The end of US exceptionalism?

For much of the past two decades, US financial markets have benefited from an aura of “American exceptionalism,” underpinned by extraordinary fiscal expansion and ultra-loose monetary policy. The US expanded its federal debt fivefold in 20 years, while the US Federal Reserve (the Fed) deployed trillions of dollars in quantitative easing, measures that no other major economy matched. These policies fueled asset prices and consumption, supporting US outperformance relative to global peers.

Today, the landscape is shifting. Rising debt burdens, tighter monetary conditions and growing political constraints are eroding the foundations that once set the US apart. As the forces behind US exceptionalism wane, investors must reassess their outlook and consider broadening their global exposure. If America’s recent outperformance is increasingly viewed as stimulus-driven rather than structurally entrenched, the risk-reward profile for US equities may be less compelling. This creates a timely opportunity for international markets, particularly, to attract renewed attention and capital.

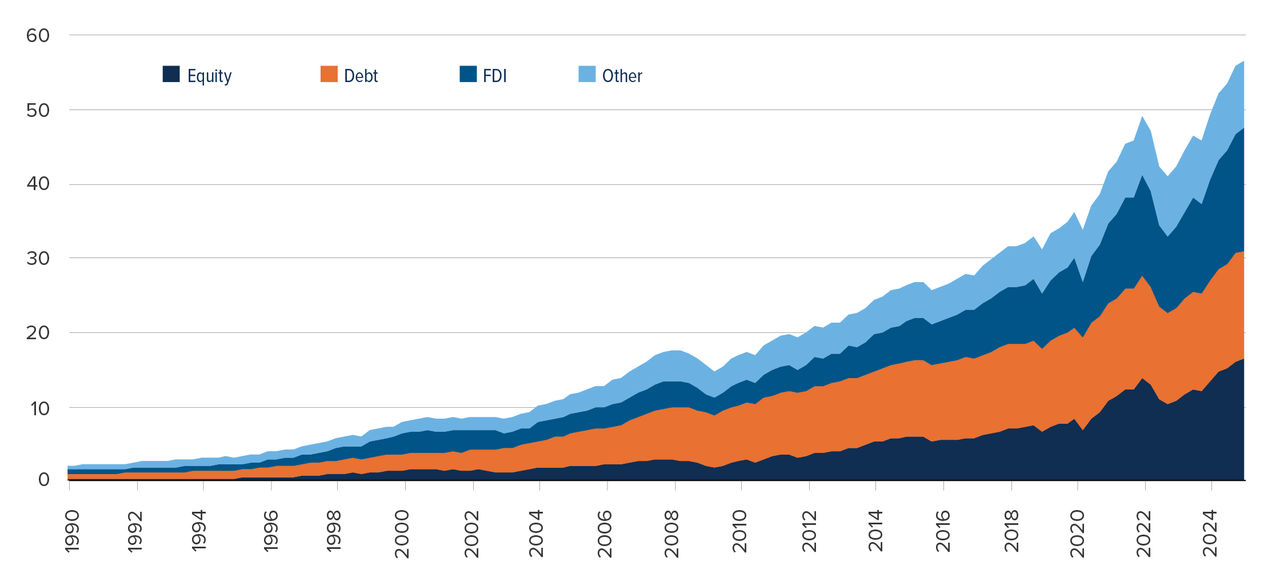

Figure 1: Foreign ownership of US financial assets

USD trillions, Q1/1990 – Q4/2024, quarterly. Financial assets as reported in the US Financial Accounts.

Source: J.P. Morgan, Board of Governors of the Federal Reserve System.

Source: J.P. Morgan, Board of Governors of the Federal Reserve System.

Table 1: Foreign ownership of US financial assets

USD billions. Financial assets as reported at year end in the US Financial Accounts.

