Time to revisit global diversification

IN THIS ARTICLE min read

The case for EAFE

In today’s dynamic market landscape, the importance of international diversification cannot be overstated. The MSCI EAFE Investable Market Index (IMI), which serves as the benchmark for the Mackenzie International All Cap Fund, covers small, mid and large-cap companies across 21 developed markets outside North America. This broad exposure is particularly relevant in an era marked by deglobalization and capital fragmentation.

The concentration risk in US markets is becoming increasingly pronounced. The top 10 holdings in the S&P 500 now account for 36% of the index, compared to just 11% in the MSCI EAFE IMI. Furthermore, the US dominates 71% of the MSCI World Index, raising concerns about genuine global exposure. By incorporating EAFE equities into portfolios, investors can mitigate single-market and single-sector risks, achieving a more balanced and diversified investment strategy.

Why all-cap matters

In a world trending toward regionalization, EAFE small and mid-cap firms — often more domestically focused — are better insulated from global trade shocks. An all-cap approach captures the full spectrum of opportunity, from resilient local players to globally competitive large caps, positioning investors for regional growth tailwinds.

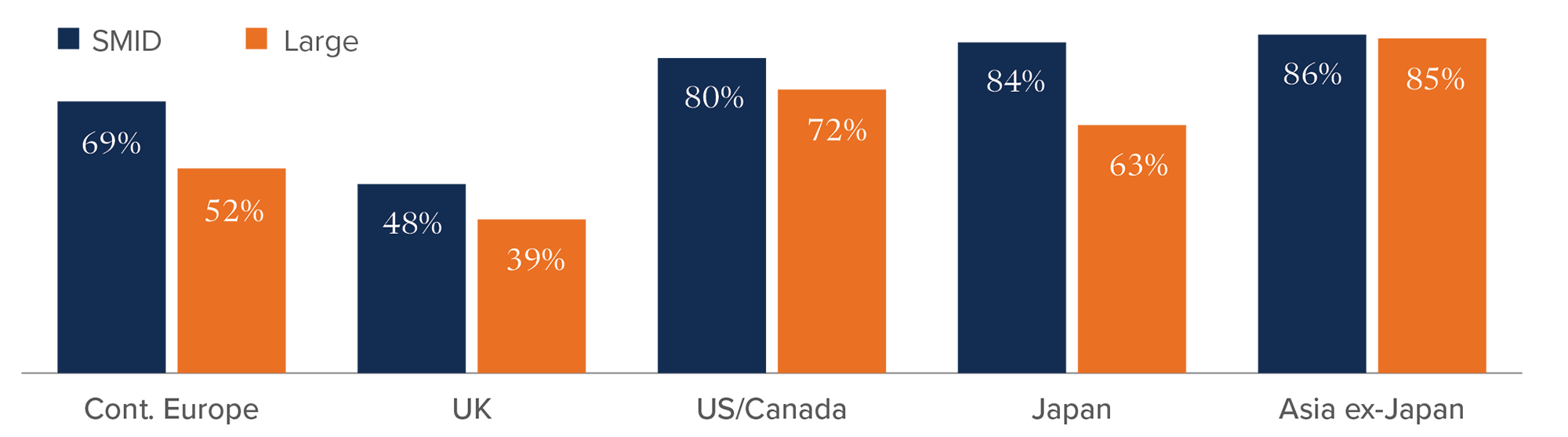

Domestic revenue share

Small-to-mid cap (SMID) has greater domestic exposure and is less reliant on global trade

Source: JP Morgan

Source: JP Morgan

Europe’s reinvestment shift

Europe is undergoing a structural shift. Moving past its austerity-era constraints, the region is embracing bold fiscal initiatives. Germany, once a symbol of fiscal restraint, is now prioritizing growth via an infrastructure fund exceeding €500 billion.

Defence investment is also rising rapidly, catalyzed by geopolitical tensions. Europe is rebuilding its industrial and military backbone, with implications for aerospace, cybersecurity and high-value manufacturing.

