing as the focus gradually shifts back to economic fundamentals.

One key source of uncertainty has been the evolving discussion around U.S. Federal Reserve leadership and the associated confirmation process. While markets are currently pricing approximately 50 bps of U.S. policy rate easing over the course of the year, investors remain focused on how a potential change in leadership might influence the Fed’s reaction function. Kevin Warsh, frequently referenced in market discussions, is generally viewed as having been more inflation‑focused and less inclined toward balance sheet expansion earlier in his career. As always, markets will ultimately judge policy credibility through bond yields and risk premia rather than rhetoric.

Beyond the Fed, investors continue to monitor legal and trade‑related risks that could materially affect market sentiment. In particular, an outstanding U.S. Supreme Court decision related to the International Emergency Economic Powers Act (IEEPA) represents a near‑term event risk.

U.S. 10‑year Treasury yields moved outside the narrow range that defined much of late 2025 and briefly pushed higher suggesting that markets are testing the current equilibrium. We believe some of the extreme uncertainty seen earlier in the year may begin to fade, allowing economic data to play a more central role in driving markets.

Closer to home, Canada’s economic backdrop looks more subdued. While headline employment data has been mixed, underlying indicators point to a softer labour market. At the same time, the housing sector, an important driver of Canadian growth, continues to face challenges, including falling prices in certain segments and slower activity overall. Inflation in Canada has been easing, particularly on core measures that the Bank of Canada watches closely. This gives policymakers more flexibility should economic conditions weaken further. As a result, we believe there is a reasonable case for modest rate cuts later this year, particularly in the first half.

For Canadian markets, trade policy remains particularly important. Ongoing discussions around the future shape of USMCA, and specifically potential changes to rules of origin requirements, are a notable risk. The auto sector stands out as especially sensitive, given its reliance on complex supply chains and its economic importance to Canada, particularly Ontario. Stricter rules of origin, especially around components sourced from outside North America could raise costs and increase uncertainty for manufacturers, with knock‑on effects for growth and credit conditions.

Fund Positioning

In this environment, our approach remains disciplined and selective. Rather than reacting to every headline, we remain focused on fundamentals: economic growth, inflation trends, and central bank policy. One of our key convictions is maintaining an overweight position in short‑term Canadian bonds, such as two and five year government securities. These areas of the market offer an attractive balance of income, capital stability, and potential upside if rates move lower.

Emerging markets continue to be a core conviction. Opportunities in Latin America remain compelling, supported by favourable geopolitical tailwinds, improving carry dynamics, and resilient market behaviour during recent risk‑off episodes. Local‑currency exposure remains concentrated in higher‑conviction markets, including Brazil, Mexico and Chile, with Brazil currently the largest individual EM allocation following strong currency performance and continued positive investor flows. We reduced exposure to longer‑dated Mexican Bonos, which had performed well on a spread basis, and rotated toward shorter‑dated instruments and money market securities. This shift reflects the view that while emerging market currencies remain attractive, keeping duration risk aligned with a cautious stance on U.S. rates is prudent given elevated global rate correlations

Within developed markets, duration exposure remains underweight, particularly at the long end of the U.S. curve. Positioning in Australian rates has been reassessed following recent changes in market pricing and central bank expectations, while maintaining a cautious stance on global curve re‑steepening themes. Overall, positioning reflects a balanced approach focused on carry, diversification and disciplined risk management.