Foreign holdings of US assets as of year end ($bn) | |||||

| 1990 | 2000 | 2010 | 2020 | 2024 |

Total | 2,186 | 8,266 | 18,785 | 41,631 | 56,625 |

Equities | 243 | 1,483 | 3,213 | 10,673 | 16,494 |

Debt securities | 709 | 2,335 | 8,252 | 13,254 | 14,461 |

FDI | 540 | 2,783 | 3,422 | 10,761 | 16,546 |

Other | 695 | 1,666 | 3,898 | 6,943 | 9,124 |

Source: J.P. Morgan, Board of Governors of the Federal Reserve System.

Could holding onto US exceptionalism make your portfolio less exceptional?

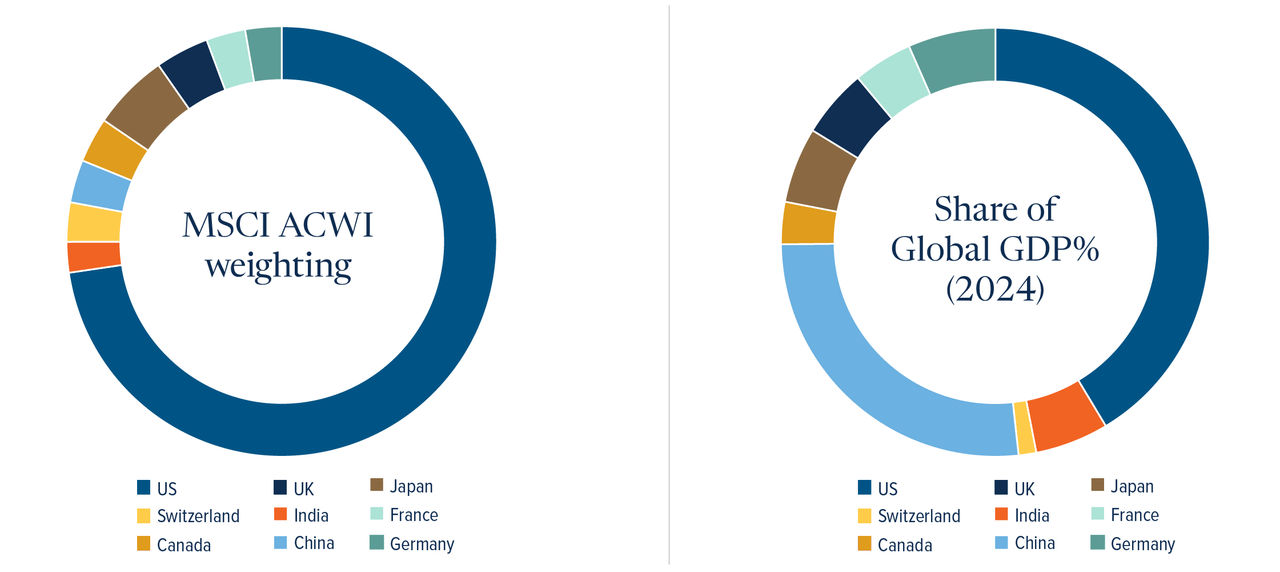

Investing in the US market has served investors exceptionally well for decades. However, that concept of US exceptionalism and the instrumental role it has played in rewarding investors is now being questioned. This is for a good reason: the US accounts for just over a quarter of global GDP yet represents nearly 65% of global stock market value1. Not only does that suggest the US market is significantly overvalued, it also means investors with portfolios heavily exposed to the US are missing out on the wealth of opportunities in international markets, estimated at $52 trillion.2

The message for investors? It's time to look outside the US for investment growth and opportunities.

