Optimizing bond portfolios with global fixed income

IN THIS ARTICLE min read

In recent history, few periods have presented such a wide range of potential outcomes for fixed income allocations within portfolios. Today, bond allocation requires a more nuanced approach to portfolio construction, as factors beyond the starting yield are increasingly influential in shaping client outcomes. The inflation-uncertainty premium driven by geopolitical tensions and tariff-related disruptions, has contributed to a divergence in global central bank policy stances. Key considerations now include, but are not limited to, active currency management, hedging costs, positioning along the yield and credit curves, and fiscal demand-supply dynamics. While these evolving dynamics introduce greater volatility and complexity, they also create a broader set of opportunities for skilled active managers with global fixed income expertise to generate risk-adjusted alpha.

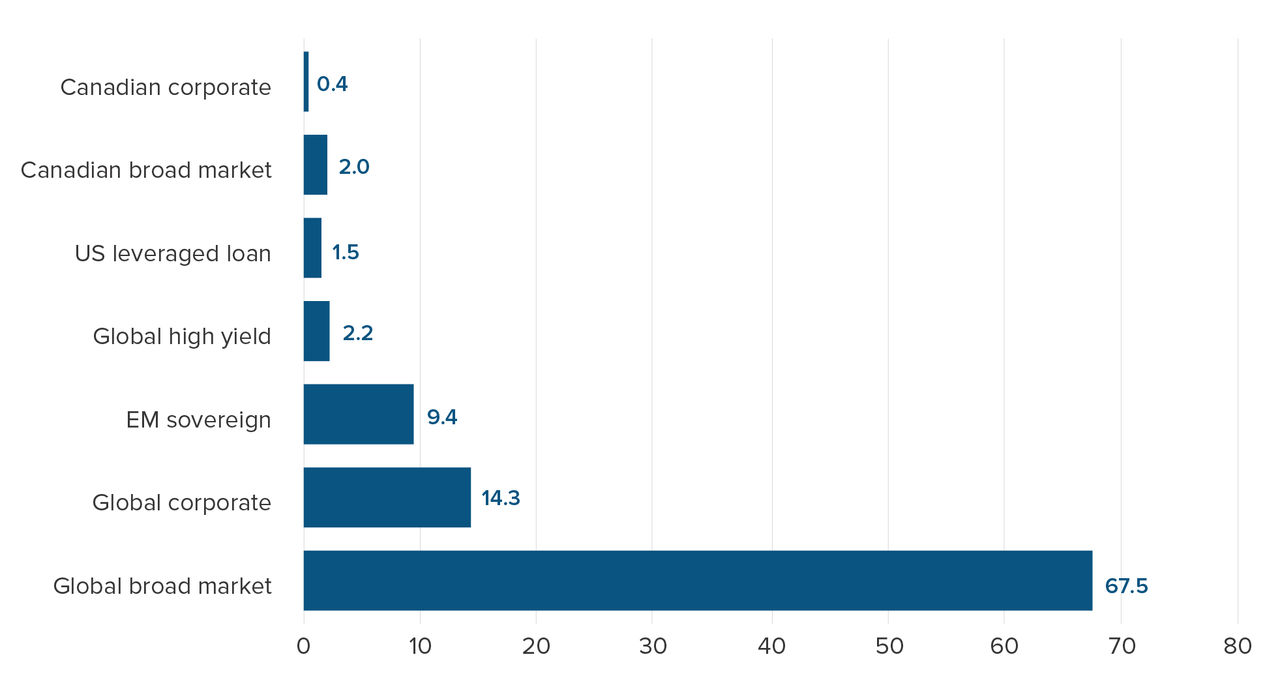

Canada’s fixed income market is a niche player on the global stage, accounting for a fraction of the global bond universe (Figure 1). For Canadian investors in particular global diversification is not just beneficial, it’s essential.

Figure 1: Market cap (USD T)

Source: Bloomberg, Mackenzie Investments as at June 30, 2025.

Source: Bloomberg, Mackenzie Investments as at June 30, 2025.