Central Bank Watch

Region | Latest CPI Inflation | Policy rate | Latest policy action | Next decision date | Market expectation | Outlook |

Canada | 2.40% | 2.25% | No change | 18-Mar-26 | No change | Neutral |

United States | 2.70% | 3.75% | No change | 18-Mar-26 | No change | Underweight |

Eurozone | 1.90% | 2.15% | No change | 19-Mar-26 | No change | Underweight |

Japan | 2.10% | 0.75% | No change | 19-Mar-26 | No change | Underweight |

Australia | 3.20% | 3.85% | 25 bp hike | 16-Mar-26 | No change | Overweight |

Credit Market Performance

U.S. leveraged loans started the year strongly but reversed sharply late in January as a sell‑off driven by high concentrations in software and technology‑related issuers (12%), where stretched valuations, heavy sponsor ownership, and elevated leverage left the sector vulnerable to a reset in risk sentiment. in technology equities driven by softer earnings signals and growing skepticism around near‑term AI benefits spilled into credit markets. Performance across borrower credit ratings highlighted a clear flight to quality in January. BB rated loans (~22% of the market) were the most resilient and finished the month slightly positive at +6 bps, B rated loans (~62% of index), declined 39 bps, while lower‑quality CCC loans underperformed sharply by 1.33% as risk aversion increased.

In contrast, high yield bonds performed positively over the same period, highlighting a clear divergence within below‑investment‑grade credit. Performance dispersion across sectors and ratings buckets remains high, reinforcing the importance of active security selection. High-yield bonds performance was led by CCCs (+0.72%), followed by BBs (+0.58%) and single Bs (+0.48%). At the sector level, Energy was the strongest performer, followed by Chemicals and Telecom. In contrast, Paper/Packaging (-1.76%) and Technology (-0.33%) lagged during the month.

Against this backdrop, the portfolio remained resilient and delivered relative outperformance. While the broader loan universe declined over the month, portfolio performance was broadly flat, reflecting a positioning that prioritised credit quality and avoided the most crowded and vulnerable areas of the market.

This resilience was driven primarily by what the portfolio did not own. Coming into the period, the portfolio was underweight software and technology‑heavy loan exposure, particularly in highly leveraged, sponsor‑owned issuers that have been most exposed to recent volatility. Similarly, we remained underweight several large benchmark names and participated selectively in primary market activity, avoiding aggressive repricing that later came under pressure.

Index | Yield | Yield m/m | Spread | Spread m/m | Performance (%) | |||

bp | bp | bp | 1m | 3m | YTD | 1Y | ||

Investment Grade | ||||||||

CA | 3.91% | -10 | 83 | -6 | 0.9 | 0.5 | 0.9 | 4.2 |

US | 4.89% | 1 | 75 | -4 | 0.4 | 0.7 | 0.4 | 7.5 |

High Yield |

|

|

|

|

|

|

|

|

CA | 6.62% | -1 | 249 | 6 | 0.4 | 1.5 | 0.4 | 7.1 |

US | 7.11% | 3 | 288 | 7 | 0.5 | 1.6 | 0.5 | 7.5 |

US Leverage Loans | 8.0% | 17 | 417 | 23 | -0.3 | 0.7 | -0.3 | 4.9 |

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns as of Jan 31, 2026, including changes in share value and reinvestment of all distributions and does not take into account sales, redemption, distribution, or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated. Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in the investment products that seek to track an index.

Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in investment products that seek to track an index.

This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of Jan 31, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

The content of this commentary (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

All information is historical and not indicative of future results. Current performance may be lower or higher than the quoted past performance, which cannot guarantee results. Share price, principal value, and return will vary, and you may have a gain or a loss when you sell your shares. Performance assumes reinvestment of distributions and does not account for taxes. Performance may not reflect any expense limitation or subsidies currently in effect. Short-term trading fees may apply.

This material is for informational and educational purposes only. It is not a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. It is not intended to address the needs, circumstances, and objectives of any specific investor. Mackenzie Investments, which earns fees when clients select its products and services, is not offering impartial advice in a fiduciary capacity in providing this sales and marketing material. This information is not meant as tax or legal advice. Investors should consult a professional advisor before making investment and financial decisions and for more information on tax rules and other laws, which are complex and subject to change.

The rate of return is used only to illustrate the effects of the compound growth rate and is not intended to reflect future values of the mutual fund or returns on investment in the mutual fund.