What to expect from new Federal Reserve Chair Kevin Warsh

About the author

IN THIS ARTICLE

Select Section

Highlights

- Incoming Fed Chair, Kevin Warsh, combines crisis-management experience, market expertise and policy credibility during heightened economic uncertainty.

- The Fed Chair strongly influences interest rates, liquidity conditions, valuations and institutional portfolio performance.

- Persistent inflation, elevated deficits, geopolitical uncertainty and fragile markets create unusually difficult policy challenges.

Introduction

On May 13, 2026, the US Senate confirmed Kevin Warsh as the new Chair of the Federal Reserve, replacing Jerome Powell. In this role, Warsh will play an important part in guiding US monetary policy, helping to manage inflation and employment objectives, and shaping financial market expectations during a period of economic uncertainty.

So, who is Kevin Warsh?

Kevin Warsh has an impressive background. Kevin Warsh is an American financier, lawyer and policymaker whose academic background combines public policy, economics and law. He earned a bachelor’s degree in public policy from Stanford University in 1992, where he concentrated on economics and political science, before receiving a Juris Doctor from Harvard Law School in 1995. He also completed additional coursework in market economics and debt capital markets at Harvard and MIT. After law school, Warsh joined Morgan Stanley, where he worked in mergers and acquisitions and rose to become vice president and executive director in the investment banking division.

Warsh transitioned from Wall Street to public service in 2002, serving in the George W. Bush White House as Special Assistant to the President for Economic Policy and Executive Secretary of the National Economic Council. In 2006, President Bush appointed him to the Federal Reserve Board of Governors, making him one of the youngest governors in the institution’s history. During the 2008 global financial crisis, Warsh played a prominent role in the Fed’s engagement with financial markets and worked closely with then-Chair Ben Bernanke and Treasury officials on crisis-response measures involving institutions such as Bear Stearns, Lehman Brothers and AIG. After leaving the Fed in 2011, he remained active in policy, academic and financial circles through roles at Stanford’s Hoover Institution, Stanford Graduate School of Business, Stanley Druckenmiller’s Duquesne Family Office and several corporate boards.

That breadth of experience is a key reason Warsh is widely seen as well qualified for the role. His career spans crisis-management experience at the Federal Reserve, as well as deep knowledge of financial markets, public policy and global economics. His role during the 2008 financial crisis lends credibility in periods of market stress and inflation uncertainty, while his private-sector and academic work have kept him closely connected to evolving macroeconomic and capital-market dynamics. Supporters also view him as a strong institutional leader capable of balancing central bank independence with pragmatic policymaking at a time when the Fed is under heightened scrutiny over inflation, interest rates and economic growth.

At the same time, Warsh’s personal background has drawn attention. He is married to Jane Lauder, daughter of billionaire businessman Ronald Lauder, placing Warsh among the wealthiest individuals ever considered for the Fed Chair role. Supporters argue that his financial independence and market experience may strengthen his credibility with investors and policymakers. Critics however contend that his ties to elite financial and corporate circles may raise questions about his sensitivity to the economic pressures facing average households and workers.

What is Warsh facing?

First, let’s look at the Fed’s dual mandate, in the words of that institution:

“Our two goals of price stability and maximum sustainable employment are known collectively as the ‘dual mandate.’ The Federal Reserve's Federal Open Market Committee (FOMC). which sets U.S. monetary policy, has translated these broad concepts into specific longer-run goals and strategies.

Price stability

The Committee judges that inflation at the rate of 2 percent, as measured by the annual change in the Price Index for Personal Consumption Expenditures (PCE), is most consistent over the longer run with the Federal Reserve's statutory mandate. The Committee has also explicitly noted that the inflation target is symmetric and stated that it ‘would be concerned if inflation were running persistently above or below this objective.’

Maximum sustainable employment

Many nonmonetary factors affect the structure and dynamics of the labor market, and these may change over time and may not be measurable directly. Accordingly, specifying an explicit goal for employment is not appropriate. Instead, the Committee’s decisions must be informed by a wide range of labor market indicators.”

So where are we on each side of the Fed’s dual mandate?

