Illiquidity: your hidden superpower

About the author

IN THIS ARTICLE min read

The illiquidity premium

Many investors don’t realize that liquidity comes at a cost. Data shows that investors face a trade-off between the flexibility and convenience of easily tradable liquid investments and the higher historical returns generated by less-liquid private market investments. This excess return from illiquid investments, the illiquidity premium, can be viewed as additional compensation paid to investors in exchange for the inconvenience of limited liquidity. It can also be seen as the opportunity cost of choosing more liquid forms of investment that offer greater flexibility.

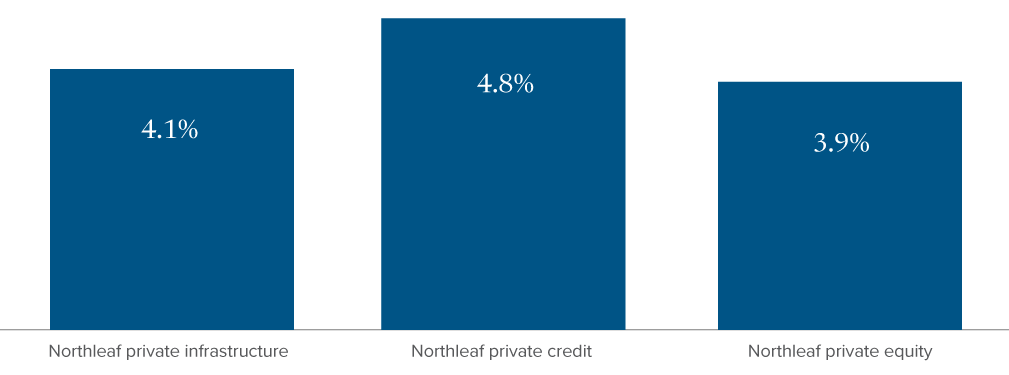

The trade-off remains important even after periods of strong public market performance. While public markets have rallied in the near term, top-tier private managers have continued to outperform public benchmarks over the long term. The chart below illustrates this return difference using private markets strategies managed by Northleaf Capital Partners, Mackenzie’s strategic partner in private market investing and one of Canada’s largest private markets firms. It compares Northleaf’s returns with public market equivalents across the same broad asset classes, assuming a 10-year holding period.

Figure 1: Northleaf vs. public market equivalents: Annualized outperformance by asset class over the past 10 years

As at December 31, 2025. Returns in base currency (USD). Northleaf private infrastructure excess return is the outperformance of Northleaf's infrastructure program versus the S&P Global Infrastructure TR Index. Northleaf private credit excess return reflects outperformance versus 50% ICE BofA US High Yield TR Index + 50% Morningstar LSTA US LL TR Index. Northleaf private equity excess return is the outperformance of Northleaf's private equity program versus the MSCI World GR Index. Past performance is not indicative of future results.

What creates the illiquidity premium?

In our view, the illiquidity premium comes from features of private markets that are difficult to replicate in public markets. Together, these features have historically helped skilled private market managers create significant value for investors over time.

Operational control

Private equity managers usually take majority or control positions in portfolio companies. This allows them to drive improvements in strategy, leadership, operations and capital allocation in ways that minority public-market investors typically cannot.

More room for growth

Private companies range from early-stage businesses to large, mature corporations. By the time a company goes public, much of its (potentially sizeable) early-stage growth may have already been captured by insiders and private investors.

Informational advantages

Private managers can access and analyze detailed company information that is not available or tradeable in public markets before deciding to invest. This can lead to better investment outcomes, particularly for skilled managers with strong sourcing and due diligence capabilities.

Patient, long-term capital

Private asset managers benefit from capital that is committed for longer periods and less likely to be withdrawn during periods of market stress. This gives private companies more room to pursue longer-term strategies without the same pressure to manage to quarterly public market expectations.

Control over exit timing

Public markets reflect current investor sentiment, positive or negative. Private managers can choose the timing of an asset sale and tend to choose times when asset prices are strong. This can help boost the long-term value creation record of private asset managers versus public markets.

Limited intermediaries

Public markets rely on intermediaries that help create liquidity, including investment banks, exchanges and broker-dealer networks. Those services are valuable, but they come at a cost. Private markets can involve fewer layers of intermediation, allowing more of the return potential to accrue to long-term investors.

We view these attributes of private markets to be structural in nature, which may have positive implications for the persistence of the private markets illiquidity premium we describe here.

