Why a stakeholder lens is key to tapping the world’s $13 trillion

sustainable opportunity

#BlackLivesMatter. #MeToo. #ClimateChangeIsReal. These aren’t just social media hashtags - they each represent a global movement pushing for a better world by addressing systemic racism, climate change, and societal inequities. Collectively, they send a clear message: the status quo is no longer tenable. We need positive change for the better, and fast. We believe that companies that heed the call for change will thrive. Those that continue along the same path they’ve followed in the past will not.

How companies treat the planet and the communities they operate in will determine their future profitability. It’s not just wishful thinking - it’s a fact. More and more data are emerging linking sustainable business practices to value creation for shareholders. And that represents a challenge for investors who are not incorporating these factors into their company assessment process.

The hallmarks of sustainable value creation simply aren’t reflected on company financial statements - or even by broad-based, third-party sustainability ratings. Rather, investors looking to build sustainable portfolios will need a new lens for assessing value creation. And we believe this new lens on long-term sustainability must be stakeholder focused.

Here’s why.

The trillion-dollar change

Ready or not, positive change is on the way – backed by trillions of dollars. The United Nations 2030 Agenda for Sustainable Development has scoped out a clear set of 17 goals for addressing the growing global crises of poverty, inequality, and climate change. Getting there will require a massive private sector commitment of US$5 trillion per year until 2030 (to the tune of $50 trillion between 2020 and 2030).1 In addition, investors are now expected to redirect existing capital to be good stewards of the companies they invest in and contribute to a sustainable future.

A group of Canada’s top pension plans2 - representing CDN$1.6 trillion in assets - has heeded the call. In 2020, they collectively and publicly urged investment managers and the companies they invest in to provide consistent and complete environmental, social and governance (ESG) information to strengthen their decision-making and contribute to more sustainable and inclusive economic growth.

Right now, there are trillions of dollars of capital seeking companies that support and contribute to positive environmental, social, and governance changes globally.

As that happens, it is reshaping the investment world and how investors build portfolios.

Values alignment vs. the bottom line

The future of portfolio construction

Sustainable funds are no longer just a nice to have – they are fast becoming the future of portfolio construction, moving from the niche and into the core. According to Casey Quirk, global sustainable funds are on track to exceed US$13 trillion by 2025.3

It’s not just about doing good - it’s about exposure to emerging and powerful changes to the global economy. The massive global transition to clean energy, for example, is creating opportunities for an entirely new generation of companies that can provide low carbon energy alternatives to power our future.

Energy isn’t the only sector to watch. Sustainable funds are outperforming relative to broad indices across most other sectors according to data from Morningstar4.

This level of outperformance shouldn’t come as a surprise. A recent McKinsey5 study found companies that focus on ESG factors generate better cash flow by facilitating topline growth, reducing costs, minimizing regulatory and legal interventions, increasing employee productivity, and optimizing investment and capital expenditures6. That makes a lot of sense when you consider how stakeholders such as consumers, regulators and employees perceive companies that exhibit sustainable practices throughout their business.

Consider that:

Inside out - the stakeholder lens

So, what is the best way to assess the value creation of a company’s ESG or sustainable practices?

Turn it inside out. Ask how a company is viewed by its external and internal stakeholders and you’ll get a good picture of what’s going on inside and how it views its stewardship role. How does it treat the communities it operates in? Its employees? The environment?

Financial statements rarely if ever answer these questions - and yet the answers are essential indicators of whether a company’s revenues will be sustainable over the long term. Gaining an understanding of how a company is perceived by stakeholders can ensure its practices are aligned with those of long-term asset owners - and that those companies are focused on creating value, not destroying it.

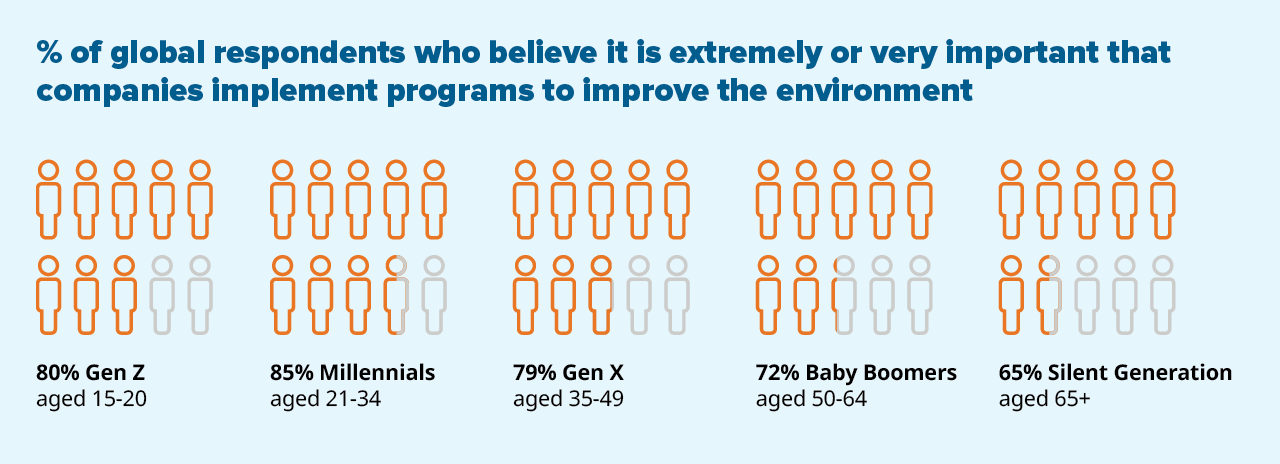

The chart below outlines the percentage of global respondents who say it is “extremely or very important that companies implement programs to improve the environment”.10

