In a market increasingly dominated by large-cap stocks, the case for investing in US small and mid-cap (SMID) equities can easily be underappreciated by many investors. The S&P 500 Index garners a lot of attention from both the media and investors alike, but it has become highly concentrated, with the “Magnificent Seven” tech giants accounting for nearly 30% of the index’s total market cap. This concentration risk has narrowed the opportunity set for investors, making portfolios more vulnerable to the risks of investing solely in a single sector. Therefore, diversifying beyond large caps may be crucial for a resilient investment strategy.

SMID companies offer a compelling solution to the concentration risk inherent in large-cap indices. These companies, typically ranging from approximately $2 billion to $40 billion in market capitalization, are underrepresented in most investor portfolios. By investing in SMID equities, investors can diversify across sectors and business models, often at more attractive valuations than large caps. This diversification can reduce overall portfolio risk and enhance the potential for long-term capital appreciation.

Growth potential

Early-stage growth, innovation and market penetration

Many SMID companies are in the early stages of their product life cycle, which includes the introduction and growth phases. This is when companies may experience rapid revenue growth as they introduce innovative products or services to the market.

In the growth phase, SMID companies are heavily focused on innovation and increasing market penetration. They invest in research and development to enhance their offerings and differentiate themselves from competitors, including larger incumbents in their market. This innovation drives higher growth rates compared to more mature, large-cap companies that may be in the maturity or decline phases of their product life cycle.

Scaling operations and market expansion

As SMID-cap companies move through the growth phase, they scale their operations to meet increasing demand. This scaling often leads to improved economies of scale, higher profit margins and enhanced operational efficiencies. Investors can benefit from this scaling as it translates into stronger financial performance and potential stock price appreciation.

Strategic focus and operational efficiency

SMID companies often benefit from a strategic focus that enables them to dominate niche segments of the market. Unlike large-cap conglomerates with diversified operations and complex internal structures, these firms concentrate their resources on core competencies, driving innovation and execution efficiencies within their specialized domains. This focused approach allows for faster decision-making, stronger customer alignment and the development of sustainable competitive advantages.

Current Macroeconomic Themes

Deglobalization and onshoring

Deglobalization trends and selective deregulation in the US are creating a more favourable operating environment for domestically focused SMID companies. As global supply chains realign and onshoring accelerates, firms with US-centric revenue and localized cost structures stand to gain market share and benefit from greater margin stability. This is particularly important as the US undergoes tariff increases with its trade partners, making domestic suppliers of goods more attractive.

Regulatory rollbacks

Targeted cuts to regulation, particularly in energy, financial services and industrials, may lower the cost of compliance and improve capital deployment flexibility for smaller firms. These structural shifts position US SMID companies to capitalize on domestic investment cycles and policy tailwinds, offering potential for earnings resilience and re-rating opportunities, relative to their global large-cap peers.

