Bullish until the bill comes due?

About the author

IN THIS ARTICLE

Select Section

Key points

- US federal debt has grown to levels that many investors believe may prove unsustainable over the long term.

- No one can predict when financial markets may begin to challenge America's fiscal trajectory, but the consequences of such a shift in confidence would likely reverberate across bonds, equities, currencies and the global economy.

- Until that inflection point arrives, the prudent investment strategy may simply be to remain bullish until the bill comes due.

The growing fiscal challenge facing the United States

The US has long benefited from extraordinary economic and financial advantages. It is the world's largest economy, issues the dominant global reserve currency and enjoys the deepest, most liquid securities markets ever created. These strengths have allowed successive administrations to finance deficits at relatively low cost, while investors around the world have willingly accumulated US Treasury securities as the benchmark risk-free asset.

Yet these advantages should not be mistaken for immunity. Over the past quarter-century, the trajectory of US federal finances has changed dramatically. Debt has risen at a pace well above economic growth, structural deficits have become embedded in the federal budget and interest costs are consuming an ever-larger share of national income.

While the US is still far from an imminent fiscal crisis, the long-term direction of travel deserves careful attention. The question facing investors is not whether higher debt matters today, but whether there is a point at which markets start to question the sustainability of America's fiscal position.

The consequences of such a reassessment would extend well beyond Washington. Changes in investor confidence could influence interest rates, inflation expectations, equity valuations, credit markets, currency markets and global capital flows. The timing of such an inflection point is unknowable, but the possibility warrants consideration because financial markets often ignore long-term risks until they suddenly become immediate.