Closing the growth and valuation gaps

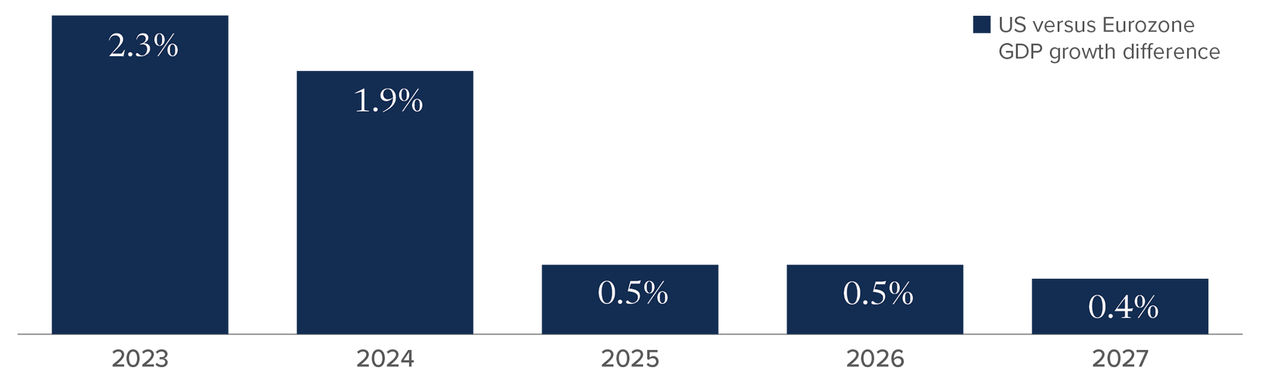

While the US has enjoyed stronger growth recently, the transatlantic GDP gap — 2.5% in 2023 — is projected to narrow to 0.5% by 2027. As economic growth converges, so may valuations: European equities, notably the MSCI Europe, trade at roughly 14× forward earnings versus 22× for the MSCI USA. Much of the skepticism surrounding Europe appears already priced in, presenting upside potential if fundamentals continue to improve.