According to the Mackenzie Betterworld Team, the stakeholder lens is specifically focused on:

Corporate governance - Companies with poor governance practices create inherent risks for shareholders. Consider the negative blowback triggered by Air Canada’s decision during the pandemic to award its executives with $10 million in compensation while also laying off its workers.

Diversity, equity, and inclusion - Companies must be working to become more diverse and inclusive. For example, among Fortune 500 companies in the U.S., black professionals account for just 0.8% of CEO positions.11 And only 26% of S&P 500 board seats are held by women.12

Community relations - Poor community relations are a risk to a company’s reputation and its profitability. According to a survey by Deloitte, companies that had previously experienced a negative reputation event reported a 41% loss of revenue and a 41% loss of brand value.13

Human Rights - Companies that engage in poor human rights practices can reflect poorly on their investors. In 2019, the Canada Pension Plan Investment Board attracted negative attention for its investment in companies hired to detain people suspected of entering the U.S. illegally - including separating parents from their children. Reputational risk is real.

Product sustainability - Consumers want sustainable choices when it comes to the products they buy. According to research by Nielsen, consumers will choose sustainable products over non-sustainable alternatives three out of four times. On average, brands can expect an uplift of approximately 5% in their shopper base by offering sustainable products.14

Environment - According to the 2017 CDP Carbon Majors report, over half of global industrial emissions can be traced to just 25 corporate and state producing entities. Such companies will only be subject to greater and greater scrutiny and restrictions by stakeholders, including regulators focused on the practices of coal, oil, and gas extraction companies. These are real threats to those businesses.15

The bottom line

More and more, the world is waking up to the impact of poor and unsustainable business practices. Companies that do better in the world also do better by their stakeholders – including their shareholders. The push for a cleaner, more equitable world is changing how business is conducted and what stakeholders expect from companies.

Now more than ever before, companies, stakeholders and investors can all be in this together.

1. United Nations, Transforming our World: the 2030 Agenda for Sustainable Development.

2. CEO Statement (CNW Group/British Columbia Investment Management Corporation (BCI)), November 2020

3. Casey Quirk: It’s not easy being green, 2021 report

4. Morningstar Research Insights, February 2021

5. McKinsey Quarterly: Five ways that ESG creates value, November 2019

6. McKinsey Quarterly: Five ways that ESG creates value - exhibit 1, November 2019

7. McKinsey Quarterly: How much will consumers pay to go green? October 2012

8. Great Place To Work: Treating Employees Well Led to Higher Stock Prices During the Pandemic, August 2021

9. Simon Cole “The Impact of Reputation on Stock Market Value”, February 2013

10. The Conference Board Global Consumer Confidence Survey, conducted in collaboration with Nielsen, Q2 2017

11. Coqual - Being Black in Corporate America, 2019

12. Spencer Stuart, 2019 United States Spencer Stuart Board Index

13. Deloitte - Reputation Risk As A Board Concern, 2015

14. Nielsen: How Can Sustainability Enhance Your Value Proposition? 2018

15. CDP Carbon Majors Report 2017

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. This document may contain forward looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of July 31 2021. There should be no expectation that such information will in all circumstances be updated, supplemented, or revised whether as a result of new information, changing circumstances, future events or otherwise.

The content of this white paper (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

©2021 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Morningstar data is shown as of the most recent reporting period by each fund family. Allocations may not equal 100% and will vary overtime. Assets contained within “Other” category are not classified by Morningstar.

All information presented in this tool is for informational purposes only and is not intended to be investment advice. The information is not meant to be an offer to sell or a recommendation to buy any investment product. Unless otherwise noted, performance is shown before sales charge. For more fund information, click the POS Documents link. All information is historical and not indicative of future results. Current performance may be lower or higher than the quoted past performance, which cannot guarantee results. Share price, principal value, and return will vary, and you may have a gain or a loss when you sell your shares. Performance assumes reinvestment of distributions and does not account for taxes. Performance may not reflect any expense limitation or subsidies currently in effect. Short-term trading fees may apply. To obtain the most recent month-end performance, visit Morningstar.com.

This material is for informational and educational purposes only. It is not a recommendation of any specific investment product, strategy, or decision, and is not intended to suggest taking or refraining from any course of action. It is not intended to address the needs, circumstances, and objectives of any specific investor. Mackenzie Investments, which earns fees when clients select its products and services, is not offering impartial advice in a fiduciary capacity in providing this sales and marketing material. This information is not meant as tax or legal advice. Investors should consult a professional advisor before making investment and financial decisions and for more information on tax rules and other laws, which are complex and subject to change. © 2021 Mackenzie Investments. All rights reserved.