Performance and return potential

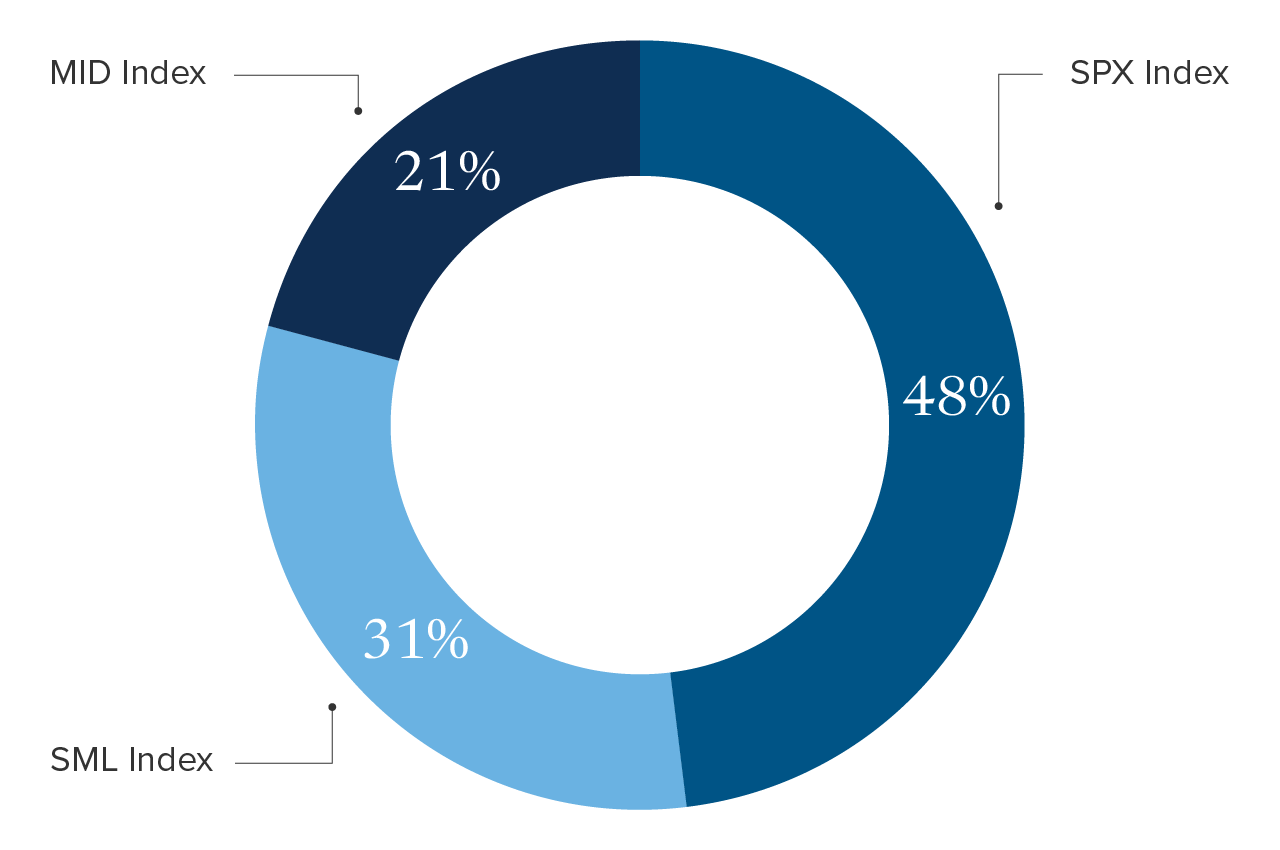

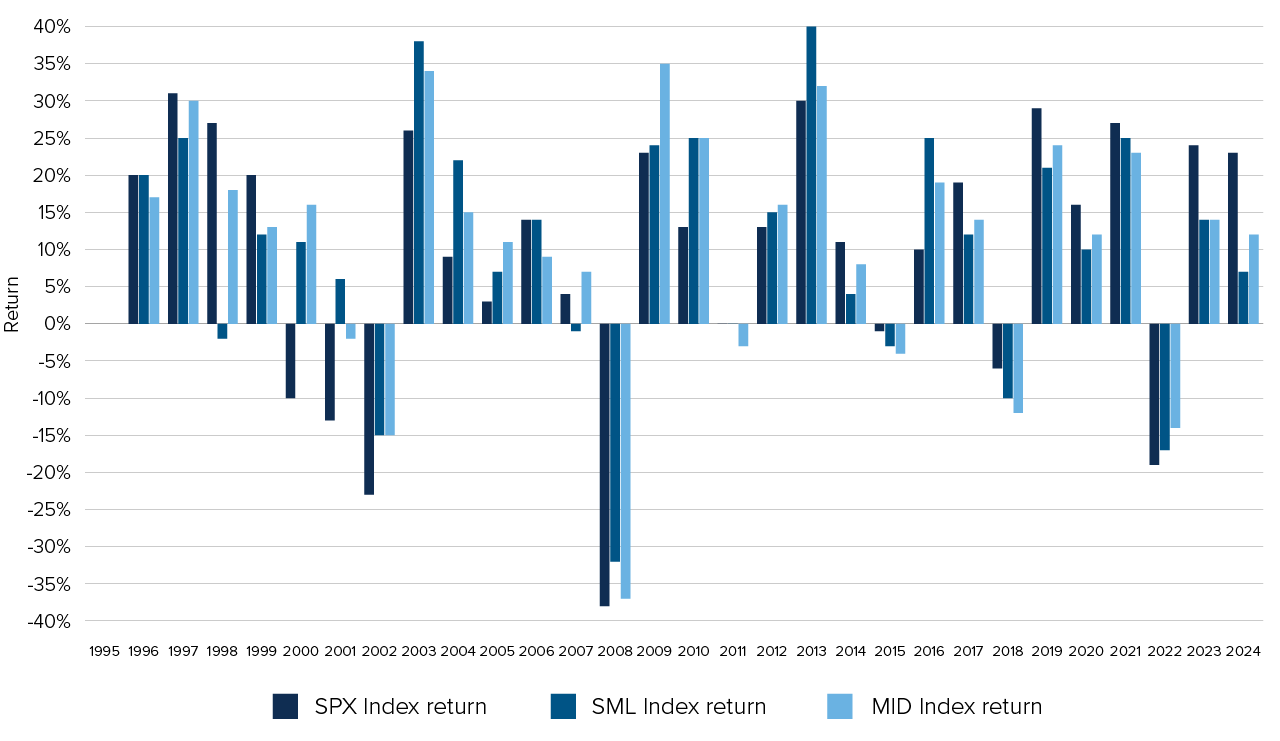

Historical data shows that over the past 30 years, the S&P Small Cap 600 Index (SML) and the S&P Mid Cap 400 Index (MID) have outperformed the S&P 500 Index (SPX) half the time (Figure 1). The performance profiles of these indices highlight the potential for long-term gains from investing in under-covered SMIDs. A skilled active manager in the SMID space can leverage this market cap spectrum to drive returns.

Currently, these companies trade at historically steep discounts relative to their large-cap peers, with a price-to-earnings ratio (P/E) of 18.5x, compared to a 28.0x P/E for large cap stocks. This gap suggests a greater margin of safety and higher return potential.

Figure 1: Each capitalization segment has its day in the sun

Percentage of time each index has led performance (1996-2024):

Source: Bloomberg.

Source: Bloomberg.

Figure 2: Return time series

Source: Bloomberg.

Source: Bloomberg.

Sector representation

The large-cap S&P 500 Index is dominated by the Information Technology (IT) sector, which represents 31% of the index. This dominance also leads to an outsized risk contribution, exposing portfolios to higher sector concentration. In contrast, SMIDs offers broader sector representation, with greater exposure to financials, industrials and consumer services. The concentration in the top 10 holdings in the S&P 500 Index was 34.1%, whereas in the Russell 2500, it only amounted to 15.6%. Clearly, SMID exposure can naturally diversify portfolio risk and reduce reliance on any single company or sector.

Conclusion

In a market increasingly defined by mega-cap dominance, SMID equities play a powerful role in investor portfolios. They can provide diversification away from large-cap concentration and technology dominance. They offer attractive valuations and the potential for multiple expansion, exposure to highly innovative companies, and alpha potential from under-analyzed stocks that are inefficiently priced.

The SMID space is more than a market segment — it’s a source of overlooked growth and innovation within US equities. For investors looking beyond the headlines, the SMID space offers potential for long-term capital appreciation and diversification benefits, making it a compelling investment proposition.

_________________________________

Note: All dollar values are USD.

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns as at December 31, 2024, including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution, or optional charges or income taxes payable by any securityholder that would have reduced returns.

Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. The content of this page (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of June 30, 2025. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.