The explosion in federal debt

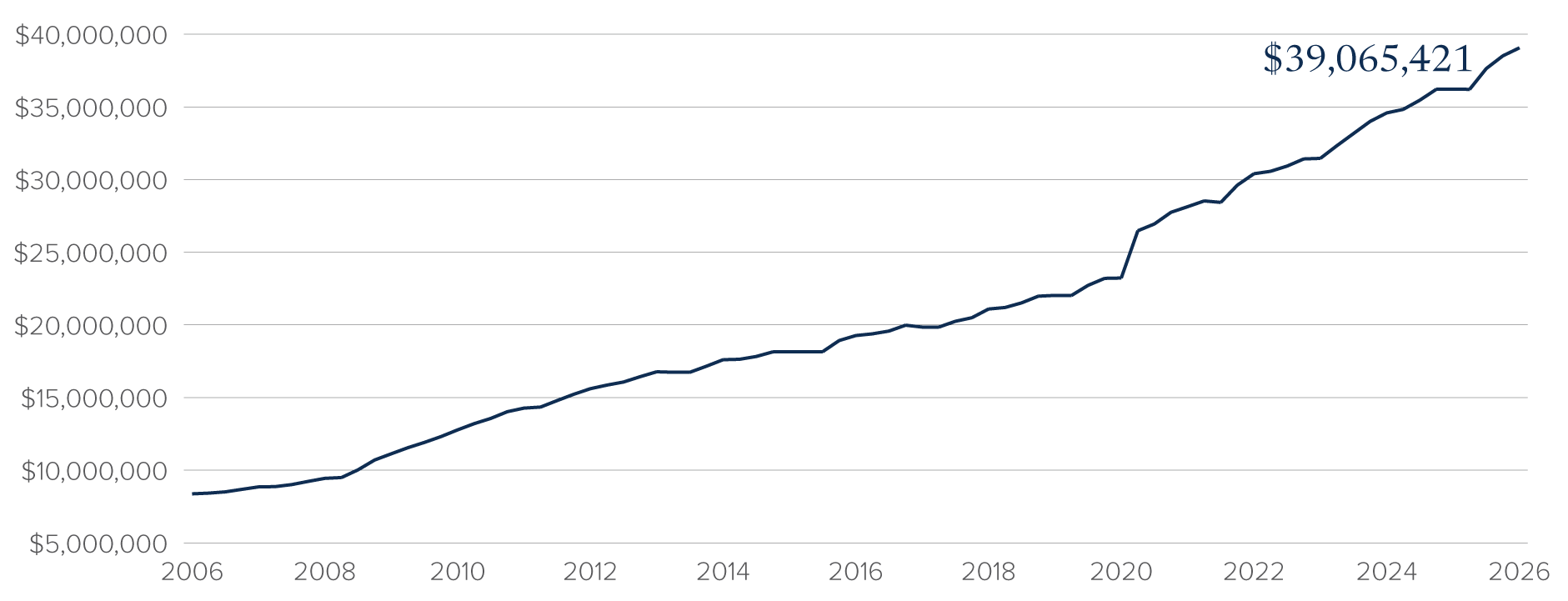

The rise in US federal indebtedness over the past 25 years has been extraordinary. At the beginning of the century, total federal debt stood at approximately $5.7 trillion. Today it exceeds $39 trillion, representing a more than six-fold increase. This expansion reflects the cumulative effects of multiple recessions, tax reductions, military spending, demographic pressures, entitlement growth, pandemic-related fiscal stimulus and persistent structural deficits (run by both Democratic and Republican administrations). Figure 1 exhibits the updated US federal debt levels.

Figure 1 - US Federal Debt (in trillions of US dollars) over the past 20 years.

Source: U.S. Department of the Treasury, FRED

This increase cannot be explained solely by temporary crises. Historically, debt surged during major wars or severe recessions before stabilizing as economic growth resumed and governments restored fiscal discipline. More recently, however, debt accumulation has become a structural feature of the federal budget. Even amid low unemployment, robust corporate profits and sustained economic growth, annual deficits have remained historically large.

Viewed in isolation, the absolute dollar amount of debt can be misleading because economies typically become larger over time. Nevertheless, the sheer scale of federal borrowing provides important context. Every additional dollar borrowed ultimately requires either future taxation, reduced government spending, faster economic growth or additional borrowing. The larger the stock of debt becomes, the more sensitive government finances become to changes in interest rates.

Who holds the debt?

It is also important to recognize that not all US federal debt is held by private investors or foreign governments. A significant portion is held by the Federal Reserve due to its monetary policy operations, while another substantial share is held by government trust funds and other federal accounts, such as the Social Security and Medicare trust funds. These intra-governmental holdings represent obligations that one part of the federal government owes to another, rather than to external creditors.

Although these holdings reduce the amount of debt that must be financed in public markets, they do not eliminate the government's obligations. Interest payments on Federal Reserve holdings are largely returned to the Treasury after the Fed's operating expenses. But the principal must still be refinanced or repaid when securities mature. Similarly, securities held by government trust funds will need to be redeemed as benefits are paid, requiring the Treasury to obtain cash through taxes, spending reductions or borrowing from the public.

Consequently, while distinguishing between debt held by the public and debt held within the government is important, the existence of these internal holdings does not fundamentally alter the long-term fiscal challenges posed by persistently rising federal debt.

Debt relative to the economy

For this reason, economists generally focus on debt relative to gross domestic product (GDP) rather than absolute debt levels. Debt-to-GDP measures the economy's capacity to support outstanding obligations and allows meaningful comparisons across time.

Following the Second World War, US federal debt briefly exceeded 100% of GDP before declining steadily for decades, as rapid economic growth outpaced new borrowing. Today's fiscal picture is fundamentally different. Rather than falling during periods of expansion, debt has continued to trend upward and now stands at levels comparable to, or exceeding, the post-war peak.

Unlike the post-war era, however, current demographics present additional challenges. An aging population is increasing expenditures on Social Security and Medicare, while slowing labour force growth reduces the economy's long-term growth potential. At the same time, political polarization has made meaningful fiscal reform increasingly difficult. The result is a debt trajectory that, under current policy assumptions, continues to rise for decades.

High debt ratios do not necessarily trigger an immediate fiscal crisis. Japan, for example, has maintained debt levels well above those of the US for many years. However, America relies much more heavily on foreign investors and international capital markets. Confidence therefore becomes an important variable. Financing costs can change quickly, once markets begin questioning whether fiscal policy remains sustainable.