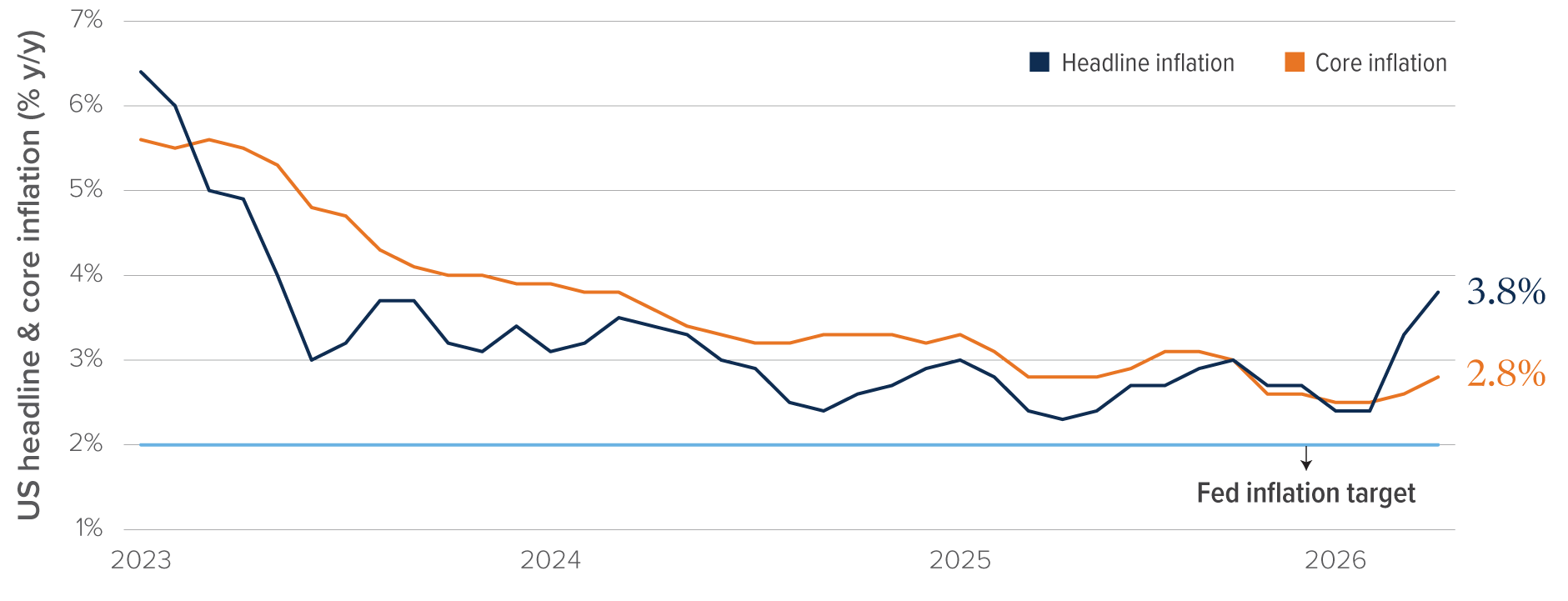

Let’s start with a review of relevant recent inflation statistics. Figure 1 illustrates updated headline and core inflation data.

Figure 1 – US headline & core inflation

Source: Bloomberg. As of April 30, 2026.

It is evident from the US inflation data above that price pressures remain elevated and above the Federal Reserve’s 2% target. The Consumer Price Index (CPI) rose 3.8% year-over-year in April, up from 3.3% in March, with higher energy costs, particularly gasoline, accounting for a significant portion of the increase. Core inflation, which excludes food and energy, rose 2.8% over the past year, while shelter costs continued to contribute to underlying price pressures.

