Over the past decade and a half, “US exceptionalism” has dominated global equity markets, with the S&P 500 commanding an outsized share of investor attention. Too often, this has meant ignoring the compelling opportunities in a less celebrated corner of the market: US mid-cap value stocks.

As at the end of 2024, the mid-cap category accounted for over 20% of the market capitalization of the Russell 3000 Index (representing approximately 98% of investable US equities).1 As a percentage of all US equity assets however, it accounted for roughly 6%, less than a third of their “appropriate” weighting2.

This often overlooked “forgotten middle” offers strong potential for returns and significant liquidity, often at attractive valuations.

Positioned to perform

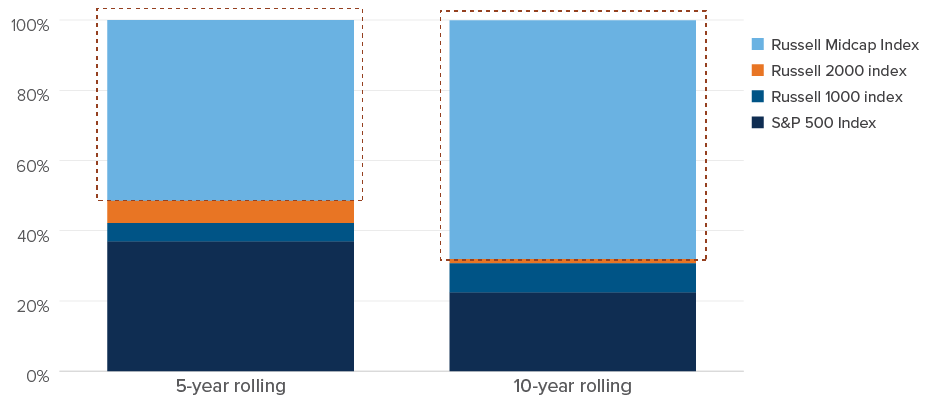

The cohort represents a risk/return lifecycle “sweet spot” within the US market. Mid cap stocks have tended to outperform over time, with fundamentals — such as high return on invested capital (ROIC) or the ability to generate consistent cash flows — proving to be a more reliable driver of returns than speculation. Over the past 30 years, the Russell Midcap Index has outperformed the large cap Russell Top 200 Index, the Russell 1000 Index and the small cap Russell 2000 Index a majority of the time, over five- and 10-year rolling bases (see Figure 1).

FIGURE 1 – Top performing index over past 30 years (one-month steps)

Source: FactSet, SPAR. As at September 30, 2025.

Source: FactSet, SPAR. As at September 30, 2025.

From alpha to beta

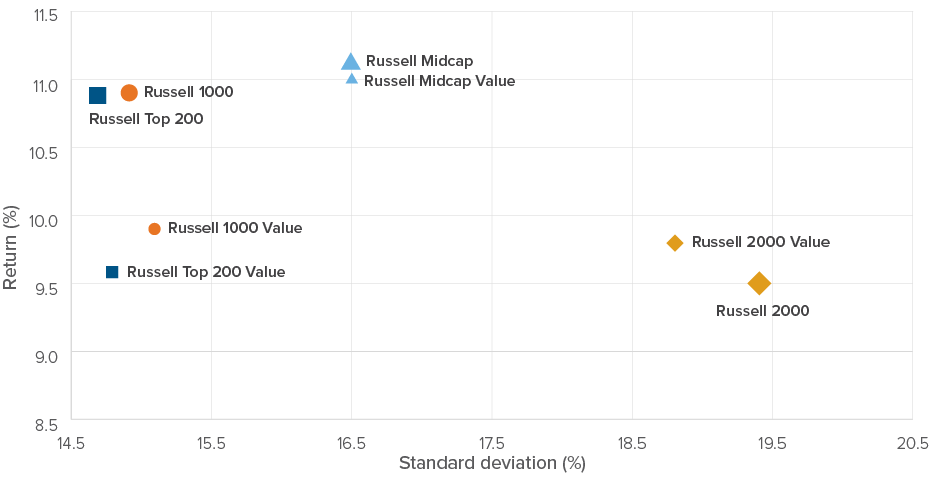

Mid cap stocks are also able to deliver performance with only a marginal increase in volatility, relative to their large cap counterparts. Their long-term risk-adjusted returns, as measured by their Sharpe ratio, are on par with larger cap holdings and significantly ahead of the small cap cohort (see Figure 2). Mapping the historic returns and volatility (as measured by standard deviation) of the Russell indices and value sub-indices helps paint an undeniably compelling picture in favour of mid caps, both core and value.

