Understanding private equity: a long-term, transformational asset class

Private equity refers to equity investments in companies that are not listed on public stock exchanges. These companies range from early-stage startups to mature businesses in need of capital for expansion, strategic repositioning or ownership transition.

Compared to public markets, private equity has the potential to offer exposure to less correlated, high-conviction opportunities. Historically, top-performing private equity funds have outpaced public equity benchmarks, in part due to their ability to access inefficient markets and actively drive performance improvements at the portfolio company level.

At its core, private equity involves long-term, hands-on investing with the goal of enhancing the value of a portfolio company over time. Investment strategies vary from venture capital, which supports innovation in sectors like technology or life sciences, to growth equity, which funds scaling businesses, and buyouts, where established firms are acquired and taken private with the intent to improve operations and eventually sell the business at a higher valuation.

Private equity managers actively reshape businesses by bringing in new leadership, streamlining operations, expanding into new markets or divesting from non-core divisions. In many cases, companies are acquired by private equity managers to allow for deeper transformation away from the short-term pressures of quarterly earnings reports.

Funds typically hold stakes in several companies (often between 10 and 30) to diversify risk and balance return potential. Value is ultimately realized through public listings (IPOs), sales to other private buyers (secondary buyouts), or mergers and acquisitions. These exits commonly occur within three to seven years after the initial investment, though hold periods have lengthened in recent cycles.

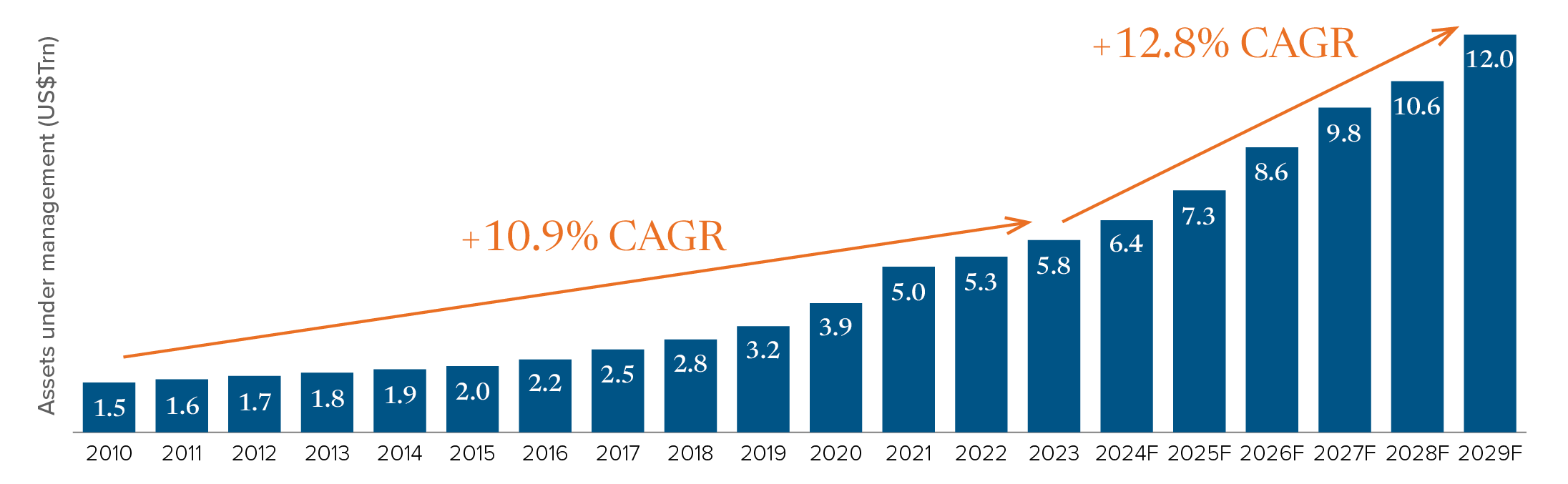

The growth of private equity

Private equity investing has been around since at least the 1960s. Over the past 10 years, growth has accelerated as private equity has gained widespread acceptance as a mainstream asset class. According to data from private markets data firm Preqin, private equity’s growth rate is poised to accelerate further in the years ahead, driven by a broadening investor base, improvements in access to the asset class and increased allocations among investors in response to strong returns and on-going volatility in public equity markets, among other factors.