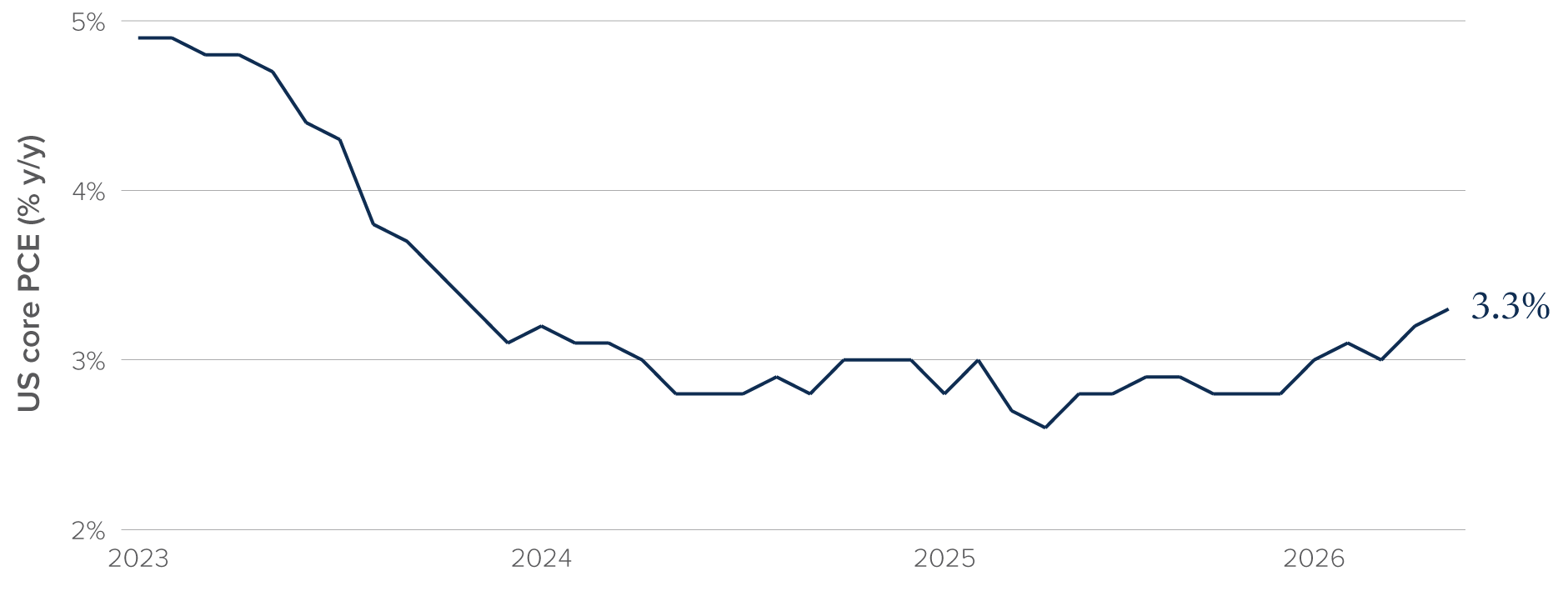

As well, it is useful to review the Fed’s preferred inflation measure, the Core PCE Deflator, to get a fulsome view of inflation trends (Figure 2).

Figure 2 – US core PCE

Source: Bloomberg. As of April 30, 2026.

The Fed’s preferred inflation measure, the Personal Consumption Expenditures (PCE) index, also increased 3.8% year-over-year in April, with core PCE rising 3.3%. Overall, the data indicates that inflation has reaccelerated in recent months, complicating the outlook for interest rate cuts and reinforcing expectations that policymakers will remain cautious.

What each of the above indicators shows is that inflation remains elevated, well above the Fed’s 2.0% target. There had already been a stubborn persistence in underlying inflation pressures throughout 2025, which many have attributed in part to the impact of President Trump’s tariff policies on goods inflation. More recently, inflation has received an additional upward push from elevated energy prices tied directly to the President’s war against Iran. The disruption to global energy supply chains, both through the destruction of production capacity and the temporary closure of the critical Strait of Hormuz shipping corridor, has intensified upward pressure on energy and transportation costs, creating renewed inflationary risks across the broader economy.

The key takeaway is that inflationary pressures are proving more persistent and broad-based than policymakers had anticipated, reducing the likelihood of a near-term return to the Fed’s 2.0% target. Trade policies and geopolitical conflict are now reinforcing one another, with tariffs sustaining core inflation while energy supply disruptions add a new layer of upward price pressure across the global economy.

