Written by the Mackenzie Fixed Income Team

Key Highlights

- Geopolitical tensions rise with U.S. intervention in Venezuela, aiming to curb Chinese and Russian influence. Market volatility remains low, but any shock could have an outsized impact given the current calm backdrop.

- Risk of Fed autonomy erosion could weaken the U.S. dollar and push long-term rates higher, though probability remains low.

- Eurozone inflation surprises to the downside, giving ECB room to stay patient; Japan leans toward rate hikes. Monitoring European defense spending trends; considering deeper underweight in European bonds.

- Neutralized short U.S. Treasury position amid upcoming data and geopolitical uncertainty. Established outright long position in Australian government bonds, supported by RBA’s dovish stance.

- Remain constructive on Latin America; recent Venezuelan developments seen as stabilizing for the region. Took profits on Peru and South Africa positions; actively evaluating new EM opportunities.

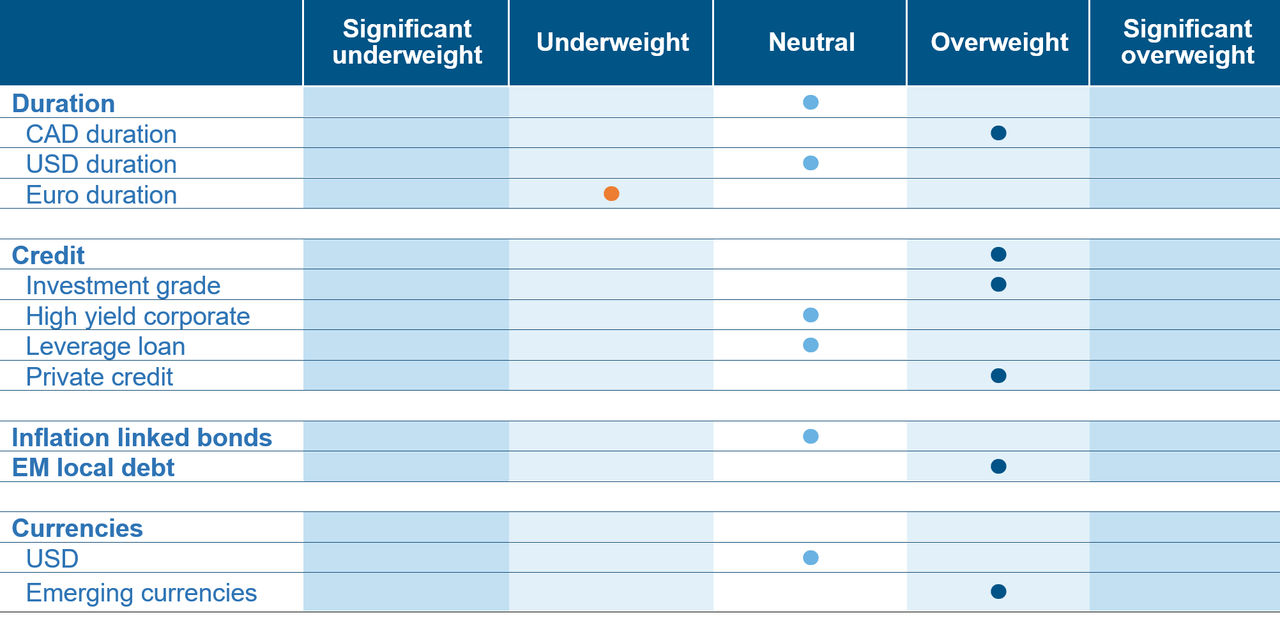

Fixed Income Team Views

Source: Mackenzie Investments. As of December 31, 2025.

Source: Mackenzie Investments. As of December 31, 2025.

Fixed Income Market Update

A Happy New Year to all. The start of the year has been marked by significant geopolitical developments, most notably the U.S. intervention in Venezuela. This action appears to be driven by several strategic goals, including containing Chinese and Russian influence in the Western Hemisphere, disrupting oil supplies to both China and Cuba, and potentially boosting the U.S. oil industry. While this has created headlines, the immediate market reaction has been relatively contained. Oil prices have been volatile but have not seen a sustained move in one direction, and major government bonds remained in a stable range.

This intervention is also seen as a move to give the U.S. leverage in trade negotiations, particularly concerning the USMCA (United States-Mexico-Canada Agreement). For Canada, which exports a significant amount of heavy crude to the U.S. Gulf Coast, the potential for renewed Venezuelan supply presents a competitive challenge, though initial concerns may be overstated as the direct overlap is limited. We are also monitoring other geopolitical hotspots, such as the potential for increased U.S.-Iran tensions and renewed calls for the U.S. to acquire Greenland, which could have ripple effects on global stability and trade alliances.

There is a concern, albeit a remote one, that pressure could be exerted on the independence of the U.S. Federal Reserve. An erosion of the Fed's autonomy could lead to a weaker U.S. dollar and higher long-term interest rates. While institutional checks and balances make this a low-probability scenario, it is a risk that cannot be entirely dismissed.

On the economic front, the data has been mixed. In the U.S., the ISM manufacturing index pointed to a slowdown in the factory sector, however, the services sector remains robust, with the ISM Services index showing surprisingly strong growth. The labor market will be the key focus for the week, to provide a crucial update on the health of the U.S. economy.

Elsewhere, inflation in the Eurozone came in lower than expected, giving the European Central Bank room to remain patient. In Japan, the central bank maintains a bias towards raising interest rates as its economy and inflation improve.

Fund Positioning

Our core view has been that U.S. economic growth would remain firm, potentially leading to higher inflation and interest rates. As such, we held a short position in U.S. Treasuries (profiting from a rise in rates). However, given the significant amount of upcoming economic data being released and the unpredictable nature of geopolitical events, we have tactically neutralized this position to reduce risk, and we will look for opportunities to re-engage.

