Refined over 30 years, the Mackenzie Ivy Team’s approach to investing is time-tested and trusted, protecting capital and helping investors reach their long-term goals. In this interview with the Ivy Team, we drill deeper into how Ivy helps investors meet their objectives.

Q1. Tell us about the Ivy investment approach.

Matt: The Ivy approach is rooted in discipline and patience. We aim to better understand how businesses perform under a variety of market conditions, especially in adverse environments. By focusing on quality businesses and being highly selective about how we invest, we build concentrated portfolios designed to outperform when markets are under pressure while still participating in the upside.

We aim to deliver above-average returns over a full market cycle, with less volatility than our peers along the way.

Q2. Long-term investing is a term everyone uses. But for Ivy, long-term has a very specific meaning. Can you explain what that means for you?

Matt: At Ivy, we have been through a lot together and know from experience that anything can happen, and over time it likely will. So, we use a full cycle — about 10 years — to determine a company’s ability to deliver the kind of steady earnings required to generate consistent returns. We don’t sugarcoat it: our forecasts bake in at least one recession, and if a company’s valuation only looks good on blue-sky assumptions, it doesn’t work for us, even if it looks great in the present moment.

Adam: We are looking for quality companies with management teams that are aligned with our long-term investment horizon, rather than prioritizing short-term objectives. There are companies that will sell off solid businesses or conduct share buybacks at the expense of long-term durability. We make sure to filter that out in our research.

Q3. What kinds of companies do you find typically perform well over a full market cycle?

Matt: We look for successful, world-class businesses that know their edge and consistently invest in it. These qualities are the hallmarks of enduring value. Companies like that come in many different shapes and sizes — Google and TJX look nothing alike, yet both own proven, durable advantages around data moats and lowest cost scale.

Hussein: We are very vigilant on the thesis for a company and monitor the numbers continually. Industry structures change and competitive advantages erode. We ask “Is it a high-quality business? Does it have a solid balance sheet to help it survive and outcompete during market shocks?” We especially interrogate whether that quality is sustainable.

Q4. Ivy is often perceived as being very cautious and methodical, but that’s not always the case. When are the times Ivy might be considered nimble and opportunistic?

Matt: The relentless rigour we place around understanding companies provides a strong investment edge that can be very quickly leveraged when a desired company hits the right price point. There is no need to scramble to research that company on the fly — that work is always done well ahead of time, allowing the team to strike with confidence.

Jason: That quality also makes us a little unconventional in volatile markets. When managers who use different approaches need to pause — or even backpedal — and reconsider, we’re ready to act on opportunities when they arise. In that sense, our approach makes us nimble.

Q5. So, there is some offense built into your defensive approach?

Matt: Absolutely. We are active managers, and taking a defensive approach does not need to mean sitting on your hands. We act to provide both downside protection and upside capture. We believe that this allows our funds to compound much better than purely defensive vehicles.

Marlena: That ties into how we invest through a market cycle. In fact, some of our most active trading is in periods of market upheaval. Our long-term view allows for opportunistic purchases, and whether they may be defensive or cyclical businesses, we take a portfolio approach and remain diversified.

Q6. What does Ivy’s “unconventional” approach mean for the experience of investors in your funds?

Hussein: It’s a mindset that goes slightly against the grain, and it can lead to unconventional performance in the short term, but ultimately to better outcomes for investors.

James: We try to view everything through the lens of the investor — how they experience risk and behave in different markets. This shapes how we define success: “winning” can sometimes mean lagging slightly in strong up markets if it means offering greater resilience in down markets and a smoother journey overall. That helps investors avoid common behavioural pitfalls, like selling in the downturns.