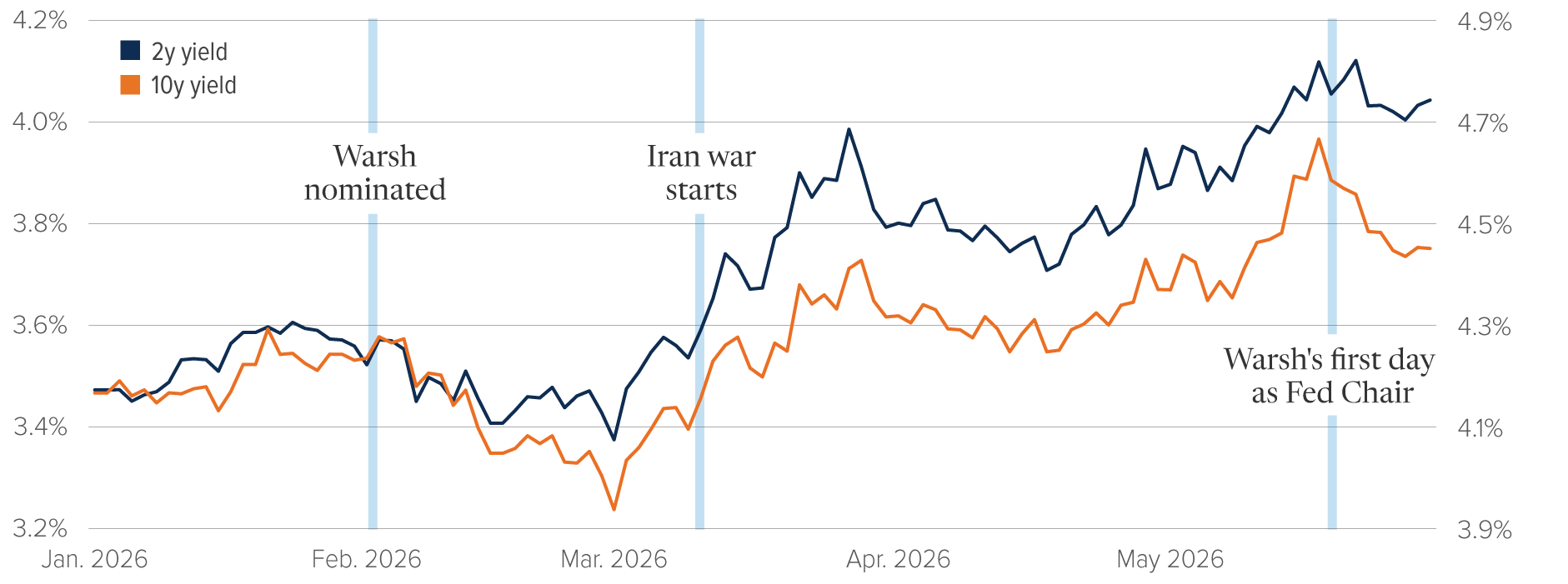

The expected effect of much higher energy prices (due to war in Iran), and the potential for this to feed through to higher inflation in the near-term, has resulted in a sharp rise in bond yields, as seen in Figure 3.

Figure 3 – Rising short-term Treasury yields

The surge in yields since the start of the Iran war has jeopardized Warsh's stated policy agenda.

US 2-year and 10-year treasury yields (%).

Source: Bloomberg, Mackenzie Investments, as of May 26, 2026.

Higher bond yields, should they persist, have the potential to act as a drag on economic growth and thus make Warsh’s life more difficult.