Global bond divergence: a source of alpha

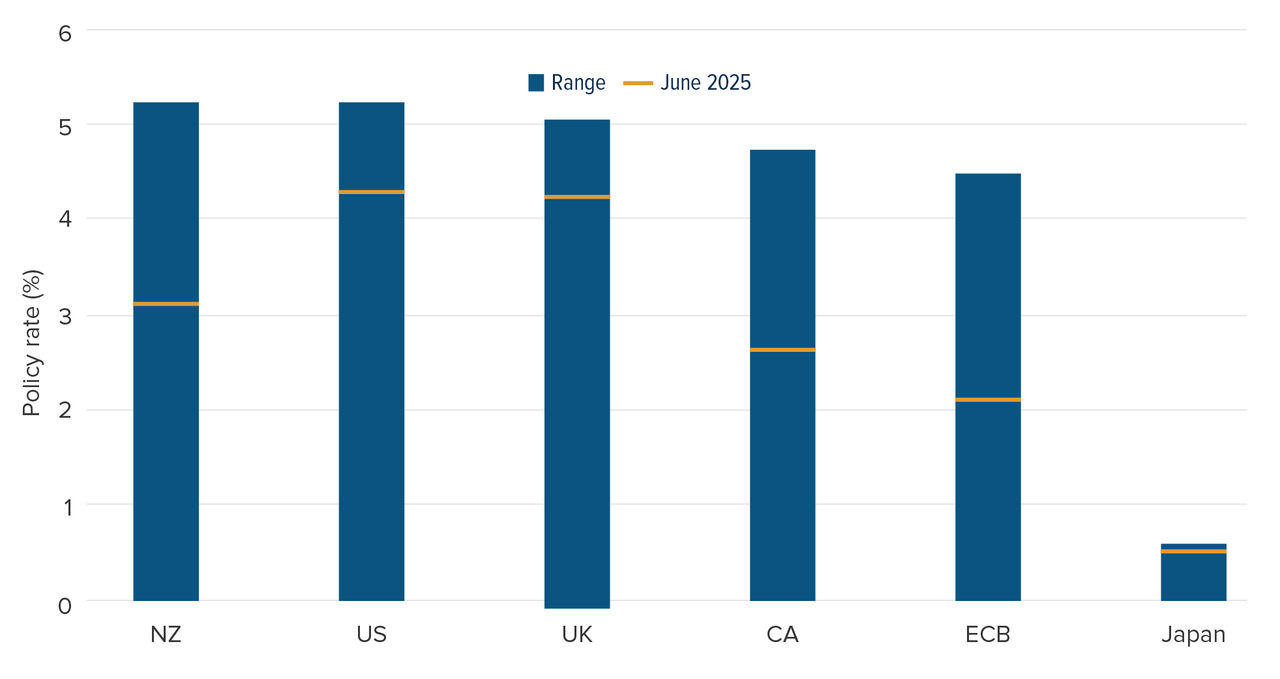

Since 2020, we have experienced three distinct cycles driven by inflation dynamics and monetary policy responses. Most G10 countries embraced fiscal expansion during and after COVID, despite being in recessionary environments. This resulted in a positive fiscal impulse, as governments increased spending and/or reduced taxes to support economic activity. From synchronized easing during the pandemic to aggressive tightening in 2022, and now, a phase of policy divergence, central banks are no longer moving in lockstep (Figure 2). The US Federal Reserve, for instance, faces tariff-driven inflation risks, while the Bank of Canada contends with sluggish growth further deteriorated by tariff uncertainty. This divergence presents both opportunities and risks. For Canadian investors, the relative richness of domestic bonds versus global peers may limit return potential but also signals a more unstable macro backdrop. Active managers can exploit these dislocations through cross-market relative value trades, while remaining mindful of currency risk and policy inflection points (Figure 3).

Figure 2: Global policy rate - 2020 to present

Source: Bloomberg, Mackenzie Investments as at June 30, 2025.

Source: Bloomberg, Mackenzie Investments as at June 30, 2025.

