The long-term wealth advantage of private markets

IN THIS ARTICLE min read

The power of compounding and the benefit of thinking long-term

One of the most powerful forces in investing is compound growth — the ability for returns to generate their own returns over time. Even small differences in annual returns, say 1% or 2%, can have an outsized impact when allowed to compound for decades.

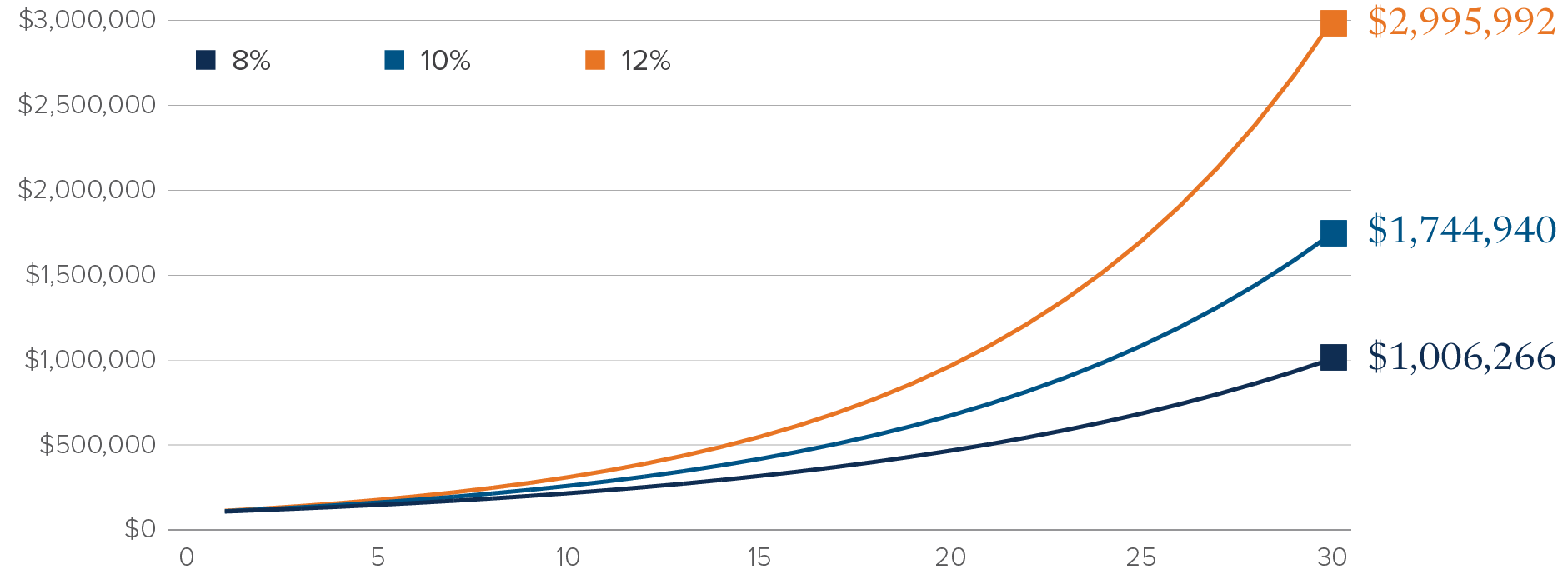

As Figure 1 shows, the difference between an 8% and 10% return can result in more than a 70% increase in wealth, proof that even modest gains can transform outcomes for investors who stay the course.

In a world where traditional portfolios can feel like they’re hitting a ceiling, finding new ways to let growth build on itself has never been more important.

Figure 1: Why small differences matter

Compounding of $100,000 over 30 years at various growth rates

For illustration purposes only.

For illustration purposes only.

Expanding compounding opportunities through private markets

For decades, the traditional 60/40 portfolio has served investors well, balancing growth and stability. But in today’s environment of lower yields and higher volatility, many investors are finding that the traditional approach no longer delivers the growth it once did.

Generating consistent alpha has become harder; recent data shows that only about 41% of active managers in the global or foreign equity space have outperformed their passive peers between July 2024 and June 2025.1

Because traditional portfolios of public securities exist in the daily spotlight, investors are often prompted to react to headlines and chase short-term performance. This behaviour can lead to emotionally driven buying and selling — actions that disrupt compounding and long-term planning.

One of the most compelling developments in recent years is the expanded access to private markets, including private equity, private credit and infrastructure, for accredited investors. By tapping into return sources not typically available in public markets, investors can potentially strengthen the compounding engine that builds long-term wealth.

How private markets strengthen compounding

Private markets enhance compounding through three interconnected forces: the illiquidity premium, value creation and structural stability.

1. The illiquidity premium

Investors earn this premium by committing capital for longer periods and accepting less frequent liquidity. Because private assets are not traded daily, managers can take a long-term view focused on value creation, not market timing. Historically, this patient approach has rewarded investors with higher average returns — an important tailwind for compounding over time.

2. Value creation: accelerating compounding from within

Private market managers do more than simply buy and hold assets — they actively work to improve them. A private equity manager might help a business expand into new markets or modernize operations; an infrastructure manager may enhance efficiency or renegotiate contracts; private credit lenders can structure financing that provides higher yields and stronger protections.

These active improvements directly accelerate compounding by increasing an asset’s intrinsic value. For investors, that means returns are built not just on what markets deliver, but also on what skilled private equity management teams can create — compounding from a stronger foundation.