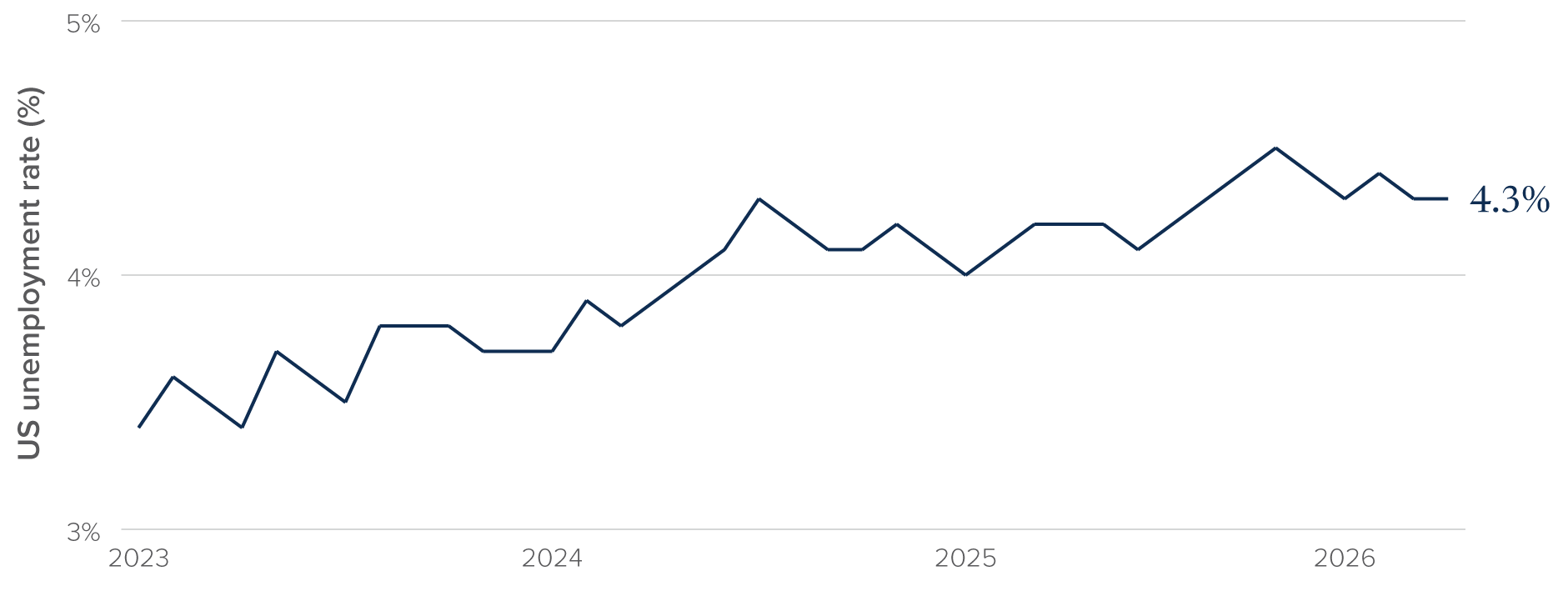

Now let’s look at labour markets, the second leg of the Fed’s mandate. Figure 4 shows the US unemployment rate over the course of the past 3 years.

Figure 4 – US unemployment rate

Source: Bloomberg. As of April 30, 2026.

The US labour market currently sits in an uneasy “low-hire, low-fire” equilibrium. Unemployment has remained relatively stable near 4.3%, not because hiring is strong, but because labour force growth has slowed sharply due to retirements, lower immigration and weaker participation rates. Payroll growth has cooled materially compared with the post-pandemic expansion, job openings have steadily declined and workers are increasingly reluctant to leave existing positions amid concerns about limited alternative opportunities. At the same time, layoffs remain historically low, which has prevented a more pronounced deterioration in headline labour market conditions.

Beneath the surface, however, the market appears increasingly fragile and less dynamic, with hiring concentrated in a narrow set of sectors such as health care and transportation, while many cyclical and white-collar industries stagnate.

These conditions will create a difficult balancing act for Warsh. On one hand, inflation remains well above target due to tariffs, geopolitical energy shocks and persistent service-sector price pressures, arguing for tighter monetary policy or at least a prolonged period of elevated interest rates. On the other hand, the labour market is showing clear signs of fatigue beneath the stable unemployment rate, leaving the economy vulnerable to even a modest rise in layoffs or further slowdown in hiring. Warsh therefore inherits a stagflation-like environment in which the Fed’s dual mandate is increasingly in conflict: fighting inflation would risk weakening an already fragile labour market, while easing policy too early risks reigniting inflation expectations and undermining Fed credibility.

What to expect

Warsh was a staunch inflation hawk in his first term as a Fed Governor (2006–11). Even though the economy was weak following the Global Financial Crisis, he was concerned that easy Fed policy (particularly quantitative easing) would cause an inflation problem down the line.