Figure 2: US weight in global stock indices far exceeds its share of GDP

Sources: Bloomberg, IMF • MSCI All-Country World index, a global stocks benchmark

Sources: Bloomberg, IMF • MSCI All-Country World index, a global stocks benchmark

Four highly compelling reasons to diversify into international markets

1. Enhanced return potential.

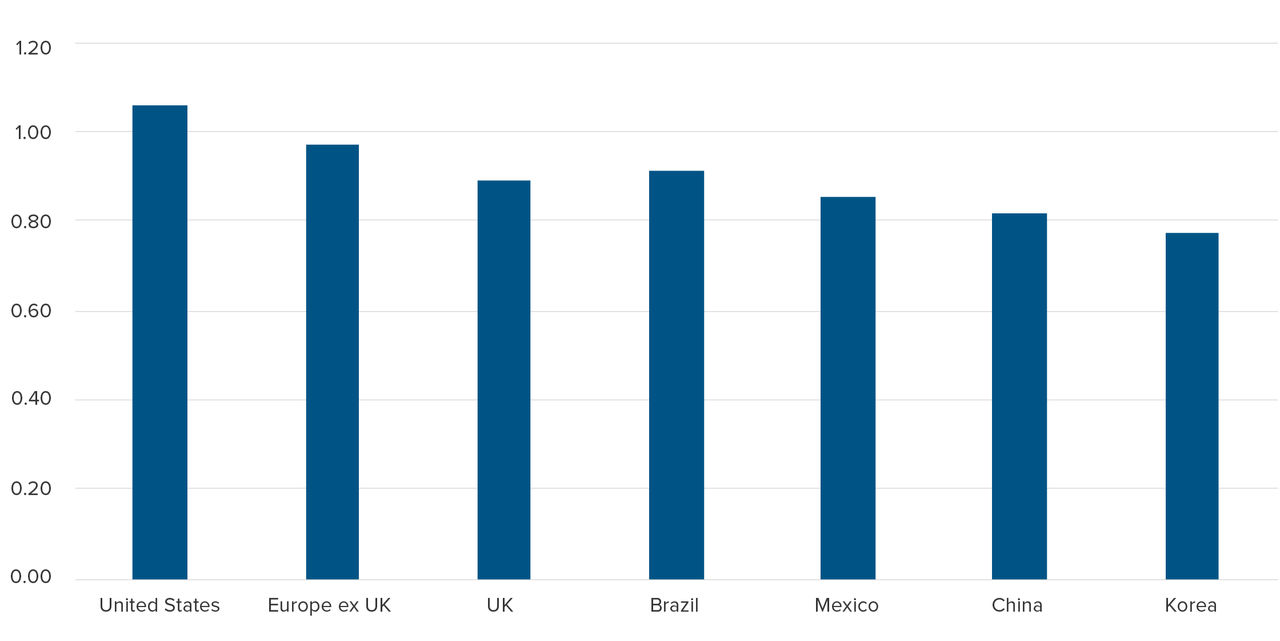

Non-US markets are trading at a discount to their intrinsic value. That’s part of the reason why investment data provider Morningstar predicts low-single-digit returns in the US over the next decade, while other regions are expected to deliver higher — and in some cases much higher — returns.3

Figure 3: Key non-US markets trade at a discount to their intrinsic value

Source: Morningstar, Why Our Best Investment Ideas for 2025 Are Outside the US. Philip Straehl and Michael Field, CFA (Nov 25, 2024).

Source: Morningstar, Why Our Best Investment Ideas for 2025 Are Outside the US. Philip Straehl and Michael Field, CFA (Nov 25, 2024).

