Written by the Mackenzie Fixed Income Team

Key Highlights

- Jerome Powell’s Jackson Hole speech marked a clear shift in Fed priorities, emphasizing labour market vulnerabilities over inflation concerns. This pivot sets the stage for a likely September rate cut.

- The path of future rate cuts hinges on how tariff-related costs are absorbed or passed on. Limited pass-through and cooling services inflation would support continued easing; otherwise, the pace may slow.

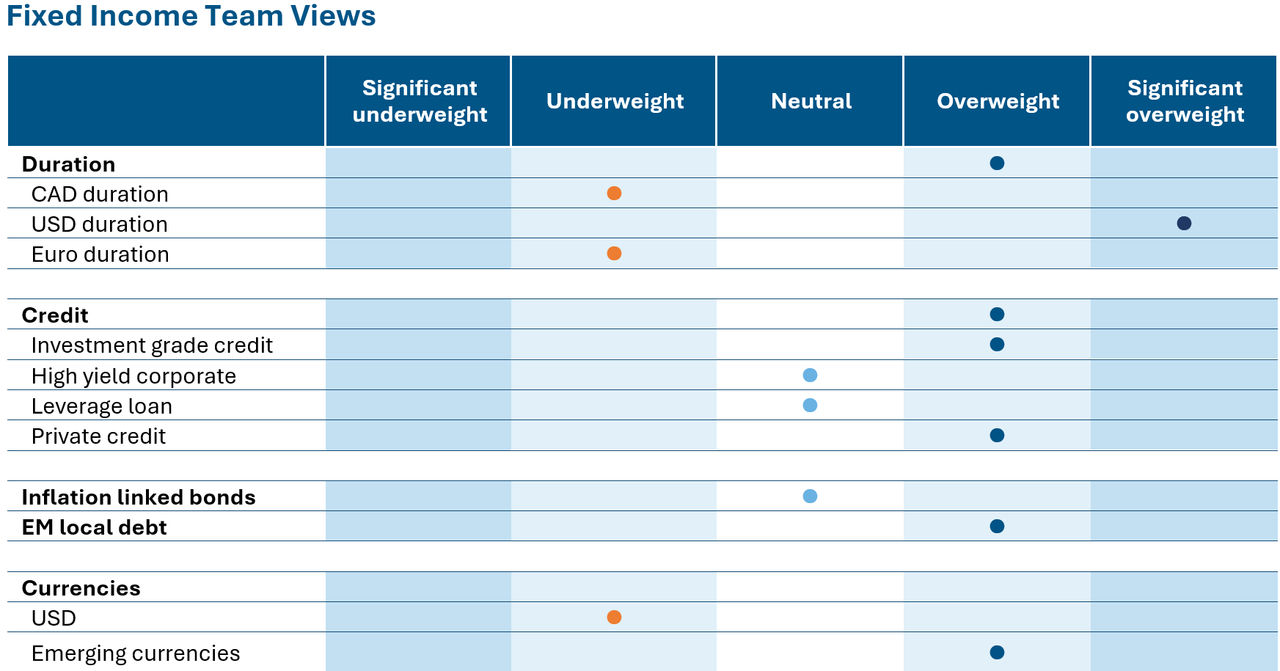

- The portfolio remains overweight U.S. duration, reflecting a successful thesis on narrowing U.S.-Canada yield spreads. With much of the compression realized, tactical reassessment is underway.

- The global portfolios saw exits from long TIPS and New Zealand duration positions due to valuation and macro shifts.

- Exposure was added to high real yield EMs like South Africa and Peru, while Indonesia was exited ahead of currency and political volatility, demonstrating proactive risk management.

Source: Mackenzie Investments. As of Aug 31, 2025.

Source: Mackenzie Investments. As of Aug 31, 2025.