Manager selection: the critical variable

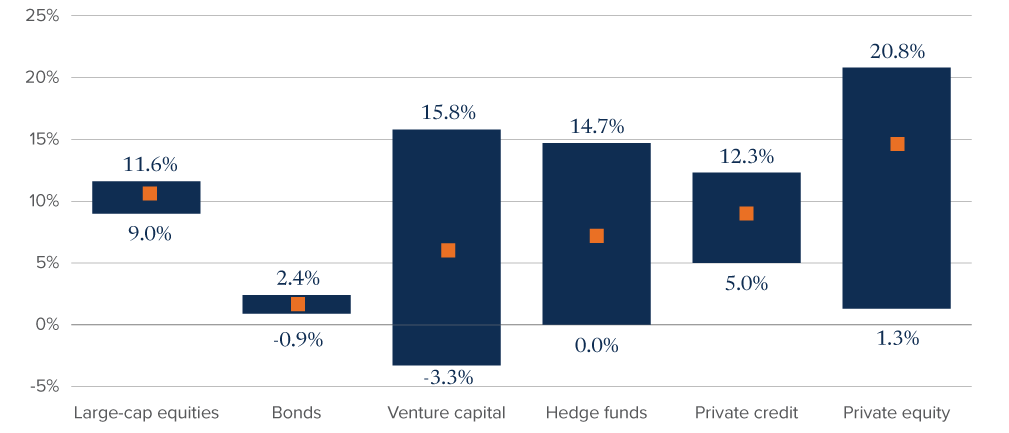

The case for illiquid private-market investments is compelling, but investors must recognize one important truth: the illiquidity premium is not automatic. The dispersion of returns between top-performing and bottom-performing private market managers is dramatically wider than in public markets, meaning choosing a manager matters enormously.

According to J.P. Morgan Asset Management, there has been an average gap of approximately 20 percentage points between top-quartile and bottom-quartile private equity managers over the past 10 years. This is roughly 10 times the dispersion seen in public equity markets. The implication is clear: investing with the wrong manager in private markets can be far more damaging than investing in the wrong public fund — but investing with a proven manager can be a powerful source of risk-adjusted returns.

Figure 2: Public and private manager dispersion

Based on returns from Q4 2015 to Q4 2025

Source: J.P. Morgan Asset Management, Burgiss, NCREIF, Morningstar, PivotalPath. Manager dispersion based on 10-year returns. Global Equities (Large Cap) and Bonds based on Morningstar categories. Private Credit, Private Equity and Venture Capital based on 10-year IRR. Hedge Funds based on PivotalPath index. For illustrative purposes only; data as at December 31, 2025. The dispersion figures shown are approximate representations of industry data.

This data underscores a fundamental point: in public markets, most managers cluster around the index return. In private markets, the gap between a skilled manager and a poor one can span 20 percentage points or more per year — a difference that compounds dramatically over a typical 7–10-year fund life.

Private equity: understanding the premium today

Private equity has historically delivered strong excess returns relative to public markets, with average net outperformance of approximately 300–500 basis points per year over the long term. However, in recent years, as public markets (particularly the S&P 500) experienced exceptional performance driven largely by a narrow group of mega-cap technology stocks, the relative premium of private equity appeared to compress.

This compression was not a sign of private equity weakness. Rather, it reflects an unusual and likely unsustainable concentration in public market returns. When one looks at broader public equity indices — such as the equal-weighted S&P 500 or the Russell 2000 — private equity has continued to compare very favourably.

When public markets soften, private equity shines

Research from KKR's Global Macro & Asset Allocation team provides an important insight: private equity's outperformance over public markets tends to be inversely related to public equity returns. In other words, the lower the S&P 500's return environment, the greater private equity's excess return has historically been.

Figure 3: US private equity excess return vs. S&P 500 return scenarios

Based on KKR analysis “Why private equity? Why now? Reasons to invest in private equity in 2026”. The Cambridge Associates LLC US Private Equity Index is an end-to-end calculation based on data compiled from 1,482 US private equity funds (buyout, growth equity, private equity energy and mezzanine funds), including fully liquidated partnerships. Pooled end-to-end return, net of fees, expenses and carried interest. Historic quarterly returns are updated in year year-end report to adjust for changes in the index sample. Data latest available as at June 30, 2025. Source: Cambridge Associates, S&P. Observed period: Q1 1986 – Q1 2025.

There is clear economic rationale for this relationship. When public markets are surging, investors accept lower equity risk premiums. When public market returns are modest or challenged — as KKR and many leading strategists now project for the next five years — private equity's active value creation model, control positions and diversified opportunity set become far more advantageous.

The forward-looking case: private markets well-positioned

Perhaps the most important question for investors today is not what private markets have delivered historically, but what they can deliver in the years ahead. On this front, the evidence is compelling.