FIGURE 2 – Russell core indices since common inception Sept. 1, 1992 vs. Russell value indices since common inception Feb. 1, 1995

Source: eVestment as at December 31, 2025.

Source: eVestment as at December 31, 2025.

Do you have the exposure you think you have?

Active investors commonly seek mid cap exposure by coupling a large cap manager with a small cap manager on the assumption that the former will trade down sufficiently below the cap scale for the benchmark, with the latter seeking to do the reverse. This view is at odds with reality, however. The average large cap core strategy has a weighted average market cap of over $800 billion, suggesting a strong bias for mega caps, compared to less than $80 billion for the average mid-cap core strategy. For small caps, the average core strategy has a weighted average market cap of just over $5 billion, some way short of the mid cap’s aforementioned $80 billion average.

Similar issues arise when adopting a passive approach. Broad-based indices like the S&P 500 and Russell 1000 are market-cap weighted, so their returns are dominated by larger stocks. While the Russell Midcap Index comprises the smallest 800 companies in the Russell 1000 Index, the largest 200 stocks represent about 80% of the index, with the five largest accounting for circa 25%.3

Under-analysed, not just under-owned

It’s long been the case that, relative to large cap stocks, mid caps tend to enjoy markedly lower sell-side analyst coverage. For example, it’s not uncommon for institutional mandates to restrict investment in mid caps, leading to less attention from institutional managers. This allocation “blind spot” results in wider variance in mid cap valuations and, as a result, a greater opportunity for the active investor to generate alpha.

Value is still inexpensive

As a sub-set of the broader mid cap space, mid-cap value hasn’t traded this cheaply versus growth since the tech bubble, with only the pandemic years of 2020–2021 as exceptions.

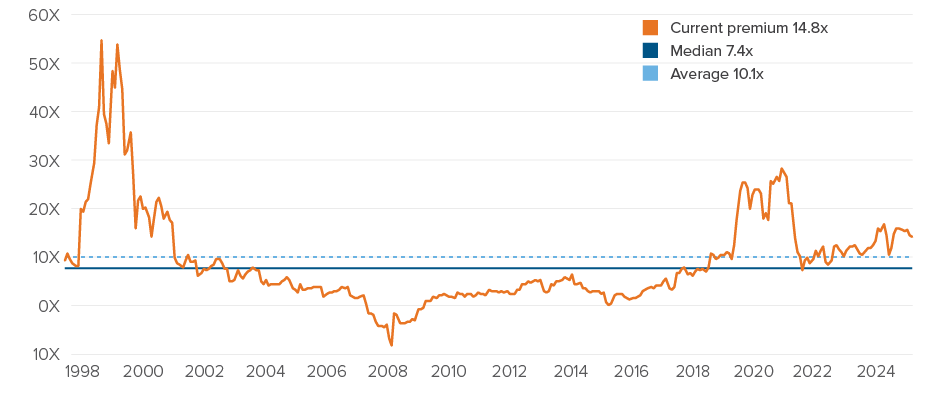

As at year-end 2024, the Russell Midcap Value Index traded at 17.5x FY1 estimated earnings while the Russell Midcap Growth Index traded at 33.2x, a spread of 15.7. Contrast this with the fact that the average and median valuation spreads have been 9.8x and 6.7x respectively over the past 25 years. It is by no means certain when, and to what extent, the valuation premium for large cap and growth stocks will recalibrate but it’s safe to say that the current differential stands mid-cap value in good stead going forward.