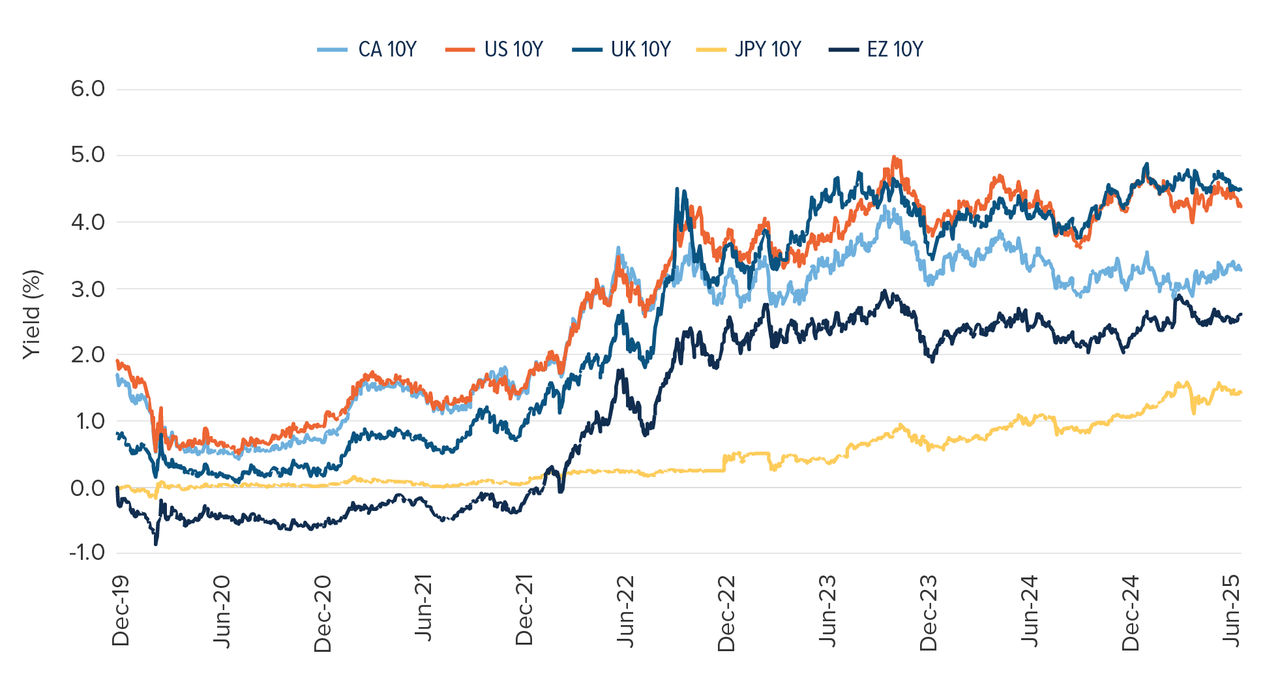

Figure 3: Global government bond yields

Source: Bloomberg, Mackenzie Investments as at June 30, 2025.

Source: Bloomberg, Mackenzie Investments as at June 30, 2025.

From a policy perspective, Fed Chair Powell has highlighted the risk of tariff-driven inflation, but if this fails to materialize in the data, the Fed may find itself behind the curve. In this context, we maintain a constructive stance on US duration as we believe the curve could respond to a dovish pivot. Importantly, we see limited near-term risk of fiscal policy disruption in the US. Turning to Canada, we expect domestic duration to underperform US duration in the second half of the year. This view is informed not only by diverging central bank paths but also by fiscal dynamics. Both federal and provincial issuance are set to increase meaningfully and is likely to place upward pressure on Canadian bond yields. As such, we remain cautious on Canadian duration, relative to the US.

New Zealand interest rates remain relatively high compared to other developed economies. As global interest rates fell, New Zealand bond yields saw the most significant spread tightening versus US, from 100 bps in 2021 to -20 bps in December 2024, while also benefitting from the country’s higher initial yields. Inflation, currently at 2.7%, has also been trending steadily downward and is now within the central bank’s target range of 1% to 3%. In response to evolving economic data and emerging opportunities, the team realized profits by exiting its exposure to New Zealand.

The euro zone has its own challenges, which supports our neutral view. European governments are ramping up fiscal commitments, particularly in defense spending. This surge in spending, while politically driven, risks widening deficits — especially in high-debt nations like Italy, Spain and France. Germany’s recent suspension of its “debt brake” has signaled a broader shift away from austerity. This policy pivot has increased issuance expectations, adding upward pressure on yields.

In the past we have long held a short Japanese Government Bond position across our funds as a medium-term macro trade based on the idea that Japan was “not an island” and the Bank of Japan’s yield curve control policy was keeping JGB yields artificially low. This was predicated in part on the notion that Japanese domestic inflation would be like global inflation, not only in direction, but also stickiness, and the BoJ was underestimating how quickly domestic inflation would rise.