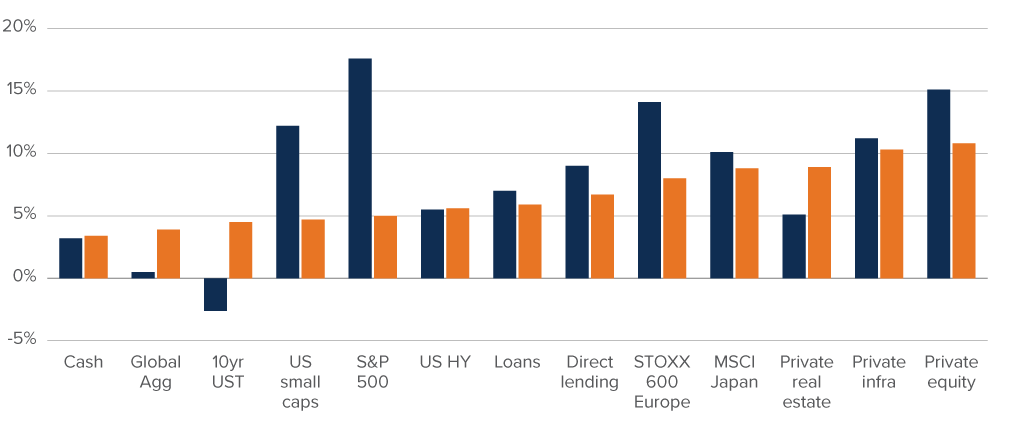

For example, KKR’s 2025 Capital Market Assumptions project that private equity will deliver approximately 11–12% net annual returns over the next five years, compared to just 5–6% for the S&P 500. Similarly, private credit (direct lending) is expected to generate 7–9% annually, well above global bonds at 4–5%. Private infrastructure, benefiting from contractual inflation linkage and sustained demand, is projected to deliver 8–10%.

Figure 4: Past five-year returns vs. next five-year forecasts by asset class

Currency in USD. Based on KKR analysis “Why private equity? Why now? Reasons to invest in private equity in 2026”. For private asset classes, returns represent median manager return net of fees and carry. Past 5-Years return from October 31, 2020 to October 31, 2025 for consistency across asset classes. Private Markets as at Q2 2025. Source: Bloomberg, BofA, Burgiss, Cambridge, KKR Global Macro & Asset Allocation analysis. Forecasts are forward-looking projections and are not guaranteed.

The shift in the relative return outlook is significant. In the past five years, the S&P 500 outperformed private equity — an unusual outcome driven by the extraordinary concentration and multiple expansion of mega-cap technology stocks. Looking forward, as public equity valuations remain elevated and earnings growth expectations moderate, private equity and private markets broadly are expected to reclaim a meaningful advantage.

Is it worth paying for a service you’re not using?

In summary, liquidity is a service provided by public market intermediaries, which comes at a cost. There are numerous advantages to operating a company and/or managing a fund in the private capital markets that are not available to public market investors, and those advantages have historically tended to produce superior returns for investors over time. Liquid investment funds also do not provide exposures to the large universe of private companies that can offer compelling growth and value-creation potential.

Retail investors often hold more liquidity than their long-term plans require. The data shows that mutual fund investors are not typically active traders within their accounts, suggesting that full liquidity is valued more than it is used. In practice, not every dollar of investible assets needs to always be available.

For capital that can remain invested, trading a portion of that liquidity for access to private assets may have historically improved return potential. That premium is supported by enduring features of private markets that are likely to remain relevant over time.

Liquidity is valuable when it serves a clear purpose. When it is held in excess, however, it can become an opportunity cost. For investors with capital that can remain invested over longer horizons, private markets may offer a way to turn unused flexibility into access to return drivers that are not generally available in public markets.

To find out more about the advantages of investing in private, illiquid investments, speak to your financial advisor.

For accredited investors only (as defined in NI 45-106). Past performance is not necessarily indicative of any future results.

The content of this material (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This material is not intended to constitute an offer of units of Mackenzie Northleaf Global Private Equity Fund, Mackenzie Northleaf Private Credit Fund, Mackenzie Northleaf Private Infrastructure Fund, or Mackenzie Northleaf Multi-Asset Private Markets Fund (the “Funds”). The information herein is qualified in its entirety by reference to the applicable Offering Memorandums of the Funds. The OMs contain information about the investment objectives and terms and conditions of an investment in the Funds (including fees) and also contains tax information and risk disclosures that are important to any investment decision regarding such Funds.