Rising debt servicing costs

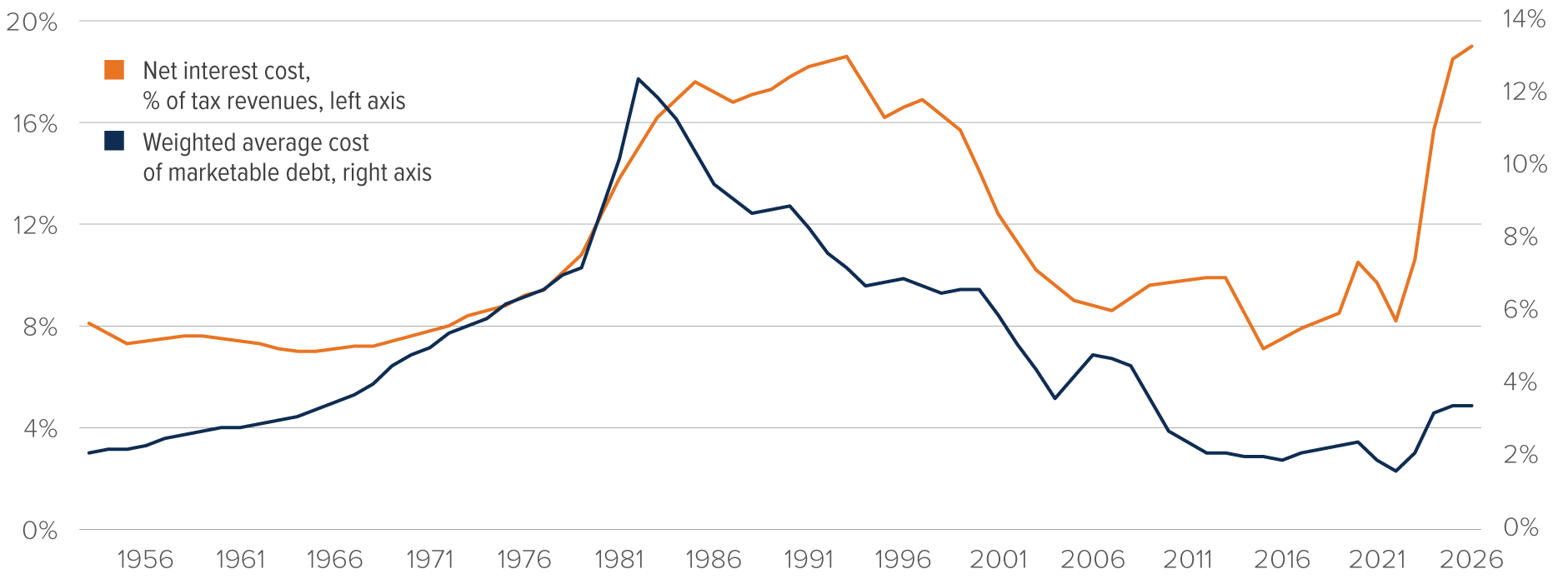

The true economic burden of government debt is not its headline size, but the cost of servicing it. Governments do not repay their obligations all at once. Instead, they continually refinance maturing debt while making interest payments from current revenues. Consequently, interest expense as a percentage of GDP provides the clearest measure of fiscal pressure. Figure 2 illustrates net interest costs as a percentage of tax revenues.

Figure 2 - Net Interest Cost & Weighted Average Cost of Marketable Debt

Source: Mackenzie Investments, Strategas Research Partners.

