Monthly commentary - Mackenzie Fixed Income Team

IN THIS ARTICLE min read

Written by the Mackenzie Fixed Income Team

Key Highlights

- Markets are underestimating the persistence of inflation, with structurally tighter oil supply implying a more durable shift in the inflation and rate regime.

- Higher oil prices are expected to push inflation back higher, keeping policy restrictive for longer even without a new hiking cycle.

- In the U.S., the key risk is stronger-than-expected labor data poses the key upside risk to rates, with potential for rapid repricing at the front end.

- The portfolio has added tactical long-end Canada duration tied to index extension demand and is positioned via front-end receiver swaptions for eventual BoC cuts.

- Globally, Europe is positioned for further curve flattening amid ECB tightening in a weak growth backdrop, Japan remains tactically underweight duration, and an Australia–U.S. spread trade has been exited.

- Positioning remains defensive in credit while expressing relative value through FX (long NOK vs CAD) and selective emerging market exposure (Brazil & Mexico).

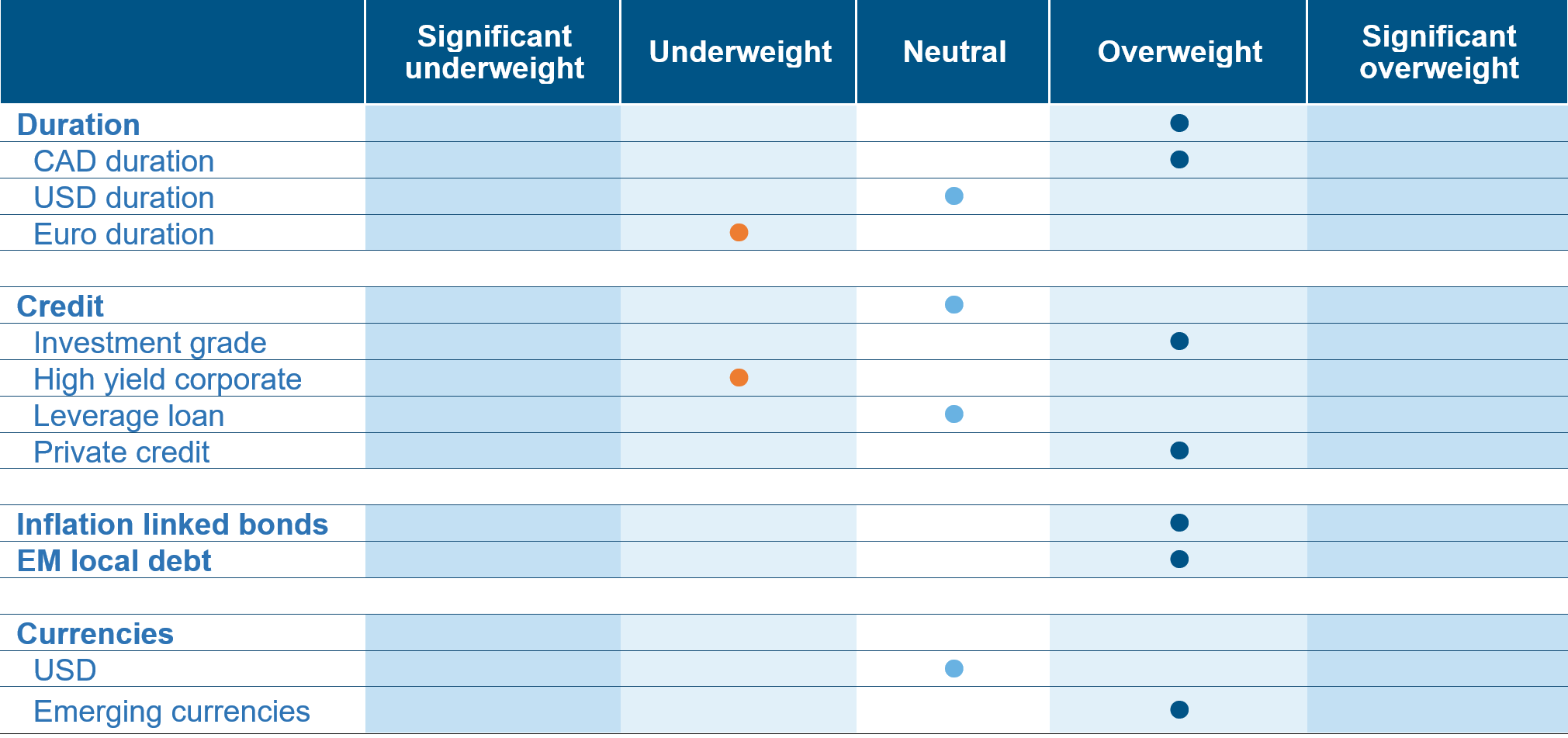

Fixed Income Team Views

Source: Mackenzie Investments. As of Apr 30, 2026.

