Navigating US small caps with a disciplined quantitative approach

IN THIS ARTICLE min read

Key takeaways

US small caps offer significant growth potential, but wide dispersion in company outcomes creates both opportunity and risk. A disciplined quantitative approach can help investors capture this opportunity by consistently evaluating a broad universe of stocks, translating research insights into diversified portfolios and managing liquidity, trading costs and unintended risk exposures.

How a structured quantitative approach helps capture opportunity while managing risk in US small cap investing

US small caps can deliver significant growth, but their returns can vary widely. Some businesses thrive, while others struggle, especially during periods of economic uncertainty. That wide gap in outcomes, known as dispersion, creates both opportunity and risk for investors.

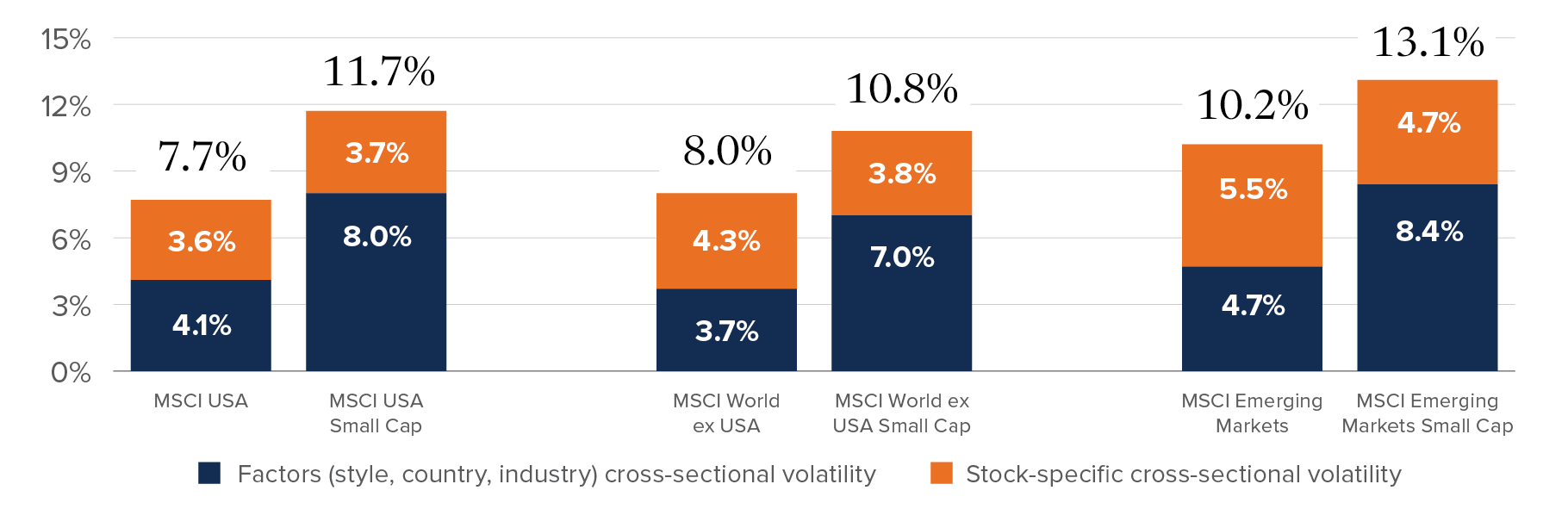

FIGURE 1: Greater return dispersion in small caps

Small caps exhibit higher total dispersion, creating greater potential for alpha through stock selection

Total dispersion, or cross-sectional volatility (CSV) = stock-specific CSV + factor-driven CSV.

Source: Morningstar. Analysis period: January 2002–September 2023. Monthly averages. Cross-sectional volatility (CSV) calculated using the MSCI Global Equity Model for Long-Term Investors (GEMLT).

Wider dispersion can increase the potential value of active stock picking, but it can also magnify implementation challenges. Liquidity varies widely across small cap stocks, and trading costs can rise quickly in volatile markets.

Higher dispersion in small caps creates greater opportunity for stock selection

Small cap returns often depend more on which companies are owned than on the overall direction of the market. When dispersion is high, the opportunity set for stock selection can expand because the market differentiates more sharply across business models, balance sheets and earnings resilience.

A quantitative approach can help by applying a consistent lens across a wide set of companies and updating that assessment as new information arrives, without relying on a narrow narrative or a limited research list.

Why discipline matters as much as opportunity

Small cap investing can be unforgiving without strong risk and implementation discipline. Liquidity conditions can change quickly, and trading costs can become a meaningful driver of outcomes.

The practical implication is that stock selection works best when paired with portfolio construction that manages exposures, and with implementation practices that reflect real trading conditions.

How a quantitative approach is applied in the Mackenzie GQE US Small Cap Fund

The Global Quantitative Equity (GQE) Team manages the Mackenzie GQE US Small Cap Fund using a quantitative investment process designed to consistently evaluate a broad universe, translate research insights into diversified holdings and maintain clear risk guidelines across changing market conditions.

Core portfolio profile Maintain balanced exposure across value, growth and quality, avoiding over-reliance on any one style and supporting more consistent outcomes across market cycles. | Nimble, yet disciplined Models are updated daily so the portfolio’s view of the opportunity set remains current. Updates only apply to a small fraction of the portfolio. |

Research-led security selection Signals are grounded in economic rationale and empirical evidence, with an emphasis on robustness and diversification across return drivers. | Risk-managed implementation Risk controls help keep active risk aligned with intended sources of return, limiting unintended factor, sector or concentration exposures. |

Stock selection is expressed through diversified exposure to several return drivers, rather than relying on a single style. Portfolio construction seeks to translate research signals into target holdings while managing exposure limits, and implementation considerations help focus activity where the expected benefit is more likely to justify trading costs — particularly in more volatile markets.

Investment implications for investors

Small caps can offer meaningful opportunity because company outcomes can differ widely, especially during periods of uncertainty. That same dispersion increases the importance of a disciplined approach that combines stock selection, portfolio construction and cost- and liquidity-aware implementation.

The Mackenzie GQE US Small Cap Fund combines these key features within a single integrated framework. The result is a quantitative approach designed to evaluate a broad opportunity set while managing risk across changing market environments.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. The content of this page (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

©2026 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.