Invest with a broader perspective on energy.

With our deep expertise across the entire resource and energy value chain, we uncover opportunities others miss.

IN THIS ARTICLE min read

The energy transition is entering a new phase of growth and investment, driven by rising demand, innovation and global system expansion. For investors and advisors, this creates a powerful opportunity set, across energy, infrastructure and materials—making thoughtful capital allocation key to capturing long-term value.

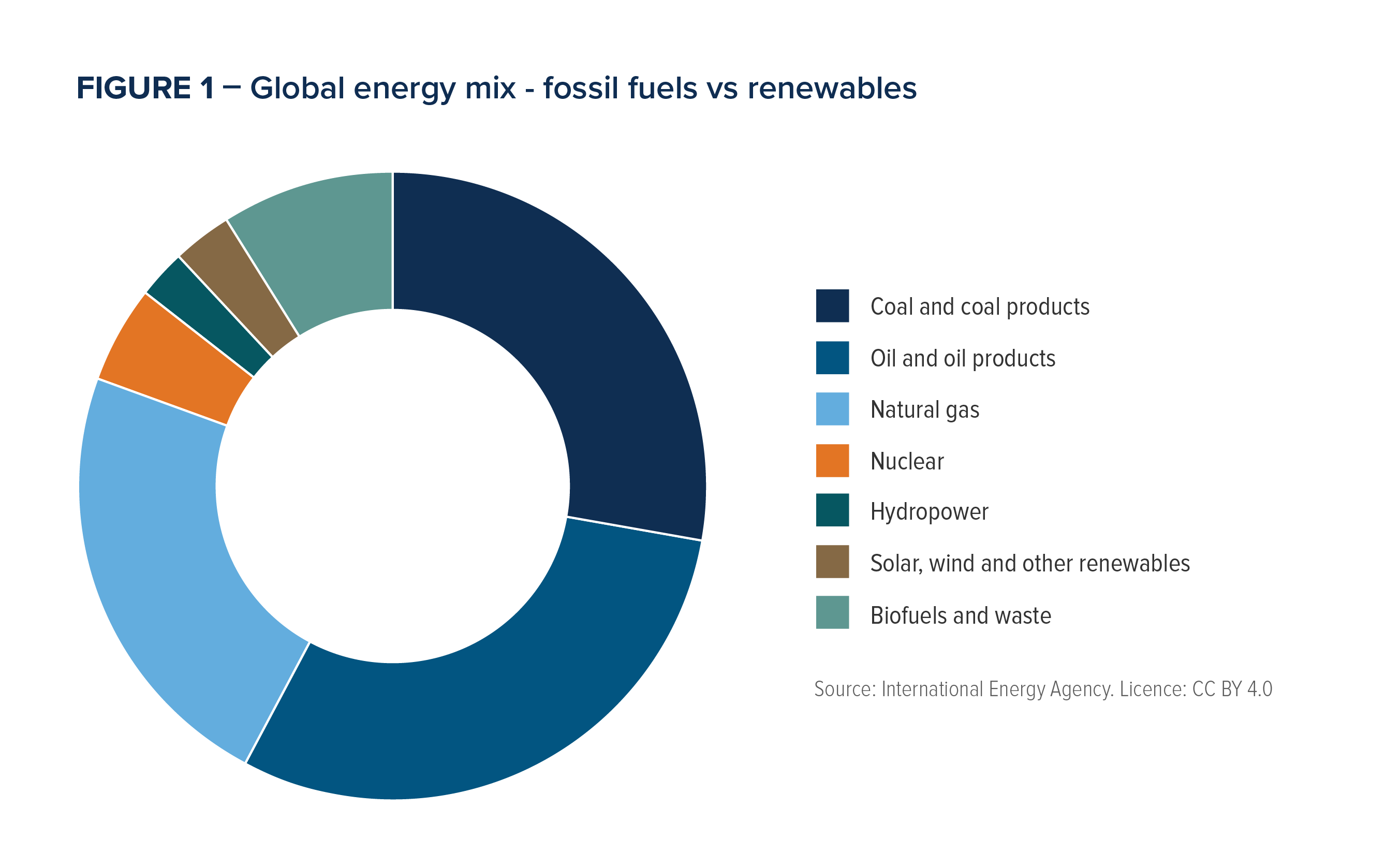

For much of the past decade, the energy transition was framed as a relatively straightforward shift, from fossil fuels to renewable energy. However, that narrative no longer reflects the reality of the system we are trying to build. Today, despite the approximate $15 trillion1 invested in clean energy and related technologies over the past two decades, the global energy system remains overwhelmingly dependent on fossil fuels, which still account for roughly 80% of total energy consumption.2

At the same time, many clean technologies, such as hydrogen and long-duration storage, face challenges related to scale, system integration and economic competitiveness in certain applications.