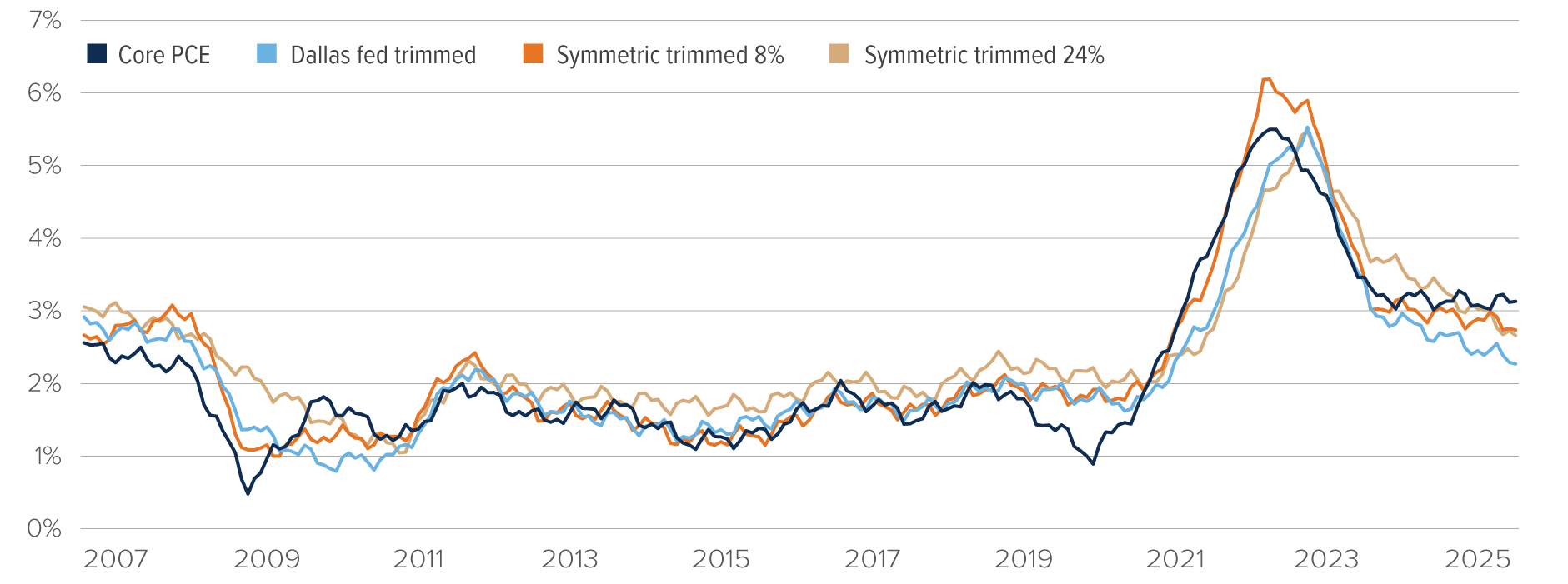

Recently, however, Warsh has taken a dovish stance. Before his nomination for Fed Chair, in the middle of 2025, he called for immediate interest rate cuts, arguing that the Fed is over-reacting to its error on inflation in 2021–22 by keeping policy rates elevated. At his nomination meeting, Warsh said the Fed should look through on-off changes in price levels due to tariffs and geopolitics. He said the Fed should focus on measures of “underlying inflation” and expressed a preference for median and trimmed-mean inflation over the traditional core.

Figure 5 – More than one way to look at inflation

The signal from trimmed-mean inflation measures can vary widely based on the defination of the trim.

Core PCE (% y/y) vs. different types of trimmed-mean PCE inflation.

Source: Mackenzie Investments, BEA, Dallas Fed, BofA Global Research, as of May 26, 2026.

Note: The Dallas Fed metric trims 31% off the top of the monthly inflation distribution, and 24% off the bottom. Our symmetric trims take off 8% and 24% off both sides of the distribution.

Warsh has had less to say on the labour market than inflation. In his nomination testimony, he said that the labour market appears to be around full employment. This is close to the FOMC consensus and, if he sticks with that view, it will be challenging to advocate for rate cuts.

Much of Warsh’s dovishness appears driven by his views on AI. He expects a disinflationary productivity boom due to AI adoption in coming years. He has even argued that the Fed should look through a potential pickup in inflation due to AI investment demand because it would be easily outweighed by the subsequent supply shock from adoption. He has argued that instead of reacting to the data, the Fed should make a forward-looking call on AI-driven disinflation by cutting interest rates. He has said that this is analogous to Chair Greenspan’s bet on productivity during the tech boom of the 1990s.