We are constructive on Australian bonds and have established a long position. We have a long position in Australian government bonds. This trade was initially structured as a spread, where we were long Australian bonds and short U.S. bonds. Now that we have closed the U.S. side, it stands as an outright long position. We believe a lot of negative sentiment is already reflected in Australian bond prices, and the Reserve Bank of Australia has recently made comments suggesting they will be patient with inflation, signaling less appetite for aggressive rate hikes. This more dovish stance is supportive for bond prices. In Europe, we are closely watching the trend of increased defense spending, which could lead to higher bond yields, and we are considering increasing our underweight position in European government bonds.

We remain positive on Emerging Markets, particularly in Latin America. The recent developments in Venezuela are seen as a net positive for the stability of the region, reducing risk for countries like Brazil and Mexico. We have held positions in both markets. We have recently taken profits on our positions in Peru and South Africa and are continuously evaluating new opportunities.

We saw major global events unfold over the last year, and while they caused brief spikes in volatility, these episodes were short-lived. The market has shown remarkable resilience, quickly reverting to a calm state. This creates a paradox for investors. The low starting point for volatility means that any shock is likely to have an outsized impact, suggesting the path of least resistance for volatility is upwards.

Central Bank Watch

Region | Latest CPI Inflation | Policy rate | Latest policy action | Next decision date | Market expectation | Outlook |

Canada | 2.20% | 2.25% | No change | 28-Jan-26 | No change | Overweight |

United States | 3.00% | 3.75% | 25 bp cut | 28-Jan-26 | No change | Neutral |

Eurozone | 2.10% | 2.15% | No change | 05-Feb-26 | No change | Underweight |

Japan | 3.00% | 0.75% | 25 bp hike | 23-Jan-26 | No change | Underweight |

Australia | 3.20% | 3.60% | No change | 03-Feb-26 | No change | Overweight |

Credit Market Performance

The high-yield market concluded the year with impressive momentum fueled by a less-hawkish-than-feared outcome from the Federal Reserve, which allowed yields to approach their cycle lows. Resilient macroeconomic data supported this risk-on sentiment, with spreads tightening to three-month lows. Investor appetite was evident in strong inflows and a clear preference for lower-quality credit; CCC-rated bonds (+1.00%) significantly outperformed their BB-rated (+0.45%) counterparts. However, sector dispersion remained a key theme, underscoring the need for careful selection. While areas like Gaming & Leisure (+1.22%) performed strongly, the Retail sector (-0.96%) faced significant headwinds. This environment highlights a market rewarding risk, but one where fundamental weakness in specific sectors cannot be ignored.

The US leveraged loan market performance was primarily driven by strong interest income that successfully countered weaknesses in the secondary market. However, with interest rates declining, the appeal of floating-rate loans diminished, causing their performance to trail behind high yield bonds. A flight to quality was evident, with higher-rated loans outperforming their lower-rated counterparts. Performance varied significantly across sectors; cyclical industries like automotive components saw declines, while areas such as media, healthcare, and utilities showed robust returns. In December, the US leveraged loan market demonstrated resilience, expanding to a new record size of $1.55 trillion. Strong demand from institutional investors, through Collateralized Loan Obligations (CLOs), continued to bolster the market, offsetting the trend of individual retail investors withdrawing funds. Default rates continued their downward trend, signaling a healthier credit environment. Despite a slight slowdown in new loan issuance compared to previous months, the market's fundamentals remain solid. For investors, loans continue to offer attractive yields compared to high-yield bonds, representing good relative value.

Index | Yield | Yield m/m | Spread | Spread m/m | Performance (%) | |||

bp | bp | bp | 1m | 3m | YTD | 1Y | ||

Investment Grade | ||||||||

CA | 4.01% | 17 | 89 | -4 | -0.6 | 0.4 | 4.3 | 4.3 |

US | 4.88% | 6 | 79 | -3 | -0.3 | 0.5 | 7.8 | 7.8 |

High Yield |

|

|

|

|

|

|

|

|

CA | 6.63% | -12 | 243 | -20 | 0.6 | 1.4 | 7.8 | 7.8 |

US | 7.08% | -5 | 281 | -11 | 0.7 | 1.3 | 8.5 | 8.5 |

US Leverage Loans | 7.86% | -21 | 394 | -5 | 0.6 | 1.2 | 5.9 | 5.9 |

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns as of Dec 31, 2025, including changes in share value and reinvestment of all distributions and does not take into account sales, redemption, distribution, or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated. Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in the investment products that seek to track an index.

Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in investment products that seek to track an index.

This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of Dec 31, 2025. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

The content of this commentary (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

All information is historical and not indicative of future results. Current performance may be lower or higher than the quoted past performance, which cannot guarantee results. Share price, principal value, and return will vary, and you may have a gain or a loss when you sell your shares. Performance assumes reinvestment of distributions and does not account for taxes. Performance may not reflect any expense limitation or subsidies currently in effect. Short-term trading fees may apply.

This material is for informational and educational purposes only. It is not a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. It is not intended to address the needs, circumstances, and objectives of any specific investor. Mackenzie Investments, which earns fees when clients select its products and services, is not offering impartial advice in a fiduciary capacity in providing this sales and marketing material. This information is not meant as tax or legal advice. Investors should consult a professional advisor before making investment and financial decisions and for more information on tax rules and other laws, which are complex and subject to change.

The rate of return is used only to illustrate the effects of the compound growth rate and is not intended to reflect future values of the mutual fund or returns on investment in the mutual fund.