After decades of relatively flat growth, global electricity demand is now expected to grow at a 3–5% annual rate3, driven by electrification, artificial intelligence, industrial reshoring and population growth. By 2050, the global population is projected to approach 10 billion people, with nearly 70% living in urban environments—all requiring housing, transportation, cooling and digital infrastructure.4

The implication is clear: the transition is no longer about replacing one system with another. It is about expanding the entire system to meet significantly higher levels of demand.

This shift introduces a more complex set of constraints.

The energy transition is increasingly shaped by a “trilemma” of competing priorities: sustainability, security and affordability.5 While climate remains a critical driver, it is no longer the only one. Geopolitical tensions, supply chain vulnerabilities and rising costs are playing an equally important role in shaping how the system evolves.

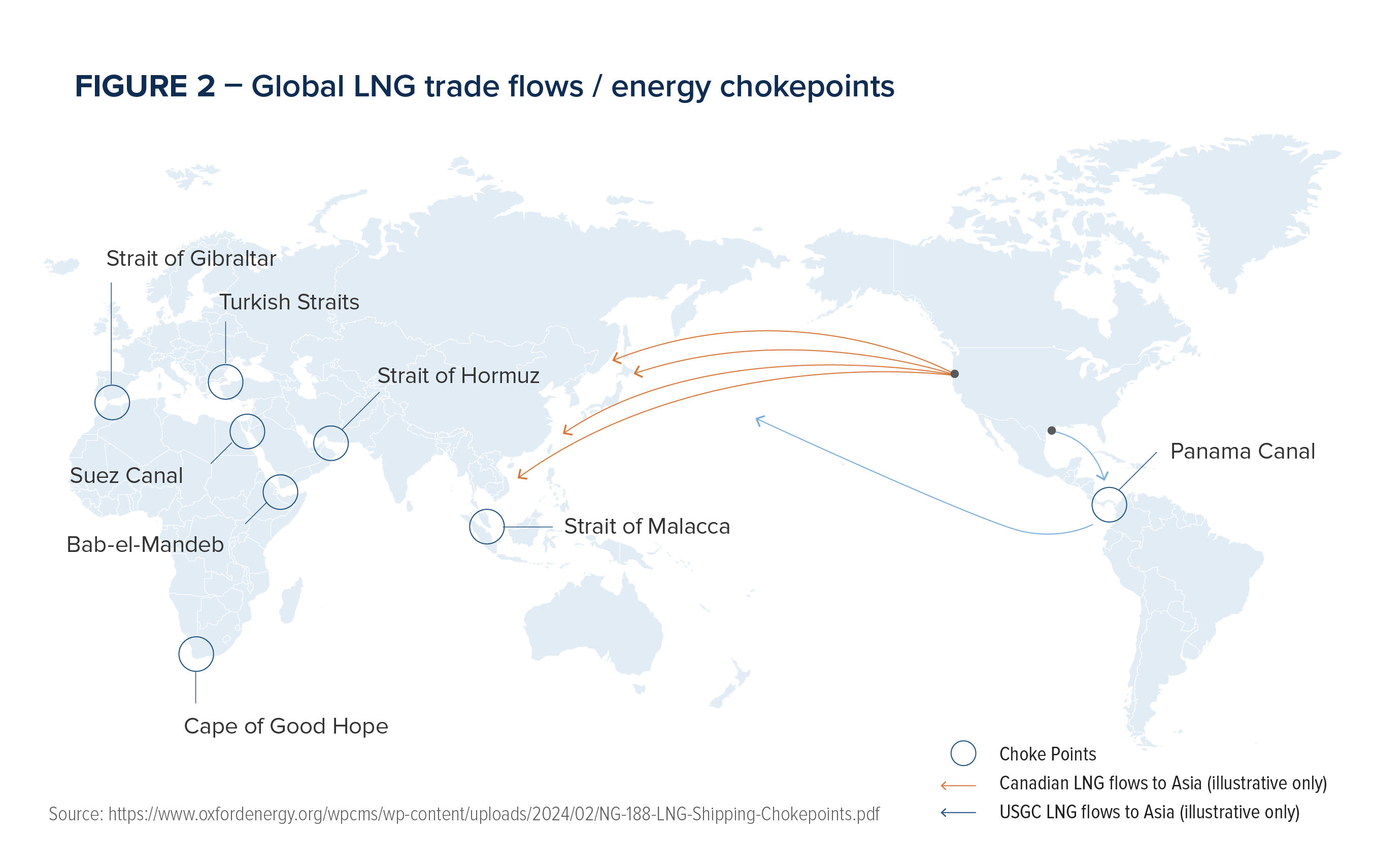

Recent events highlight how quickly these priorities can shift. Roughly 20% of global oil supply flows through the contested Strait of Hormuz, underscoring the fragility of global energy logistics.6

At the same time, Europe’s pivot away from Russian gas has reinforced how energy security can override long-term climate considerations in the short term.

Despite the growth of renewables, fossil fuels remain central to the global energy system. Approximately 60% of global electricity generation still comes from fossil fuels, compared to about 30% from renewables and 10% from nuclear.7

However, roles are changing.

To achieve the transition and meaningfully address climate change, humans will need to become more selective when deploying capital within traditional energy. Over time, this implies greater investment in operators that can deliver energy at lower cost, with lower emissions and with stronger governance. This will increasingly create a divide within the sector, between assets that remain competitive in a carbon-constrained world and those that face structural decline.

Natural gas, for example, continues to play a critical role as a “bridge fuel”, while technologies such as carbon capture are extending the viability of higher-emission assets within a more integrated energy system.

While much of the focus remains on energy generation, one of the most significant constraints sits further upstream: minerals and materials.