Growth of private equity AUM (US$Trn)1

Source: 2025 Preqin Global Annual Report, December 2024. Data for 2024-2029 are Preqin’s forecasted figures.

How to access private equity

Traditionally, private equity funds were structured as closed-end vehicles, where investors made capital commitments that were drawn down over time and returned only after the fund exited portfolio companies — usually over a 10- to 12-year horizon. These vehicles were mostly limited to institutional investors such as pension funds and endowments.

More recently, innovation has focused on evergreen and semi-liquid formats such as interval funds, open-ended trust funds and European long-term investment fund (ELTIF) structures, which are designed specifically for high net worth and mass affluent investors.

These innovative structures have effectively mitigated traditional barriers, such as:

- Investors can subscribe with immediate capital investment, removing the uncertainty of capital call schedules.

- Portfolios are already seeded, giving immediate exposure to private assets.

- Periodic (quarterly or semi-annual) redemption windows are available, though often capped to protect long-term investors.

- Some vehicles include liquid securities or use NAV credit lines to enhance flexibility.

Secondaries: a fast-growing liquidity and portfolio-management tool

As private equity matures and fundraising cycles become longer, secondary markets have become a critical mechanism for providing flexibility and managing exposures. The secondary market allows investors to buy or sell existing fund interests (deals led by limited partners) or restructure single assets through continuation vehicles (deals led by general partners). Global secondary transaction volume hit an all-time high of ~$160 billion USD in 2024, with deals led by general partners representing nearly half of that total.

These tools can help accelerate capital deployment, manage vintage diversification and provide early liquidity options. Continuation vehicles alone accounted for ~20% of all private equity exits recently, underscoring their role in today’s market.

Process and phases

Investment

Opportunities are identified and privately negotiated. To finance acquisitions, capital is gradually called into the fund from investors who made commitments during the fundraising period.

Value creation

The value of a private company is increased by organic growth, mergers and acquisitions, operational/profitability improvements, management team additions and, sometimes, restructuring. These initiatives focus on improving the business’ current and future profitability.

Harvesting

The transformed companies are sold, gains are realized and cash is paid out to investors. The typical lifespan of individual private equity investments is between four and seven years.