US/Europe GDP growth gap

Source: Bloomberg

Source: Bloomberg

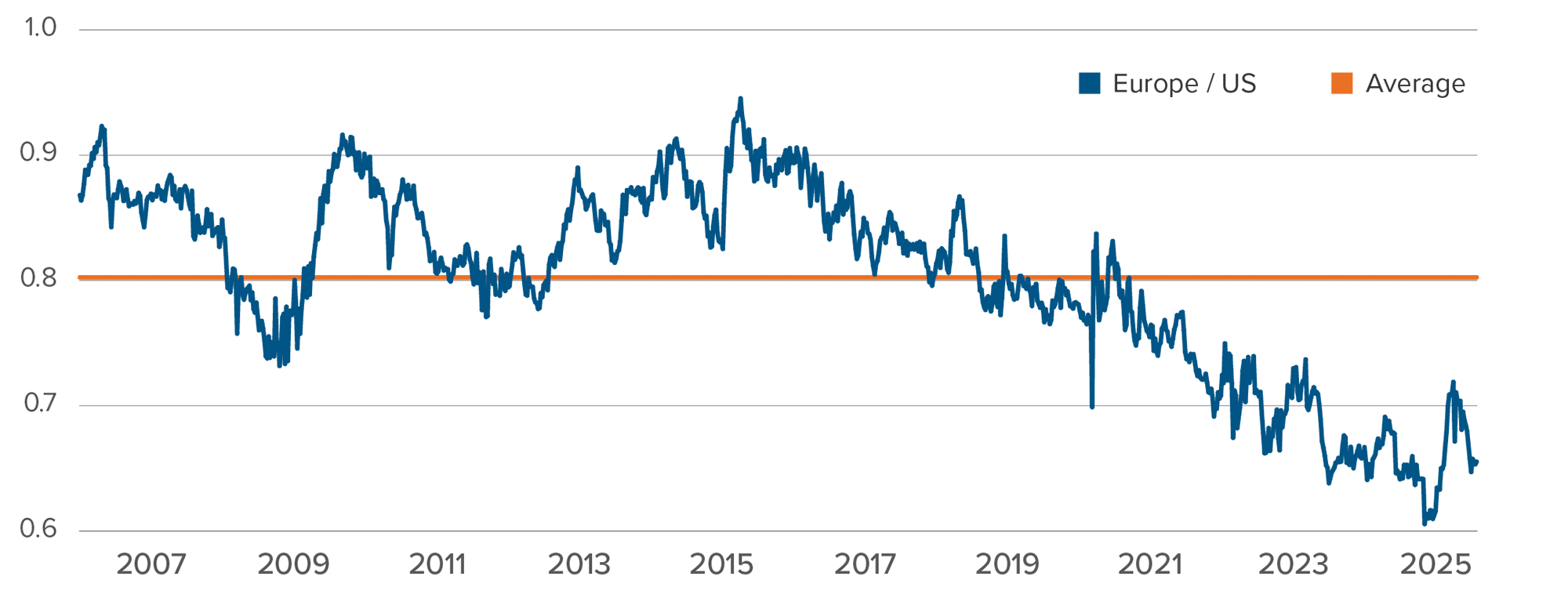

12-mo Fwd PE: MSCI Europe vs. MSCI USA

Source: Bloomberg

Source: Bloomberg

Consumer and fiscal fundamentals improve

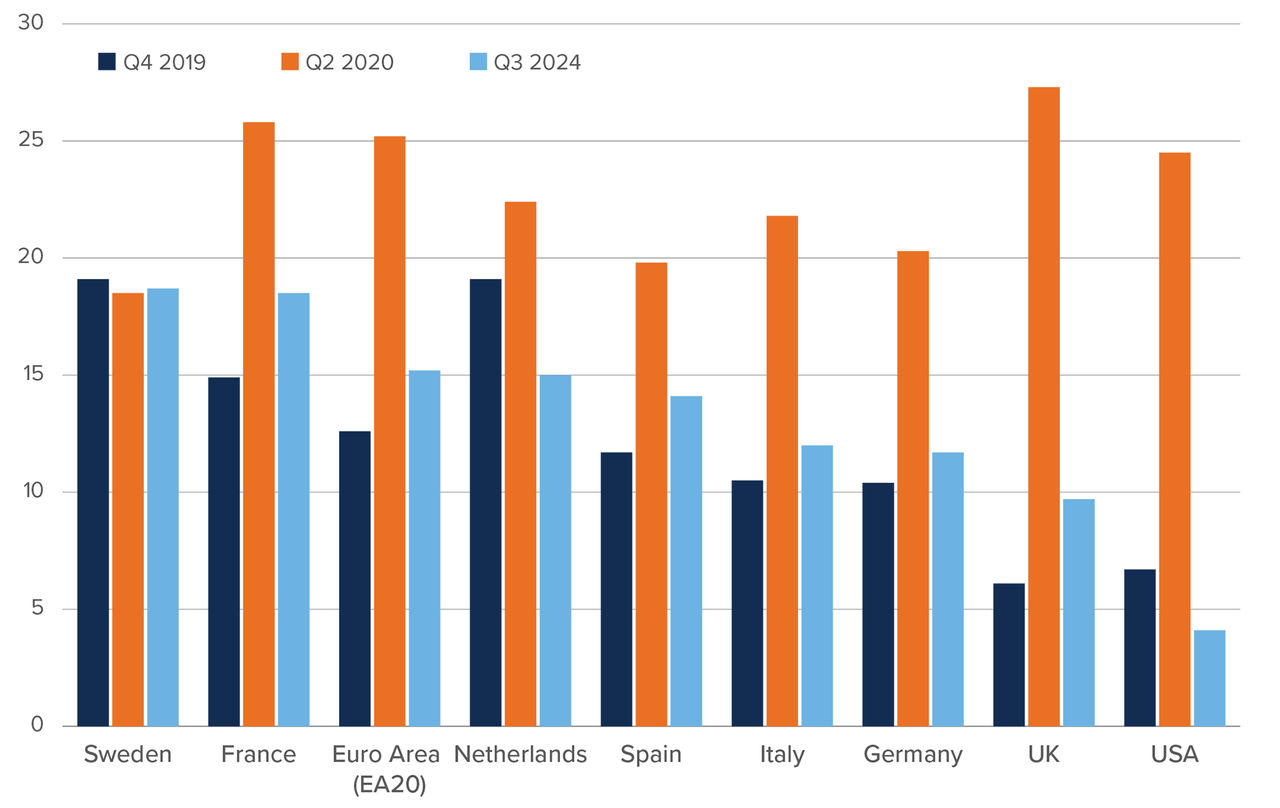

European consumers are on solid footing, with household savings at 15.3% — well above the US rate of 4.9%. This financial buffer enhances resilience and supports discretionary spending recovery.

Household gross savings rate (%)