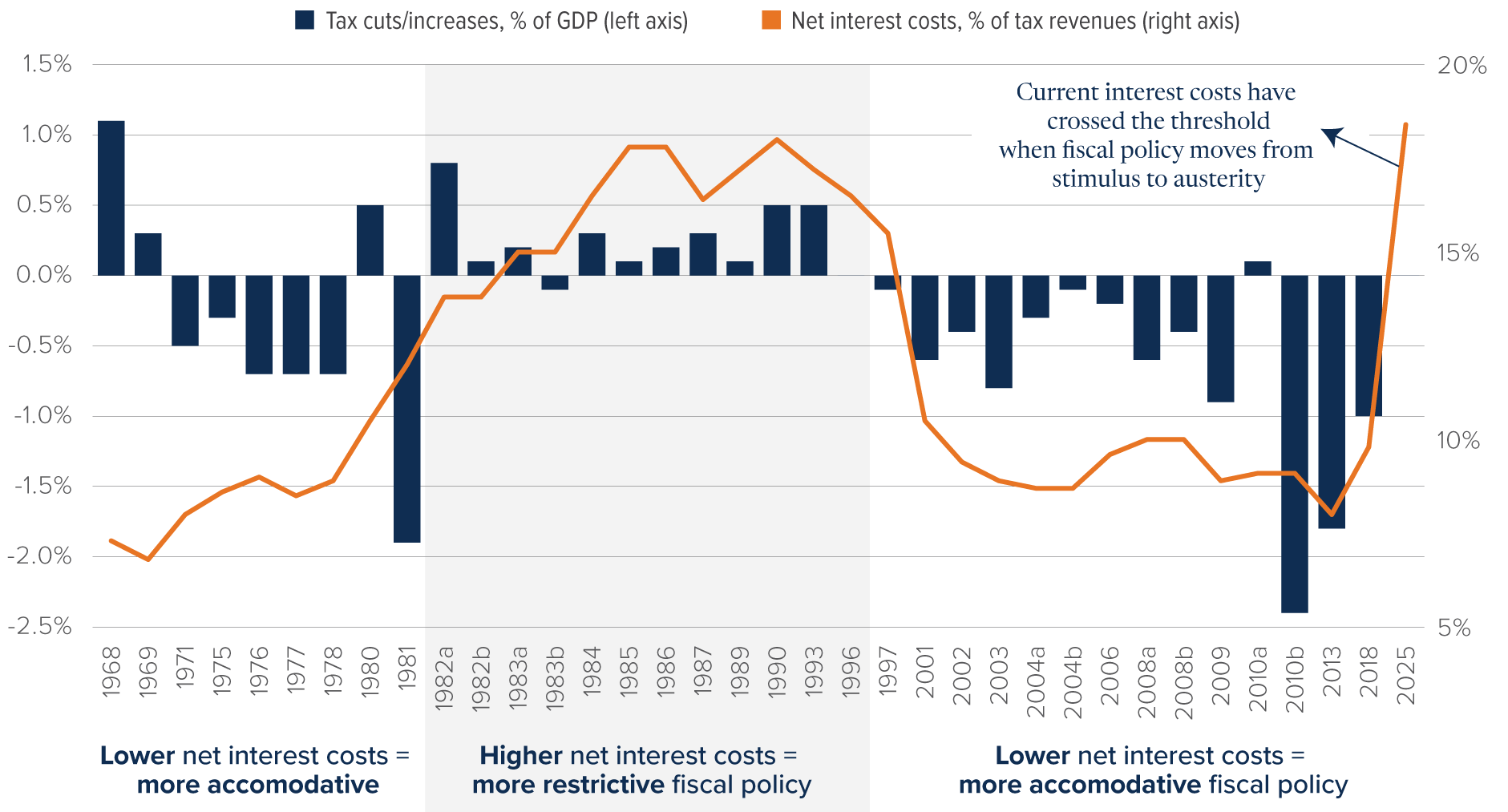

For much of the decade following the Global Financial Crisis, historically low interest rates masked the growing debt burden. Although federal borrowing expanded rapidly, financing costs remained manageable because Treasury yields hovered near historic lows. This unusual environment encouraged the perception that debt could continue increasing indefinitely without meaningful consequences. Figure 3 illustrates tax cuts/increases and net interest costs as a percentage of revenues.

Figure 3 - US debt sevicing costs determines the us fiscal environment;

new post-WWII high in May

Tax Cuts/Increases, % of GDP

Source: Mackenzie Investments, Strategas Research Partners.

That perception has changed. As inflation returned and the Federal Reserve raised policy rates, the cost of financing federal debt rose sharply. With a much larger stock of outstanding debt, even modest increases in average borrowing costs translate into substantial increases in annual interest expense.