Warsh is also a balance sheet hawk. In his view, QE subsidized government borrowing. This encourages a fiscal expansion, which ultimately proved inflationary and precipitated rate hikes. There is little doubt that Warsh would like to shrink the Fed’s $6.7 trillion balance sheet. Central bank balance sheet sizes, once right-sized, are determined by its liabilities. The Fed right-sized its balance sheet via QT until money markets reflected tightness in Q4 of 2025. To reduce the balance sheet further, the Fed needs to shrink one of its three key liabilities: currency, Treasury General Account and/or reserves. Reserves are likely the best opportunity for the Fed to reduce its balance sheet going forward.

In his testimony, Warsh said balance sheet cuts would happen slowly and deliberately. That probably means that he has concluded that the Fed will remain in an ample reserve regime.

Additionally, he has said that the Fed should only own Treasury Bills and it should get longer-dated securities off its balance sheet. It seems reasonable to see the Committee going along with the idea that the Fed should not be taking duration risk.

On another front, Warsh wants Fed Committee members to give fewer speeches and he opposes forward guidance. In his view, the more the Fed guides the markets, the less discretion it has in determining policy. He also opposes data dependence because:

- It makes policy backward-looking.

- It could cause markets to be too responsive to the minutiae of data-releases.

It is possible that Warsh will go back to quarterly press conferences and he may attempt to end the process of issuing the Summary of Economic Projections.

Conclusion

Kevin Warsh assumes leadership of the Federal Reserve at a particularly challenging time for investors and policymakers. As Fed Chair, he will have significant influence over interest rates, liquidity conditions, financial markets and the broader economy. His extensive experience spanning Wall Street, the White House and the Fed during the 2008 financial crisis makes him a credible and highly qualified choice to lead the institution.

Warsh inherits an economy where inflation remains stubbornly above the Fed's 2% target despite elevated interest rates. Tariffs, higher energy prices and geopolitical tensions have contributed to persistent price pressures. Meanwhile the labour market, although still relatively stable, is showing signs of underlying weakness through slowing hiring and declining job openings. This creates a difficult policy trade-off between controlling inflation and supporting economic growth.

While once known as an inflation hawk, Warsh has recently advocated a more dovish approach, arguing that the Fed should focus on underlying inflation trends and anticipate the disinflationary benefits of AI-driven productivity gains. At the same time, he remains committed to reducing the Fed's balance sheet and limiting market guidance, suggesting a policy framework that is forward-looking, disciplined and potentially less predictable than that of recent Fed leadership.

Most importantly, he is seen as credible in that he is a strong advocate for Fed independence. It is encouraging that immediately upon Congressional approval, President Trump commented to him “just do your own thing and do a good job”. Good luck Chair Warsh.