Source: Mackenzie Investments. As of Apr 30, 2026.

Fixed Income Market Update

Team’s macro view highlights a growing disconnect between inflation risks and how markets are currently pricing them, alongside meaningful downside risks to growth that are not fully appreciated. The team remains cautionary as higher oil prices should not be treated as noise or a transitory macro headwind. Instead, they represent a durable shift in the inflation and rates backdrop, demanding recalibration across asset classes rather than a simple expectation of mean reversion. Constrained supply growth and geopolitical disruptions have made energy markets structurally tighter, increasing the likelihood that oil prices remain elevated for an extended period.

From a macroeconomic standpoint, higher oil prices directly complicate the inflation outlook. Energy costs feed through not only into headline inflation but also into goods, transportation, and services, making disinflation harder to sustain. This broad pass‑through makes it difficult to achieve a durable decline in inflation, complicating the policy environment. Markets may be underestimating how long policy rates stay restrictive in such an environment. Inflation remains firm, with core measures already around 3% and likely to move higher as energy feeds through. However, we do not believe this necessarily leads to a sustained hiking cycle.

In the U.S., we see a realistic path for rates to be driven more by strong labor market data (e.g., a hot non-farm payrolls print) than by inflation data itself. The key “surprise factor” for markets is not inflation, which is already well understood, but the possibility that the economy, particularly the labor market, remains stronger than expected. This divergence between expectations and realized data could lead to a rapid repricing of short-end rates.

For Canada, the backdrop is more complex. The economy faces simultaneous pressures: inflation risks, housing vulnerabilities, and uncertainty around trade (including CUSMA). We do recognize the risk of a stagflationary type environment, where short-term rates rise even as long-term growth concerns weigh on the outlook. In such a scenario, policy mistakes, particularly hiking into structural weaknesses like housing, would create significant market dislocations. Our base case for Canada remains one to two rate cuts, reflecting a belief that growth risks ultimately dominate. We believe that downside risks to growth are underappreciated, while near-term pricing risks skew toward potential hawkish repricing. This creates an environment prone to sharp market reactions and dislocations, particularly if policy expectations shift quickly. While uncertain about exact outcomes, such volatility would create substantial opportunities across fixed income and macro strategies.

Fund Positioning

On rates, the portfolio has added modest long-end Canadian duration (30-year bonds), driven by a technical, time-bound opportunity linked to anticipated demand ahead of the index extension and limited near-term supply. This is framed as an asymmetric trade, with expectations of support at current yield levels and a defined exit window. The portfolio maintains a tactical bias using receiver swaptions on the front end, reflecting the view that the Bank of Canada may ultimately be forced to cut rates. These option-based positions allow for efficient exposure without significant capital deployment.

Inflation protection is present but limited (~2% in 5-year TIPS), with potential to increase. Inflation-linked exposure is expressed tactically via short-duration US TIPS, aimed at capturing near-term CPI indexation benefits rather than taking a directional duration view. This position is limited in size and contributes minimal overall duration risk.

In Europe, the portfolio retains an underweight duration stance, particularly at the long end, although this position is being actively reduced with a view to potentially turning long. The evolving macro backdrop, characterized by rising inflation pressures, weakening business confidence, and limited fiscal impulse supports the expectation that the ECB may tighten policy further, even in a low-growth environment. This dynamic is expected to drive curve flattening, in contrast to earlier steepening positioning tied to fiscal expansion expectations in Germany, which have yet to materialize. In Japan, the strategy remains underweight duration, a position that contributed positively to April performance. An Australia-US rates spread trade was previously implemented to isolate Australian rate dynamics but has since been closed after delivering limited impact.

Within FX, a notable allocation is the long NOK versus CAD trade, reflecting expected mean reversion between the two petrocurrencies. The position is supported by Norway’s more hawkish rate backdrop, stronger fiscal linkage to oil prices, and more favourable macro starting conditions relative to Canada. The trade is structured with a longer term horizon, defined return expectations, and disciplined stop-loss levels, and has already generated positive returns since initiation.