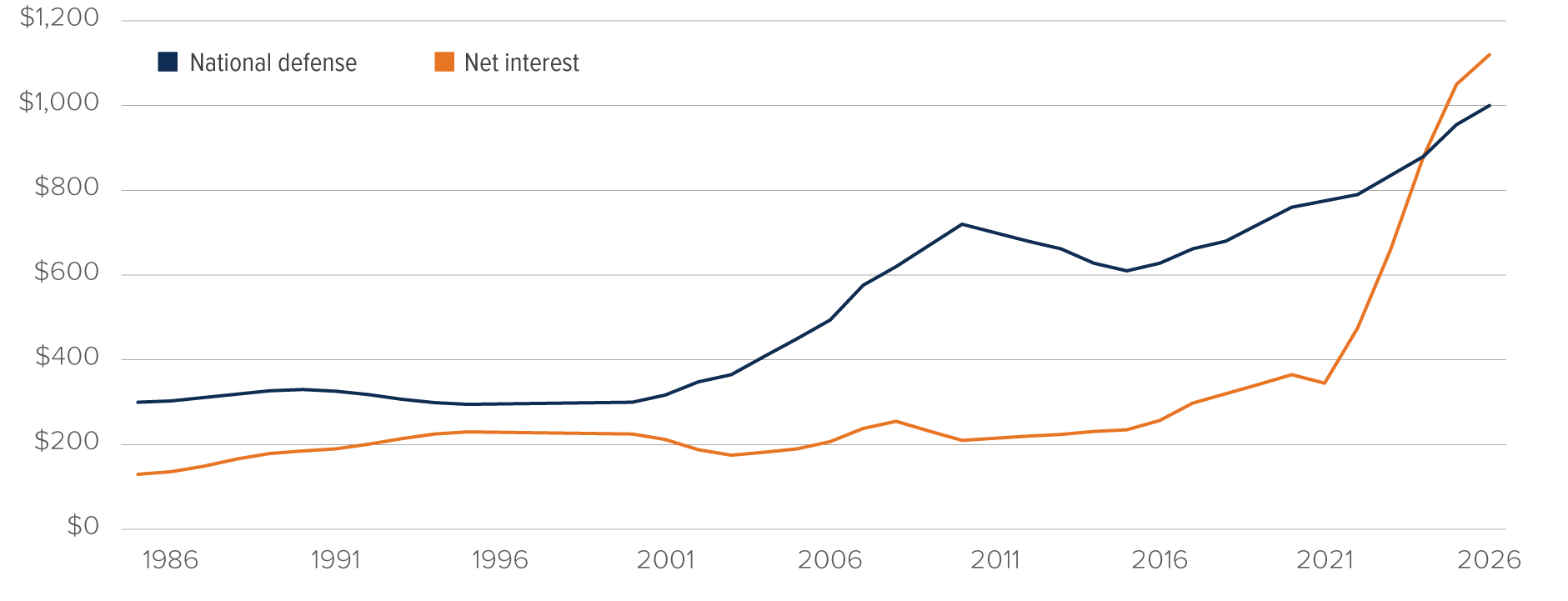

Interest payments are now among the fastest-growing components of the federal budget. Unlike infrastructure, education or defence spending, interest payments produce no new public services or productive assets. They simply represent the cost of past borrowing. Every dollar devoted to servicing debt is a dollar unavailable for future policy priorities or tax relief. Figure 4 illustrates net interest costs compared against defense spending.

Figure 4 - Defense & Net Interest Spending (12 Mo. Rolling, $BN)

Source: Mackenzie Investments, Strategas Research Partners.

A departure from classical Keynesian policy

The current fiscal trajectory also represents a notable departure from traditional Keynesian economic principles. Classical Keynesian theory advocates running deficits during recessions to support aggregate demand, while returning to balanced budgets, or even surpluses, during periods of economic expansion. Fiscal policy is intended to be countercyclical, providing stimulus when needed and rebuilding fiscal capacity during prosperous periods.

Recent US fiscal policy has increasingly broken from this framework. Large deficits have persisted not only during recessions but also throughout periods of exceptionally strong labour markets and robust economic growth. Rather than rebuilding fiscal flexibility during good times, the federal government has continued adding debt almost irrespective of the economic cycle.

This shift has important implications. Persistent structural deficits leave policymakers with less room to respond when the next recession inevitably arrives. Future stimulus packages may become more expensive precisely because debt levels and interest costs have already reached elevated levels.