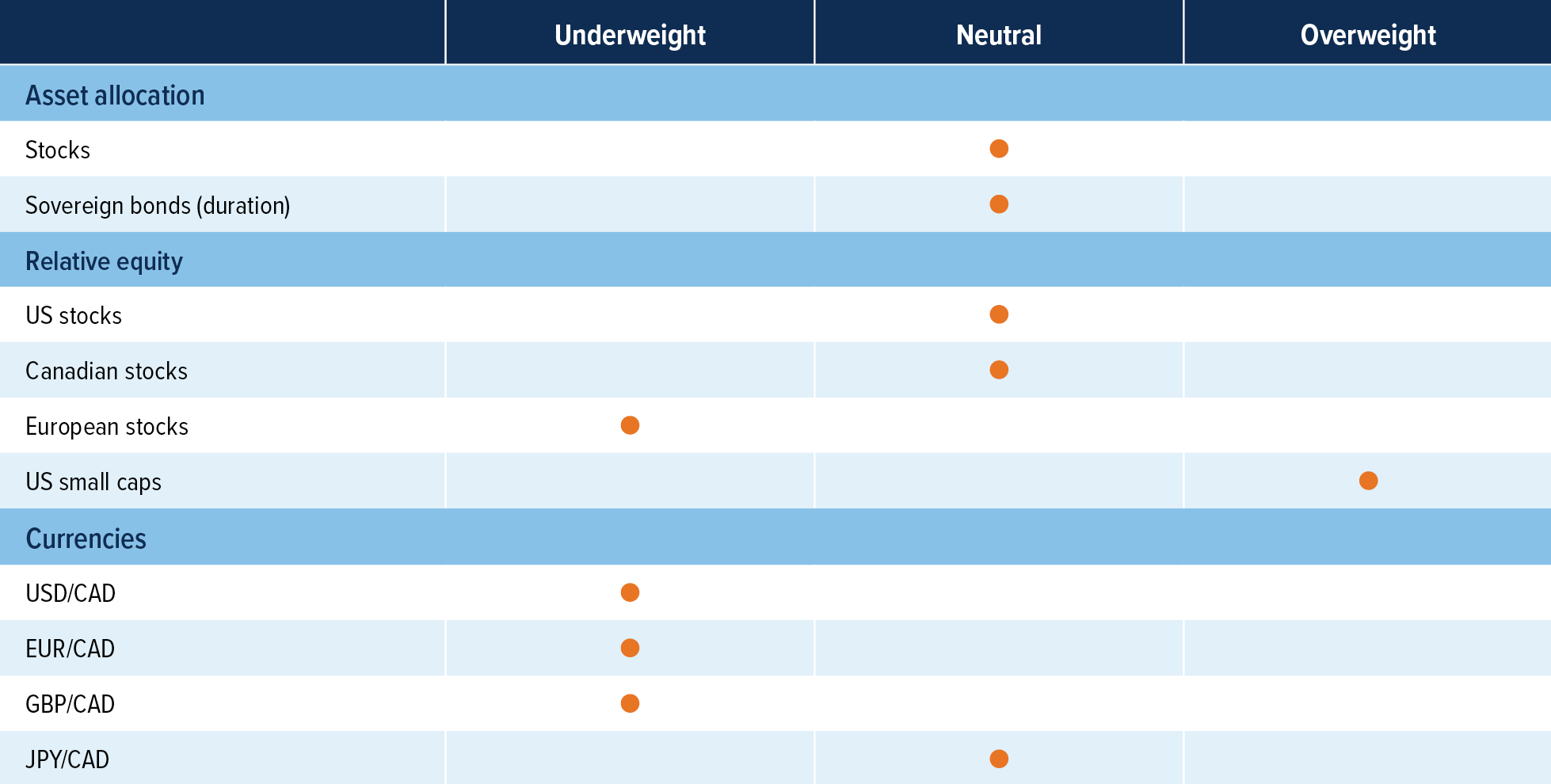

Multi-Asset Strategies Team’s investment views

Tactical summary

Source: Mackenzie Investments.

Note: The opinions expressed in this piece reflect short-term tactical views, which inform the positioning of some of the funds managed by the Multi-Asset Strategies Team.

Positioning highlights

Remain neutral on equities: We continue to remain neutral on equities. Markets have pushed back to record highs in May despite stretched valuations and a still-wide range of outcomes on the Middle East situation. Oil prices and the duration of the Middle East supply shock remain the single largest variable in our outlook, and higher oil prices effectively act like a tax on consumers and businesses alike. We see the risk-reward as balanced at these levels and prefer to express our views through relative positioning rather than outright equity beta.

Remain neutral on bonds: We remain neutral on bonds. Central banks remain caught between sticky energy-driven inflation on one side and slowing growth signals on the other, leaving the near-term path for policy rates highly uncertain.

Sell Europe and buy US small caps: We are rotating out of Europe and into US small caps. Europe is the most exposed developed region to the Middle East energy shock. In contrast, US small caps derive 70-80% of revenue domestically and are less exposed to imported energy.

Currencies: USD remains overvalued, and our long-term view is for the USD to depreciate versus most developed countries. We continue to like CAD and JPY as the best plays for this view. With oil still holding up at a higher level, it should be supportive for Canada’s economy compared to other currencies, especially the EUR and GBP.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently, and past performance may not be repeated. The content of this material (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it. This material contains forward-looking information which reflects our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of May 26, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise. Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in the investment products that seek to track an index.