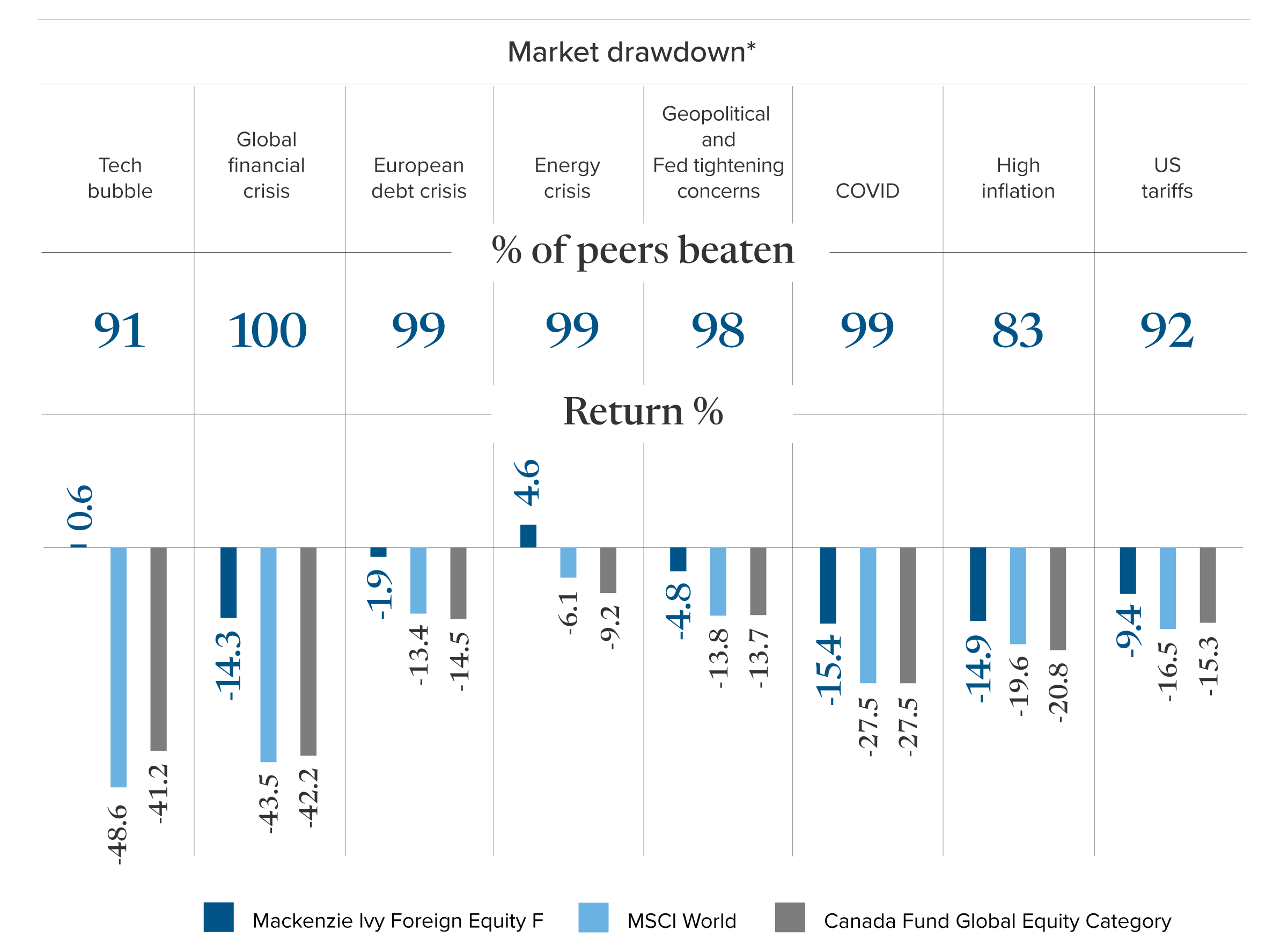

Mackenzie Ivy Foreign Equity Fund – Top quartile in every drawdown

The MSCI World returns in this chart are displayed in Canadian dollars to ensure comparability with the Mackenzie Ivy Foreign Equity Fund and other Canadian-domiciled global equity peers. Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in the investment products that seek to track an index.

When the market goes down — which it inevitably will at some point — we’re able to use our knowledge and process to confidently buy into drawdowns and upgrade the quality of the portfolio. That can put investors in an even better position going forward. Ultimately, our goal is to make investors better off in the long run.

Q7. Last word: Sum up Ivy’s edge in a sentence.

Matt: Two sentences! Always careful. Permanently opportunistic. That balance, executed by a team that’s lived every cycle since the tech bust, is hard to clone with algorithms or quarterly playbooks.

Long-term performance

| 1Y | 3Y | 5Y | 10Y |

Mackenzie Ivy Foreign Equity Fund – Series F | -0.02% | 10.19% | 7.35% | 6.96% |

Source: Morningstar. As at March 31, 2026.

* Tech bubble - 04/27/2000 – 03/12/2003, global financial crisis - 10/14/2007 – 03/09/2009, European debt crisis - 05/02/2011 – 10/04/2011, energy crisis – 05/21/2015 – 02/11/2016, geopolitical and fed tightening concerns – 09/23/2018 – 12/25/2018, COVID – 02/19/2020 – 03/23/2020, high inflation 01/04/2022 – 09/30/2022, US tariffs 02/18/2025 – 04/08/2025.”

Percentile rankings are from Morningstar Research Inc., an independent research firm, based on the Global Equity, and reflect the performance of the Mackenzie Ivy Foreign Equity Fund for the 1-, 3-, 5- and 10-year periods as of September 30, 2025. The percentile rankings compare how a fund has performed relative to other funds in a particular category and are subject to change monthly. The number of Global Equity funds for Mackenzie Ivy Foreign Equity Fund Series F for each period are as follows: one year – 1785; three years – 1578; five years – 1290; ten years – 694.

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns as of March 31, 2026, including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution, or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document may contain forward-looking information which reflect our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of March 31, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

©2025 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.