What happens if the bill comes due?

Financial markets rarely respond to long-term risks in a gradual fashion. Instead, they often exhibit long periods of complacency punctuated by sudden changes in sentiment. Fiscal sustainability may prove no different.

If investors demand higher compensation for holding Treasury securities, yields could rise independently of Federal Reserve policy. Higher Treasury yields would increase borrowing costs throughout the economy, affecting mortgages, corporate debt, commercial real estate and consumer lending. Higher discount rates would also place downward pressure on equity valuations, particularly for long-duration growth companies which have valuations that depend heavily on future earnings.

Persistent deficits could also complicate monetary policy. If markets begin expecting debt monetization or sustained fiscal dominance, inflation expectations could become less well-anchored. Even if inflation remained contained, increased Treasury issuance could crowd out private investment by absorbing a larger share of available savings.

The US dollar presents another important consideration. The dollar's reserve currency status provides significant protection by generating persistent global demand for Treasury securities. However, reserve currency status is an advantage earned through confidence rather than an immutable law of finance. A gradual erosion of confidence would likely occur over many years rather than overnight. Yet even modest diversification by global reserve managers could increase borrowing costs at the margin.

None of these outcomes are inevitable. America's innovative economy, flexible labour markets, deep capital markets and reserve currency status remain powerful structural strengths. Sensible fiscal reforms, stronger productivity growth and sustained economic expansion could materially improve long-term debt dynamics. History demonstrates that countries can stabilize debt burdens through a combination of growth, inflation, fiscal restraint and structural reform.

Investment implications

For investors, the most important lesson is that long-term fiscal concerns do not necessarily imply an immediate bearish outlook. Markets often perform well during periods of rising public debt, particularly when corporate earnings remain strong and economic growth continues. Indeed, the US equity market has generated exceptional returns throughout much of the period during which federal indebtedness has accelerated.

The greater risk lies further down the road. As debt servicing costs consume a larger share of economic output and government revenues, the probability that markets eventually demand greater fiscal discipline increases. Whether that adjustment occurs gradually or abruptly is impossible to predict. However, history suggests that once confidence begins to erode, policy options narrow quickly.

The appropriate conclusion is therefore neither complacency nor alarmism. Investors should recognize that the US retains enormous economic strengths, while also acknowledging that current fiscal trends are unlikely to continue indefinitely. Bull markets often persist longer than fundamentals alone might suggest, and few catalysts are more difficult to time than a sovereign debt reassessment. Nevertheless, the arithmetic of debt ultimately cannot be ignored. The US may continue to benefit from its exceptional position in the global financial system for many years, but eventually, every borrower faces the same reality: the bill comes due.