Source: Eurostat, Haver, Morgan Stanley Economics team Research forecasts

Source: Eurostat, Haver, Morgan Stanley Economics team Research forecasts

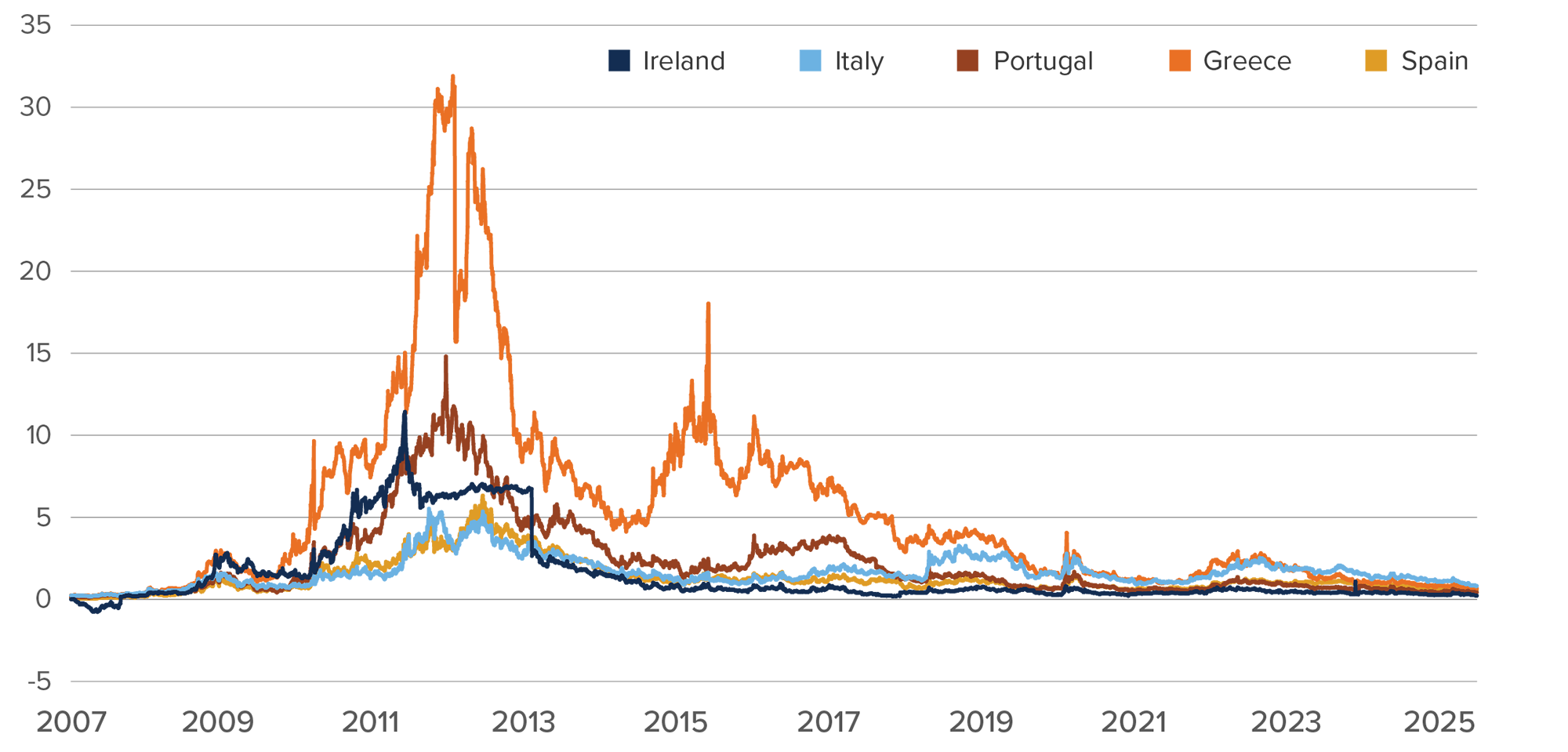

From periphery to pillar

Formerly troubled peripheral economies have staged notable turnarounds. These nations have enacted structural reforms, reduced debt loads and restored fiscal discipline, often outpacing core peers in growth.

Credit rating upgrades and tighter bond spreads reflect these improvements. Unemployment has fallen to multi-decade lows, reducing vulnerability and fueling domestic demand. Once viewed as liabilities, these economies are now investable pillars of European growth.

Periphery 10yr sovereign spread to German bonds (%)

Source: Bloomberg

Source: Bloomberg

European banks: from liability to leadership

Europe’s banks have transformed from post-crisis laggards to capital-efficient performers. Stronger balance sheets and risk controls have doubled capital ratios since 2008. Profitability is improving, with two consecutive years of double-digit ROE. The Euro Stoxx Banks Index is up more than 20% in early 2025, with valuations still modest at 8.4× 2026 earnings.

Banks are returning capital aggressively — with more than 25% of market cap through dividends and buybacks expected from 2024–20261. Industry consolidation and progress toward a banking union offer further upside.

European defence: an emerging structural theme

Europe’s defence sector is undergoing a generational shift. Decades of underinvestment, once mitigated by US security guarantees, must now be reversed. Uncertainty over American commitments — highlighted by voices from the Trump administration at the 2025 Munich Security Conference — has sparked urgency among European policymakers.

- NATO Europe spent €440 billion on defence in 2024 (2% of GDP), compared to 3.4% for the US. At the key June 2025 NATO summit, a target of 5% by 2035 was set, being 3.5% hard military expenditure and 1.5% infrastructure.

- Germany is leading fiscal realignment. Its draft federal budget bill, expected to be passed in September, outlines net borrowing of €850 billion over 5 years.

- German defence spending should, in addition, rise very rapidly.

- The EU’s ReArm Europe initiative proposes €800 billion to support joint procurement and national flexibility.

European defence strategy also emphasizes sovereignty. By 2030, the EU aims to meet 50% of procurement needs with European-made equipment — up from 35%.

This coordinated fiscal, political and industrial pivot positions Europe’s defence sector as a multi-year growth opportunity — no longer just a policy necessity but an investable structural theme.

Conclusion: Europe’s renaissance and the case for global equity allocation

Europe’s story has evolved. What was once viewed as a value trap or diversification filler is now a dynamic investment case, underpinned by strong policy support, narrowing growth and valuation gaps, improving fiscal health and reformed industries.

For investors, international diversification — particularly through an all-cap EAFE strategy with Europe at the core — offers not only balance but the potential for compelling returns. In a shifting global landscape, international equities are not just in the background — they are stepping into the spotlight.

1 Source: Bernstein Autonomous

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing.

Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. The content of this page (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This page may contain forward-looking information which reflect our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of July 29, 2025. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.