3. Stability and long-term focus

Private markets often appear less volatile than public markets — and that stability is more than just a result of infrequent pricing. Private assets are typically valued based on fundamentals and durable cash flows, not day-to-day investor sentiment. Their governance structures promote discipline and sustainable growth rather than quarterly results.

This structure helps investors stay invested through full economic cycles, a critical condition for compounding to work effectively. Private markets also help investors avoid the costly mistake of reacting to short-term volatility — supporting the patience that meaningful compounding demands.

The portfolio effect: a modest shift, a lasting impact

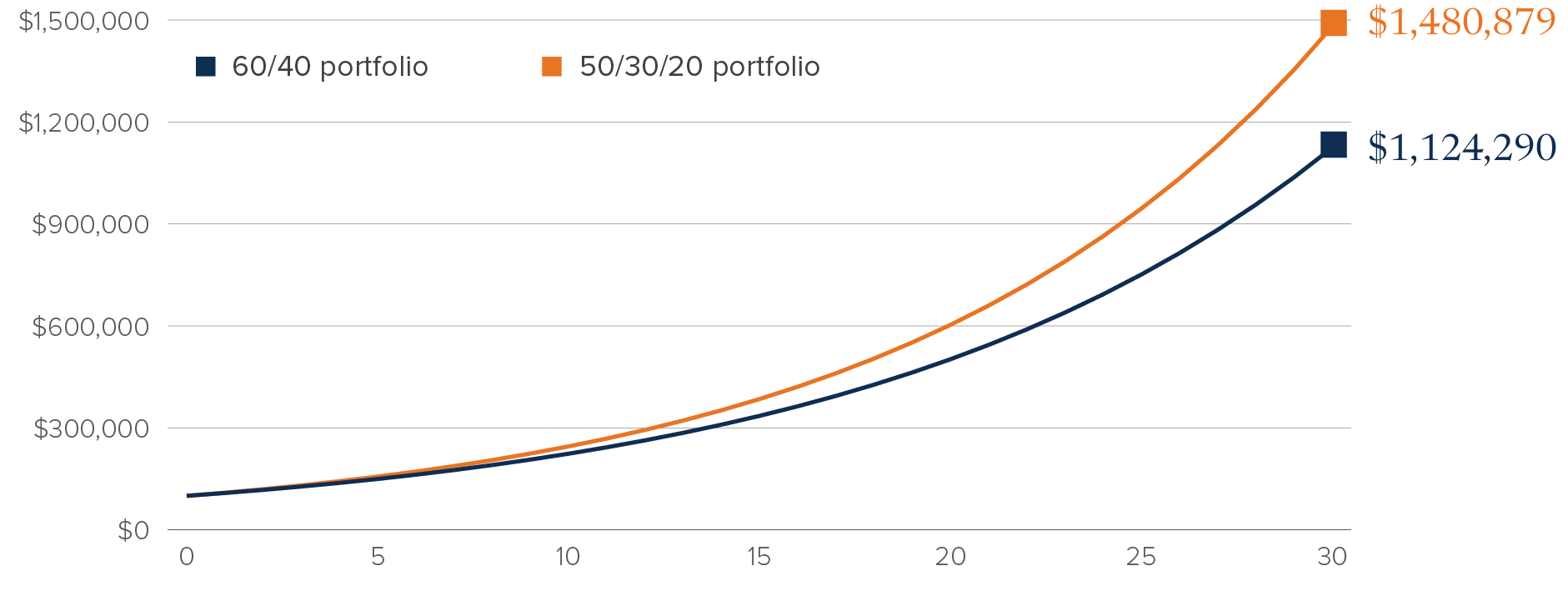

Even a modest allocation to private markets can reshape a portfolio’s long-term trajectory. Figure 2 compares a traditional balanced portfolio with one that includes private market exposure:

Figure 2: 30-year growth comparison of 60/40 vs. 50/30/20 portfolios assuming a 1% return uplift on the private allocation

For illustrative purposes only. The 60/40 portfolio assumes 60% allocation to equities growing at a CAGR of 10% and 40% allocation to bonds growing at a CAGR of 6% resulting in a weighted average CAGR of 8.4%. The 50/30/20 portfolio assumes 50% allocation to equities growing at a CAGR of 10%, 30% allocation to bonds growing at a CAGR of 6% and 20% allocation to private markets growing at a CAGR of 13% resulting in a weighted average CAGR of 9.4%.

That single percentage point of additional return compounds to a $365,000 advantage over three decades — achieved with potentially lower volatility and improved diversification. For many investors, that additional wealth could mean retiring earlier, supporting future generations or giving back through philanthropy — tangible possibilities from disciplined compounding.

Building durable wealth through patience

Compounding rewards time, patience and discipline. Private markets reinforce these traits by giving investors access to differentiated sources of return that complement public assets and extend their investment horizon.

In the end, the advantage of private markets lies not only in their potential for higher returns, but in their ability to help investors stay patient and purposeful. Allocating even modestly can be a first step toward thinking differently about how time — not timing — builds wealth that lasts.

1 “Active Managers Face Mounting Difficulty Generating Alpha” — The Wealth Advisor, August 7, 2025. https://www.thewealthadvisor.com/article/active-managers-face-mounting-difficulty-generating-alpha

For accredited investors only (as defined in NI 45-106). Past performance is not necessarily indicative of any future results.

This document may contain forward-looking information which reflect our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of December 2024. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.