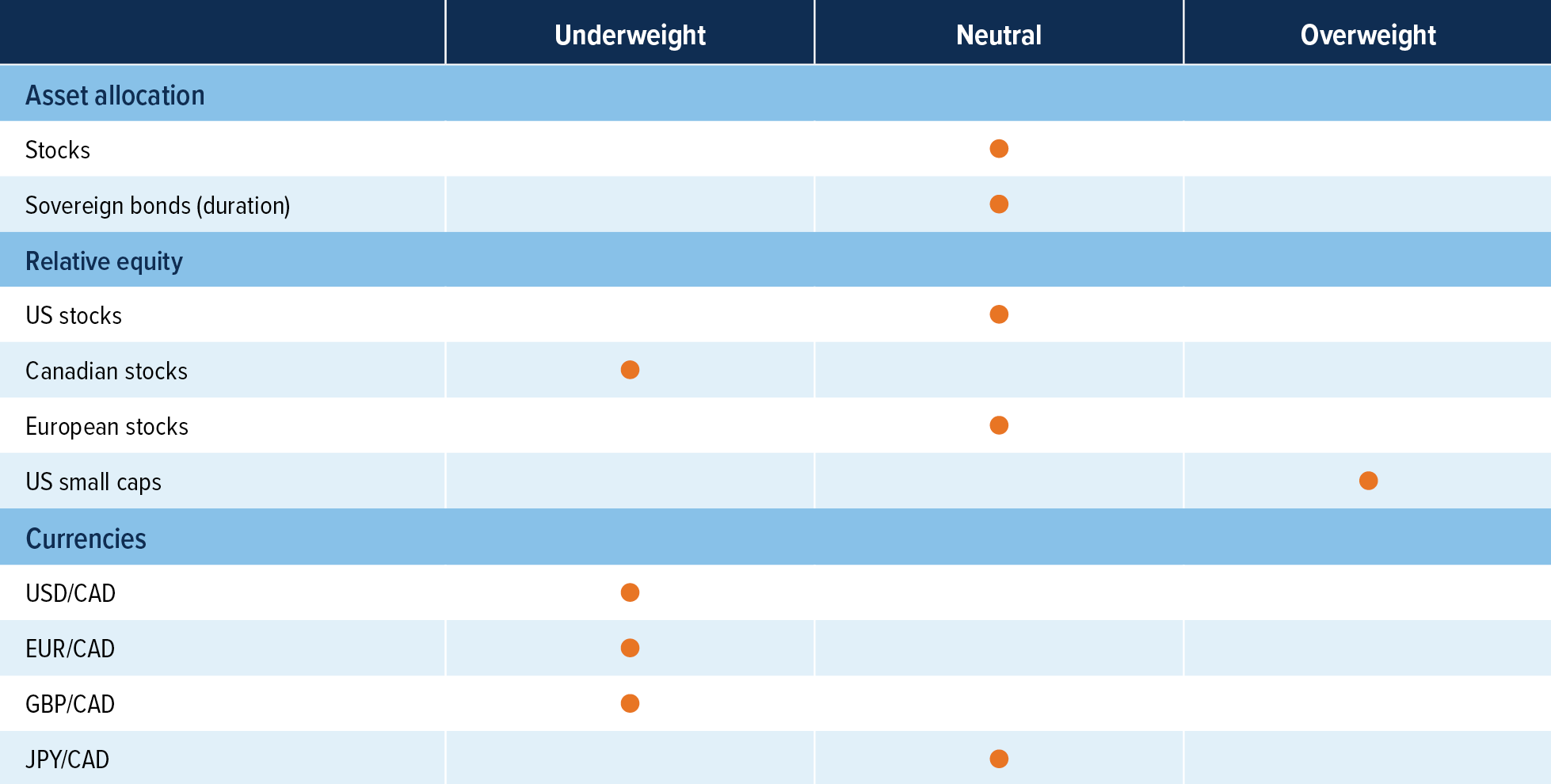

Multi-Asset Strategies Team’s investment views

Tactical summary

Source: Mackenzie Investments.

Note: The opinions expressed in this piece reflect short-term tactical views, which inform the positioning of some of the funds managed by the Multi-Asset Strategies Team.

Positioning highlights

Remain neutral on equities: Markets were sluggish in June as they struggled to find a direction. The prospect of higher rates from the new Federal Reserve Chair, Kevin Warsh, and weakness in the AI trade offset strength in other sectors. Our view is that the fundamental backdrop for equities (earnings and the economy) is strong, but we see stretched positioning from retail investors, which has sometimes led to sharp selloffs.

Remain neutral on bonds: We remain neutral on bonds. Warsh came out with a very aggressive statement in fighting inflation. This had an uncommon effect where bond yields on long-term bonds (20 year+) went down as the market priced in lower inflation in the long-term, but two-year bond yields skyrocketed as more rate hikes were priced in. The curve flattening combined with stronger US economic data leads us to remain neutral.

Close Europe underweight for Canada underweight vs. US small cap: Canada's economic data has weakened since last month, while economic conditions in Europe have improved. As a result, we shift to an underweight Canada versus US small cap instead of Europe versus US small cap. US small caps remain attractive, as a stronger US economy is supportive of small caps, which have remained undervalued for an extended period of time.

Currencies: No change in currency views from last month. The USD remains overvalued and our long-term view is for the USD to depreciate versus most developed countries. We continue to like CAD and JPY as the best plays for this view. CAD's recent sell-off has not been justified by the underlying economic conditions, so we remain bullish.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated. The content of this material (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it. This material contains forward-looking information which reflects our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of June 30, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise. Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in the investment products that seek to track an index.