Fixed Income Market Update

Fed Chair Jerome Powell used his final speech at Jackson Hole to signal that the balance of risks has shifted away from inflation and toward the labour market, effectively teeing up a September rate cut. He reiterated the 2% inflation target but stressed that employment risks can emerge suddenly, warning that “if those risks materialize, they can do so quickly in the form of sharply higher layoffs and rising unemployment.” Markets immediately translated this framing into higher odds of a 25 bp move, lower front-end yields, a softer USD, and higher equity prices. While Powell stopped short of a pre-commitment, the shift was clear: the Fed is now inclined to prioritize protecting the labour market over pressing harder on inflation. This marks a sharp contrast with the tone of the July FOMC Minutes, which suggested policymakers still viewed inflation as the greater threat. The result was a swift repricing: rate cut odds for September jumped to nearly 90% and reversing the more hawkish interpretation investors had taken from July’s inflation data.

The immediate debate is no longer about whether the Fed will cut in September, but rather whether it can continue cutting thereafter. Markets currently expect four cuts by June 2026, but the trajectory hinges on tariff pass-through. So far, companies have absorbed the bulk of the costs. While broad consumer pass-through related to tariffs has been largely avoided so far, eventual price pass through may be inevitable if tariffs remain elevated. Powell’s framing fits neatly into this backdrop. He acknowledged tariff pressures but framed them as one-off price adjustments rather than a sustained inflation cycle. The policy hinge is simple: if companies shift more decisively from absorption to pass-through while non-housing services remain sticky, the glidepath back to 2% inflation will slow and the easing cycle could be shallower than markets currently expect. If pass-through remains limited and services cool, the Fed has room to cut in September and proceed cautiously thereafter.

The key takeaway from Jackson Hole is that a key risk that the Fed falling behind the curve has been sidelined for now. Policymakers have made it clear that they are prepared to run the economy hot if that is the cost of protecting the labour market. September looks locked in for the first cut, but what comes after will depend on how tariffs filter through prices and how the labour market evolves in the months ahead.

Fund Positioning

Our broad duration stance remains overweight, but we have made meaningful adjustments at the regional level. We hold underweight positions in Canadian and European duration, while maintaining a significant overweight in U.S. duration.

One of our core fixed income positioning themes this year has been the anticipated narrowing of the yield spread between U.S. and Canadian 10-year government bonds. Earlier in the year, the differential had widened to ~140bps, a level that stood out as historically extreme, reaching 2.5 to 3 standard deviations depending on the timeframe. We viewed this as unsustainable and positioned for convergence. Our thesis was that the spread would compress primarily via lower U.S. yields, driven by a shift in Fed policy focus toward labour market softness rather than inflation persistence. At the same time, Canadian yields were expected to remain stable or drift higher, given the Bank of Canada’s earlier and more aggressive rate cuts from a higher peak. This view has largely played out, with the spread narrowing to ~80bps, in line with our initial target range. The recent pivot in U.S. rate expectations, particularly over the past 4–6 weeks, has accelerated this move. Markets are now pricing in a more responsive Fed, potentially cutting rates sooner than previously anticipated.

While the U.S. and Canadian economies have not moved in lockstep, they are showing signs of convergence. That said, we remain cautious on the macro outlook for both regions over the next few quarters. U.S. fundamentals, especially household balance sheets, remain stronger, supported by long-term mortgage structures and post-GFC deleveraging. In contrast, Canadian households are more exposed to rate resets and carry higher leverage, making the consumer more vulnerable to volatility. We continue to monitor this cross-market dynamic closely, but with much of the spread compression already realized, we are tactically reassessing the next leg of opportunity.

We made several tactical adjustments across our global fixed income and FX exposures in August, driven by evolving macro conditions, valuation signals, and geopolitical developments. We exited our long TIPS exposure, primarily due to a lack of near-term inflation pressure and muted market reaction to CPI prints. However, with real yields remaining elevated, we remain open to re-entering the position tactically should inflation dynamics or valuation warrant it. We closed our long New Zealand duration exposure, as we believe the trade has largely played out. The convergence of global policy rate paths has reduced the relative value opportunity. One of our more successful trades this month was selling French OATs versus German Bunds in the 10-year segment. This was based on rising political and fiscal uncertainty in France, including risks of government instability, budget rejection cycles, and potential early elections. The trade performed ahead of expectations, validating our thesis that French assets were mispricing these risks.