FIGURE 3 – Relative 1-year Forward P/E: Russell Midcap Growth Index – Russell Midcap Value Index

As at December 31, 2025. Source: FactSet. P/E ratios are based on forward one-year consensus earnings estimates of the Russell Midcap Value and Russell Midcap Growth indices using monthly figures.

Mid-cap value stocks also offer a bigger pond to fish in. Examining the variation in the number of constituent stocks within the Russell Midcap Growth and Russell Midcap Value indices over the last 20 years, the number of stocks within the growth universe (288) is currently at its lowest point over that period — and indeed ever — while the value universe is currently almost 150% larger (713).

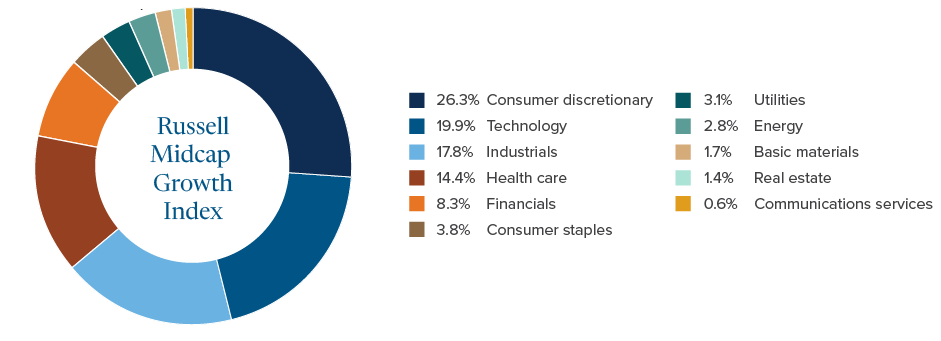

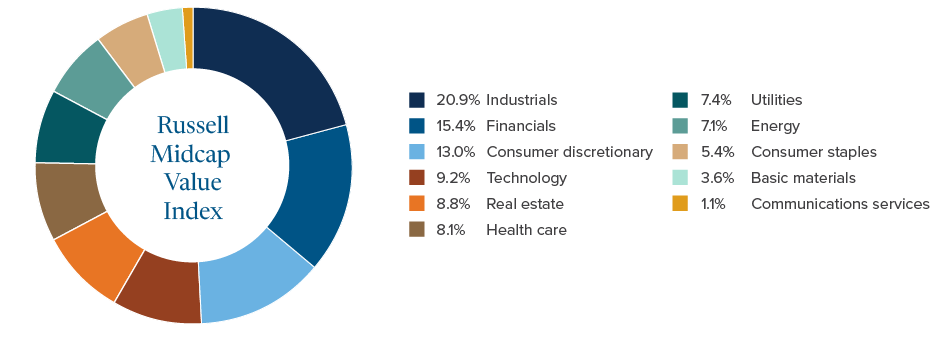

An analysis at the sector level, for example, also highlights important disparities. The Russell Midcap Growth Index as at March 30 2025, had a 30% weighting to technology, the highest ever, and more than three times higher than its value equivalent. It’s difficult not to see this as a risk for allocators — but one that can be readily reduced by revisiting mid-cap value where concentration levels remain in line with historic experience.

Russell Midcap Growth Index, as at November 30, 2025

Russell Midcap Value Index, as at November 30, 2025

Source: London Stock Exchange Group

Source: London Stock Exchange Group

Looking ahead

There is good cause for optimism on a number of fronts. Analyst projections show mid-cap earnings growth inflecting to the upside, with current year estimates exceeding large caps and, importantly, at lower valuations.

While key elements of the Trump administration’s policy remain difficult to predict, tariffs and other trade initiatives designed to stimulate US-based production are likely to prove advantageous, given that most US mid-caps are domestic. Similarly, whilst the prospect of declining corporate tax rates would bolster all US stocks, incremental tax breaks for US production would further benefit the mid-cap cohort.

It's time to look again at that “forgotten middle”.

_____________________

1 Source: FTSE Russell.

2 Source: eVestment.

3 Source: FTSE Russell.

This article may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of December 31, 2025. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in the investment products that seek to track an index.