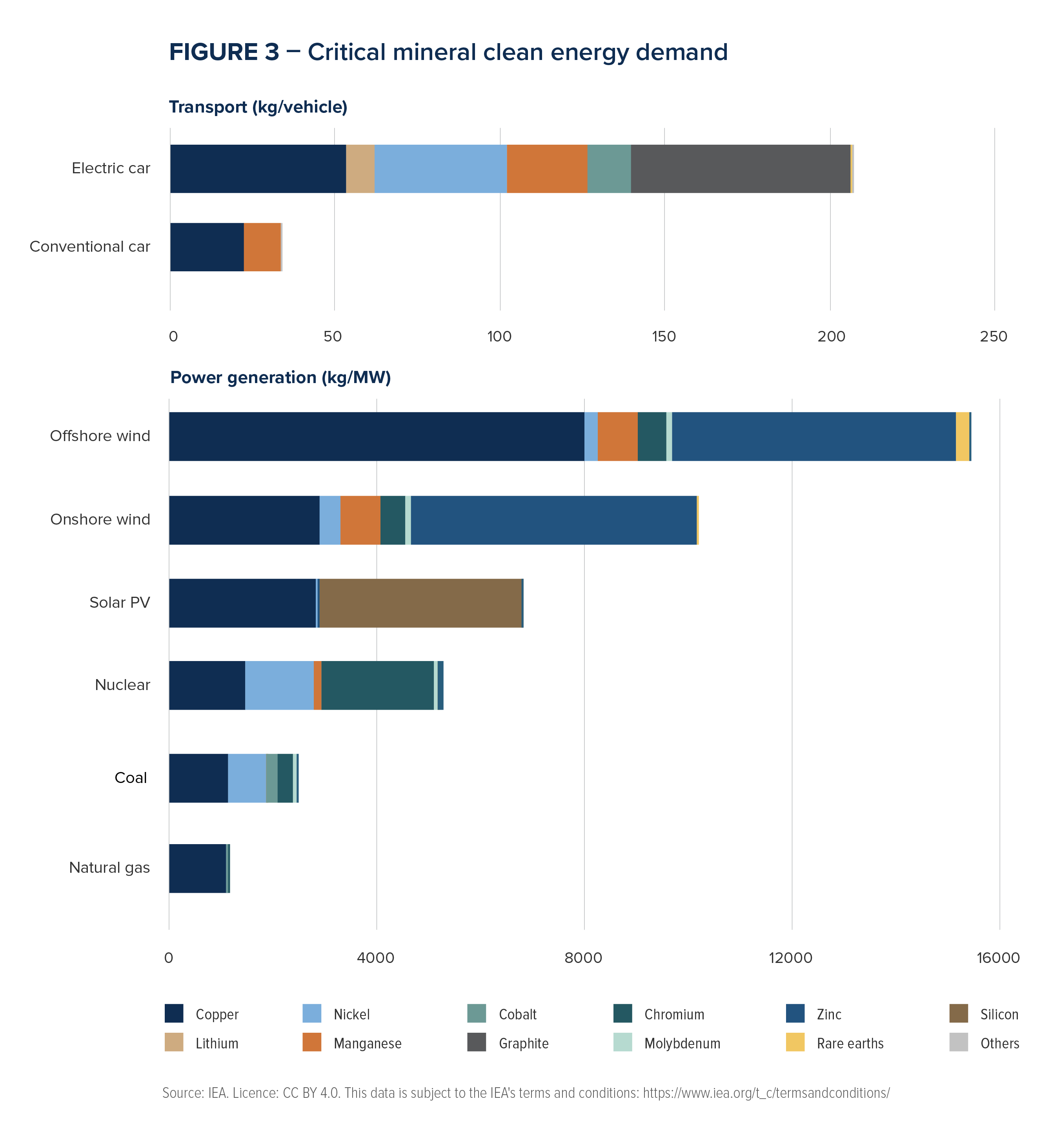

Clean energy systems are far more resource-intensive than traditional ones. An electric vehicle requires approximately six times more mineral inputs than a conventional car, while wind and solar infrastructure require significantly more materials than hydrocarbon-based generation.8

This is expected to drive a sharp increase in demand. For example, global copper production, currently around 25 million tonnes annually, may need to double to 50 million tonnes by 2050 to meet electrification targets.9

Yet supply is not keeping pace. Projections already indicate a 10 million tonne shortfall in copper, or roughly 25% below expected demand.10

Notes: kg = kilogramme; MW = megawatt. Steel and aluminium not included.

This imbalance is structural, not cyclical. It reflects years of underinvestment, long project lead times and increasing geopolitical concentration in both mining and processing. Today, countries like China dominate not only production, but also refining capacity, creating additional vulnerabilities in global supply chains.

As the system becomes more capital-intensive, affordability is emerging as a critical pressure point. The transition requires trillions of dollars in new investment, across grids, generation, storage and supply chains. Increasingly, these costs are being absorbed by governments and public balance sheets, rather than end users. This introduces fiscal constraints and raises questions about how much cost can realistically be borne by taxpayers and ratepayers.

At the same time, new demand sources, such as AI-driven data centres, are beginning to reshape electricity markets, with some large users securing power through private, “behind-the-meter” arrangements. This creates a more fragmented and potentially unequal pricing structure within energy systems.

For investors, these dynamics mark the beginning of a new investment cycle.

The opportunity is no longer about choosing between “old” and “new” energy. It is about understanding how value is created across a system that is becoming more interconnected, more constrained and more capital-intensive.

Opportunities span the full energy ecosystem:

At the same time, volatility is likely to remain elevated, driven by geopolitical events, supply constraints and shifting policy environments.

Ultimately, the energy transition is not just an energy story, but it is a capital allocation story.

The defining challenge is not simply building more but deploying capital effectively across a system constrained by resources, infrastructure, and competing priorities. Success will depend on the ability to navigate trade-offs, identify structural bottlenecks, and allocate capital with discipline.

The path forward is not linear, but the direction is clear: the global energy system is being rebuilt, and the scale of that transformation represents one of the most significant investment opportunities of the coming decades.

Mackenzie supports the investment opportunity tied to building a new global energy system and has two investment teams – the Mackenzie Greenchip and Mackenzie Resource teams – directly focused on this. Both teams understand the shared importance of natural resources and renewable technologies, allowing investors to invest directly in the future of energy, literally from ground to grid.

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. The content of this page (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document may contain forward-looking information which reflect our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of April 1, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.