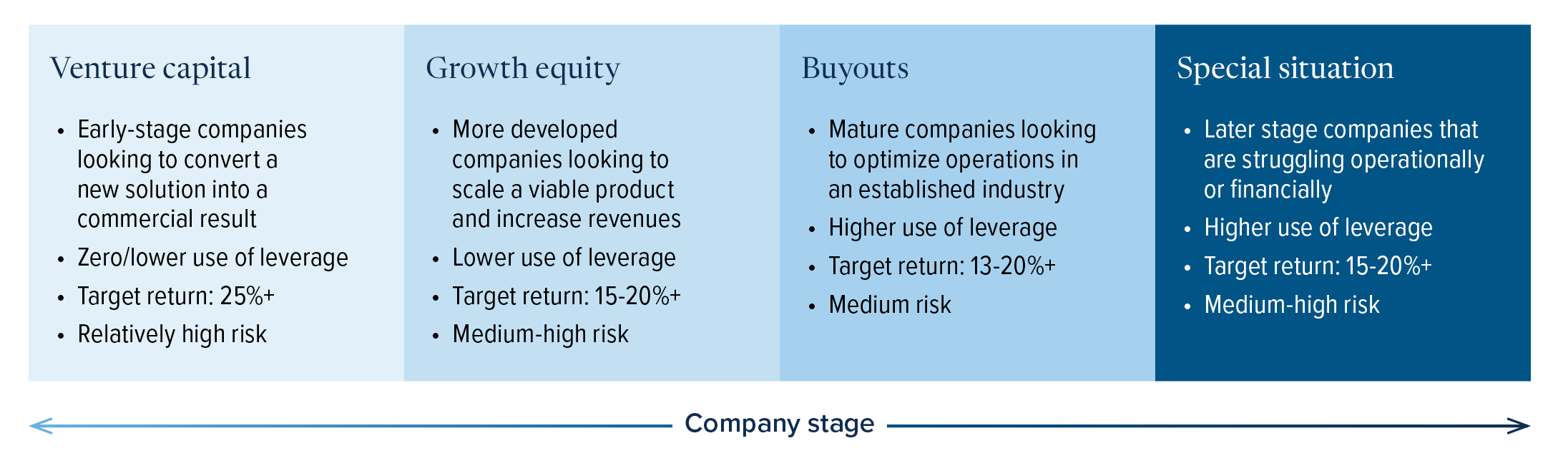

Private equity strategies

There are four broad categories of private equity, each with its own unique risk and return characteristics. Each tends to focus on companies at different stages of their life cycles.

For illustrative purposes only. Target return information is provided for general guidance and should not be relied upon when making investment decisions.

For illustrative purposes only. Target return information is provided for general guidance and should not be relied upon when making investment decisions.

The risks

Whether private or publicly traded, all equity investments involve risk. Economic factors, such as growth and inflation, can affect any business’ performance and valuations.

The private market valuation process generally helps insulate investments from the kind of volatility seen in public equities, but it does not eliminate the general risk that comes with the ownership of businesses in an uncertain economy.

Equity risk

If a private company in a portfolio underperforms, its valuation will likely decline, which will affect investor returns. This risk can be reduced within the fund through diversification across different sectors.

Liquidity risk

Private equity is suitable for investors who have a longer time horizon, as their ability to redeem their funds will be limited. This limited liquidity is generally compensated for by a higher expected return (illiquidity premium).

There are two reasons why limited, structured redemptions are in the best interest of investors:

- Private companies typically take time to mature, as the general partner implements their strategies to improve operations and profitability.

- There is no active secondary market, so it can be difficult and/or expensive for a private equity manager to sell a position to raise cash to fund unexpected redemption requests.

It’s essential to understand that investing in private equity requires the ability to commit capital that the investor does not require for several years. However, patient investors have the potential to reap strong returns generated through private equity.

The future of private equity

As we look beyond 2025, the private equity landscape is undergoing a significant transformation. Previously known as an exclusive institutional playground, it is now maturing into a mainstream portfolio building block. The evergreen and semi-liquid structures now provide investors with instant exposure without the uncertainty of capital calls. Concurrently, the secondary market has evolved into a sophisticated ecosystem, where continuation funds, credit backed by net asset value, and passive secondary vehicles coexist, enabling investors to adjust their exposure or access liquidity without forcing managers into premature exits.

Collectively, broader access, smarter liquidity solutions and data-driven value creation are converging to make private equity more inclusive, more transparent and, for long-term investors, as attractive as it has ever been. For advisors constructing multi-asset portfolios, this transformation translates into a toolkit that offers genuine diversification, calibrated liquidity and access to long-term return potential that was once strictly the domain of large institutions.

Learn more about the Mackenzie Northleaf Global Private Equity Fund >

Units of Mackenzie Northleaf Global Private Equity Fund (the “Fund”) are generally only available to “accredited investors” (as defined in NI 45-106). This material is not intended to constitute an offer of units of the Fund or any other fund referred to herein. Past performance is not necessarily indicative of any future results and there can be no guarantee that the Fund will achieve growth similar to any growth referred to herein. The Fund has material exposure to public market investments, the amount of which will fluctuate over time.

The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it. This article may contain forward-looking information which reflect our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of June 2025. There should be no expectation that such information will in all circumstances be updated, supplemented or revised, whether as a result of new information, changing circumstances, future events or otherwise.