On the EM front, we selectively added to carry positions focusing on countries viz. South Africa and Peru with high real yields and improving fundamentals. In Indonesia we exited our position in Indonesia ahead of recent currency volatility and political unrest which proved to be well timed.

Central Bank Watch

Region | Latest CPI Inflation | Policy rate | Latest policy action | Next decision date | Market expectation | Outlook |

Canada | 1.70% | 2.75% | No change | 17-Sep-25 | Rate cut | Underweight |

United States | 2.90% | 4.50% | No change | 17-Sep-25 | Rate cut | Overweight |

Eurozone | 2.10% | 2.15% | No change | 30-Oct-25 | No change | Neutral |

Japan | 3.10% | 0.50% | No change | 19-Sep-25 | No change | Underweight |

New Zealand | 2.70% | 3.00% | 25 bp cut | 07-Oct-25 | Rate cut | Neutral |

United Kingdom | 3.80% | 4.00% | 25 bp cut | 17-Sep-25 | No Change | Neutral |

Credit market performance

The high yield bond index posted +1.3% gain in August with CCCs (+1.6%) outperforming BBs (+1.3%) and Bs (+1.1%). This strength came alongside a notable rally in treasuries and rise in equities, as markets responded to a more dovish outlook for Fed policy amid signs of a cooling labour market. HY yields remain near multi-year lows, with spreads holding steady through the month. Investors absorbed a solid earnings season, consistent primary issuance, and modest inflows with confidence. Notably, this has been one of the strongest reporting seasons in recent years for high-yield issuers, with forward guidance also coming in robust across sectors.

The U.S. leveraged loan market paused in August, with the Morningstar LSTA Index returning 0.45% as secondary prices softened and investor sentiment turned more cautious. Lower rated loans underperformed as CCC loans fell 0.76% while BB rate gained 0.50%. Heavy issuance in July, softer macro data, and subdued BSL CLO formation weighed on returns. However, strong repayment activity reaching a record $54 billion, helped maintain borrower-friendly technicals and underscored investors’ continued need to deploy capital.

Index | Yield | Yield m/m | Spread | Spread m/m | Performance (%) | |||

bp | bp | bp | 1m | 3m | YTD | 1Y | ||

Investment Grade | ||||||||

CA | 4.1% | 0 | 89 | -13 | 0.0 | 1.2 | 2.2 | 6.0 |

US | 5.1% | +6 | 79 | -7 | 0.1 | 2.0 | 4.4 | 4.7 |

High Yield |

|

|

|

| ||||

CA | 6.2% | -9 | 283 | -25 | 0.8 | 3.0 | 3.9 | 8.8 |

US | 7.3% | -3 | 286 | -10 | 0.4 | 4.0 | 5.0 | 8.6 |

US Leverage Loans | 8.3% | 0 | 391 | 0 | 0.5 | 2.1 | 4.2 | 7.3 |

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns as of Aug 31, 2025, including changes in share value and reinvestment of all distributions and does not take into account sales, redemption, distribution, or optional charges or income taxes payable by any security holder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated.

Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in investment products that seek to track an index.

This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of Aug 31, 2025. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

The content of this commentary (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

All information is historical and not indicative of future results. Current performance may be lower or higher than the quoted past performance, which cannot guarantee results. Share price, principal value, and return will vary, and you may have a gain or a loss when you sell your shares. Performance assumes reinvestment of distributions and does not account for taxes. Performance may not reflect any expense limitation or subsidies currently in effect. Short-term trading fees may apply.

This material is for informational and educational purposes only. It is not a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. It is not intended to address the needs, circumstances, and objectives of any specific investor. Mackenzie Investments, which earns fees when clients select its products and services, is not offering impartial advice in a fiduciary capacity in providing this sales and marketing material. This information is not meant as tax or legal advice. Investors should consult a professional advisor before making investment and financial decisions and for more information on tax rules and other laws, which are complex and subject to change.

The rate of return is used only to illustrate the effects of the compound growth rate and is not intended to reflect future values of the mutual fund or returns on investment in the mutual fund.