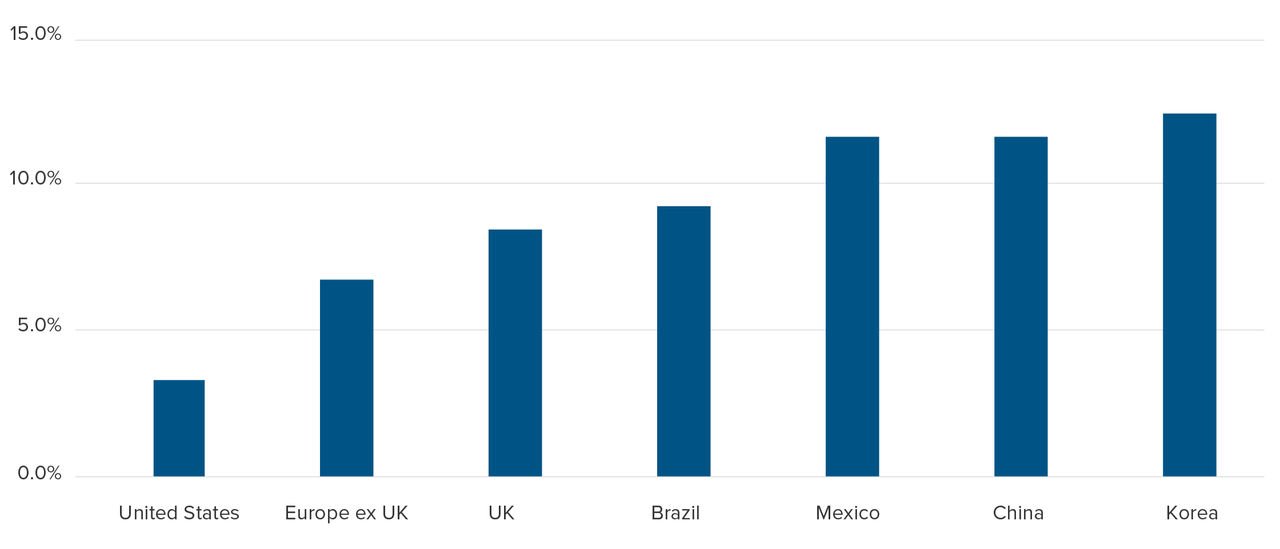

Figure 4: We expect double-digit returns from most attractively valued global markets

Source: Morningstar, Why Our Best Investment Ideas for 2025 Are Outside the US. Philip Straehl and Michael Field, CFA (Nov 25, 2024).

Source: Morningstar, Why Our Best Investment Ideas for 2025 Are Outside the US. Philip Straehl and Michael Field, CFA (Nov 25, 2024).

Read about the factors driving Europe's positive investment outlook from the Mackenzie Europe Team.

2. Good old-fashioned diversification.

Diversification is foundational to reducing risk and increasing investment opportunities. Overexposure to US markets deprives investors of those benefits. International markets account for most of the world's publicly traded companies, spanning not just large economies but also smaller and faster-growing regions. Focusing on the US, where just 10 companies account for about a third of the S&P 500 Index’s value, increases concentration risk and limits investor access to innovative businesses and emerging trends in other markets. 4

And if you think investing in US-based multinationals can deliver the international exposure you need, think again.

Read Mackenzie's study on why exposure solely to US multinationals is not an effective way to diversify or construct efficient portfolios.

3. Emerging investment themes demand a global perspective.

Many emerging investment themes are global in nature: increased spending on defense and national security, digital automation and robotics. This scenario is tailor-made for active managers, where the focus is not on specific geographic markets but rather on companies best positioned to leverage these trends, regardless of location.

4. Gaining appropriate emerging markets exposure.

Emerging markets, such as those in Asia, Latin America and Africa, offer tremendous growth potential, but they’re often underrepresented in the portfolios of most investors. These markets are typically characterized by rapid economic growth, urbanization and industrialization, creating differentiated opportunities for investors to tap into new regions, industries and sectors.

Sources

1 How much exposure to US stocks is too much? Katie Martin, Financial Times, May 2, 2025

2 World Federation of Exchanges database, World Federation of Exchanges (WFE)

3 Why Our Best Investment Ideas for 2025 Are Outside the US, Morningstar, Philip Straehl and Michael Field, CFA, November 2024

4 Ten Stocks Squat On 34% Of The S&P 500's Cash Pile, Matt Krantz, Investors Business Daily, October 2024

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated.

The content of this page (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document may contain forward-looking information which reflect our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events.

Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of July 29, 2025.

There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.