In emerging markets, positioning favours Brazil over Mexico, primarily due to the higher real yield cushion in Brazil. While Mexico may be approaching the end of its easing cycle, its lower real rates reduce its relative attractiveness. Exposure to Chile has been exited, as the oil-driven macro environment has dominated and invalidated the earlier commodity-linked thesis tied to copper.

From a credit perspective, the portfolio remains positioned defensively. Lower duration exposure via floating-rate instruments and private credit has been a key contributor to performance. Floating-rate assets performed strongly, and private credit continues to deliver stable returns despite broader market concerns. Credit selection has avoided major idiosyncratic losses.

Central Bank Watch

Region | Latest CPI Inflation | Policy rate | Latest policy action | Next decision date | Market expectation | Outlook |

Canada | 2.40% | 2.25% | No change | 10-Jun-26 | No change | Overweight |

United States | 3.30% | 3.75% | No change | 17-Jun-26 | No change | Underweight |

Eurozone | 3.00% | 2.15% | No change | 11-Jun-26 | Rate hike | Underweight |

Japan | 1.50% | 0.75% | No change | 16-Jun-26 | No change | Underweight |

Australia | 3.20% | 4.35% | 25 bp hike | 16-Jun-26 | No change | Neutral |

Credit Market Performance

High yield bonds provided strong gains in April, with lower quality credits outperforming as the asset class benefitted from a rally in equities (S&P500 +10.5% m/m) amid receding geopolitical tensions with US/Iran reaching a temporary ceasefire deal. Meanwhile, spreads tightened 40bp to a 2.5-month low as the product was also supported by a solid start to earnings season, active capital markets, and robust inflows. Outperformers in April included Telecom (+2.80%) and Media (+2.30%) with Cable/Sat. (+0.86%) and Transportation (+0.89%) lagging.

Leveraged loans delivered a strong performance in April amid risk-on conditions, bringing year-to-date returns into positive territory. Performance remained bifurcated, particularly within software and technology, with B and CCC rated credits outperforming. Despite lower volatility, markets continued to focus on themes such as AI disruption, tariffs, inflation, growth, and geopolitics. Lower-quality credits led gains, while higher-quality loans lagged. Defaults remained low, and overall default trends showed improvement.

Index | Yield | Yield m/m | Spread | Spread m/m | Performance (%) | |||

bp | bp | bp | 1m | 3m | YTD | 1Y | ||

Investment Grade | ||||||||

CA | 4.2% | 0 | 89 | -4 | 0.6 | -0.2 | 0.7 | 3.8 |

US | 5.2% | -2 | 82 | -8 | 0.9 | -0.2 | 0.1 | 5.5 |

High Yield |

|

|

|

|

|

|

|

|

CA | 7.0% | -11 | 270 | -21 | 1.5 | -0 | 0.4 | 7.3 |

US | 7.3% | -33 | 283 | -45 | 2.3 | 0.7 | 1.1 | 8.7 |

US Leverage Loans | 8.1% | -20 | 428

| -17 | 1.3 | 1.0 | 0.7 | 6.2 |

Source: Bloomberg, as of 30 Apr 2026, performance is reflective of ICE BoFA indices local returns.

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns as of Apr 30, 2026, including changes in share value and reinvestment of all distributions and does not take into account sales, redemption, distribution, or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated.

Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in investment products that seek to track an index.

This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties, and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and do not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of Apr 30, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

The content of this commentary (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

All information is historical and not indicative of future results. Current performance may be lower or higher than the quoted past performance, which cannot guarantee results. Share price, principal value, and return will vary, and you may have a gain or a loss when you sell your shares. Performance assumes reinvestment of distributions and does not account for taxes. Performance may not reflect any expense limitation or subsidies currently in effect. Short-term trading fees may apply.

This material is for informational and educational purposes only. It is not a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. It is not intended to address the needs, circumstances, and objectives of any specific investor. Mackenzie Investments, which earns fees when clients select its products and services, is not offering impartial advice in a fiduciary capacity in providing this sales and marketing material. This information is not meant as tax or legal advice. Investors should consult a professional advisor before making investment and financial decisions and for more information on tax rules and other laws, which are complex and subject to change.

The rate of return is used only to illustrate the effects of the compound growth rate and is not intended to reflect future values of the mutual fund or returns on investment in the mutual fund.