Currency: a strategic lever in global fixed income

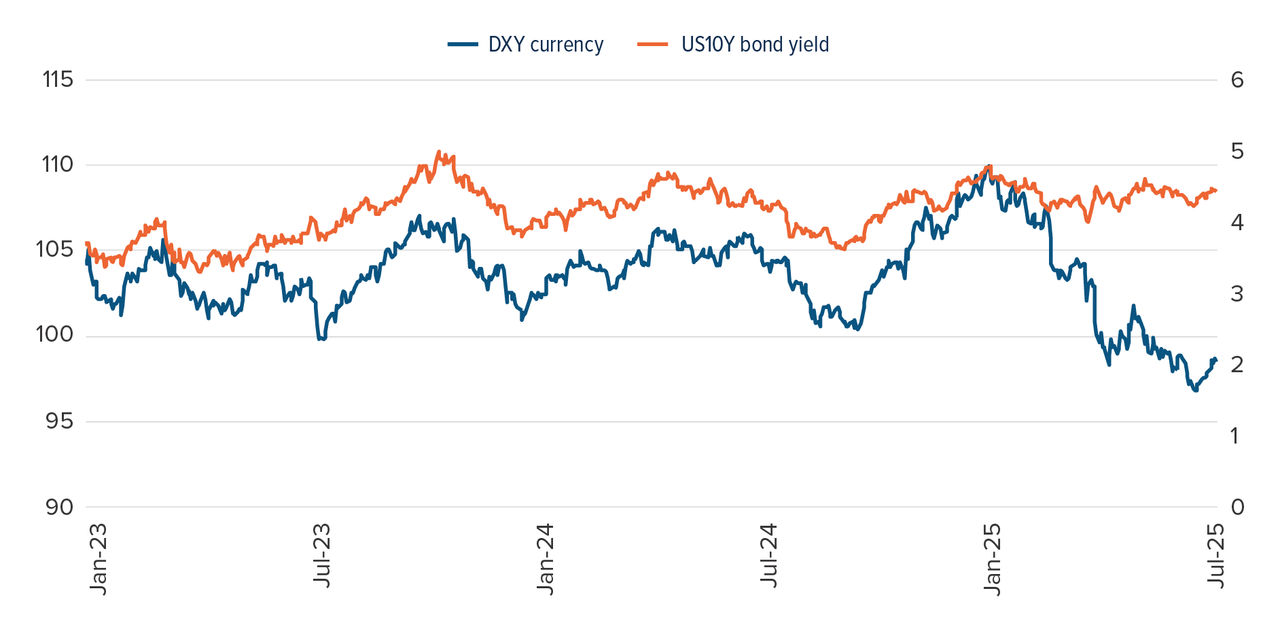

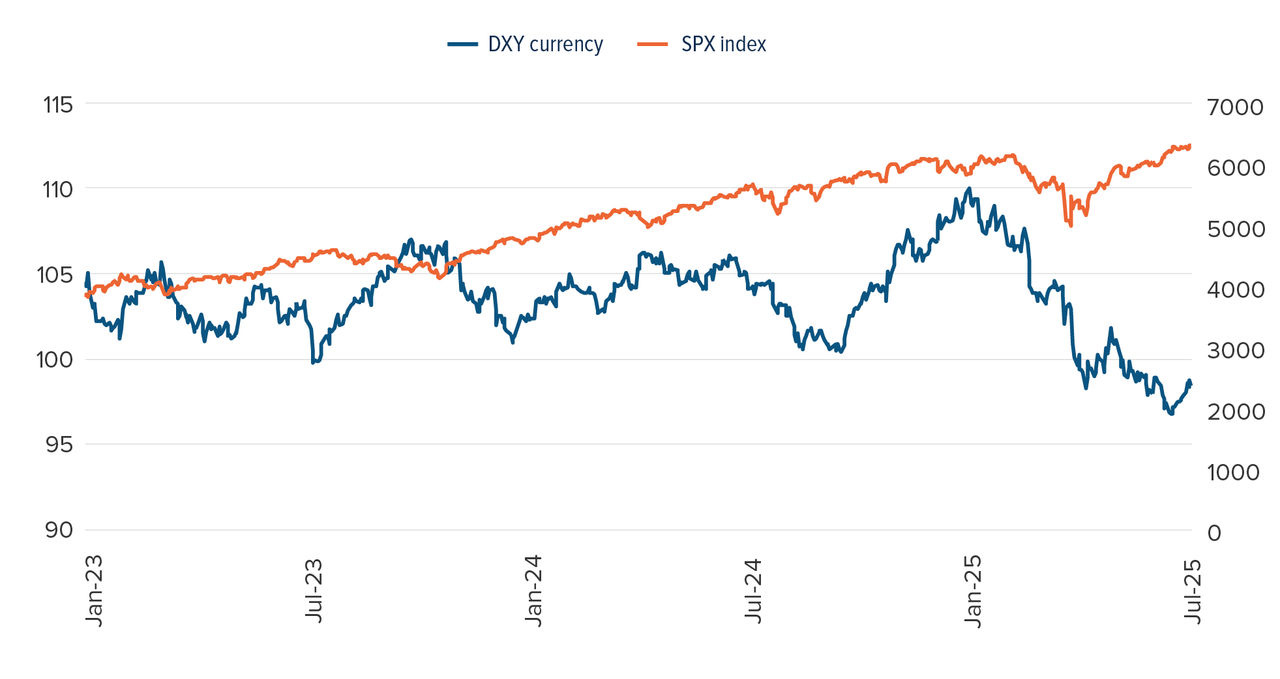

The US dollar has posted its weakest performance in over five decades in the first half of 2025, reflecting a confluence of policy uncertainty and unwinding of the US exceptionalism trade. The recent breakdown in correlation between the US dollar, US Treasuries and equities marks a significant departure from historical norms (Figure 4). Traditionally, the dollar has exhibited a negative correlation with risk assets like the

S&P 500 and a positive correlation with Treasuries, reflecting its dual role as both a safe-haven and a proxy for US monetary policy. However, in 2025, all three asset classes have come under pressure simultaneously, a rare and telling phenomenon.

Figure 4: Dollar correlation vs treasuries and equities

Source: Bloomberg, Mackenzie Investments as at June 30, 2025.

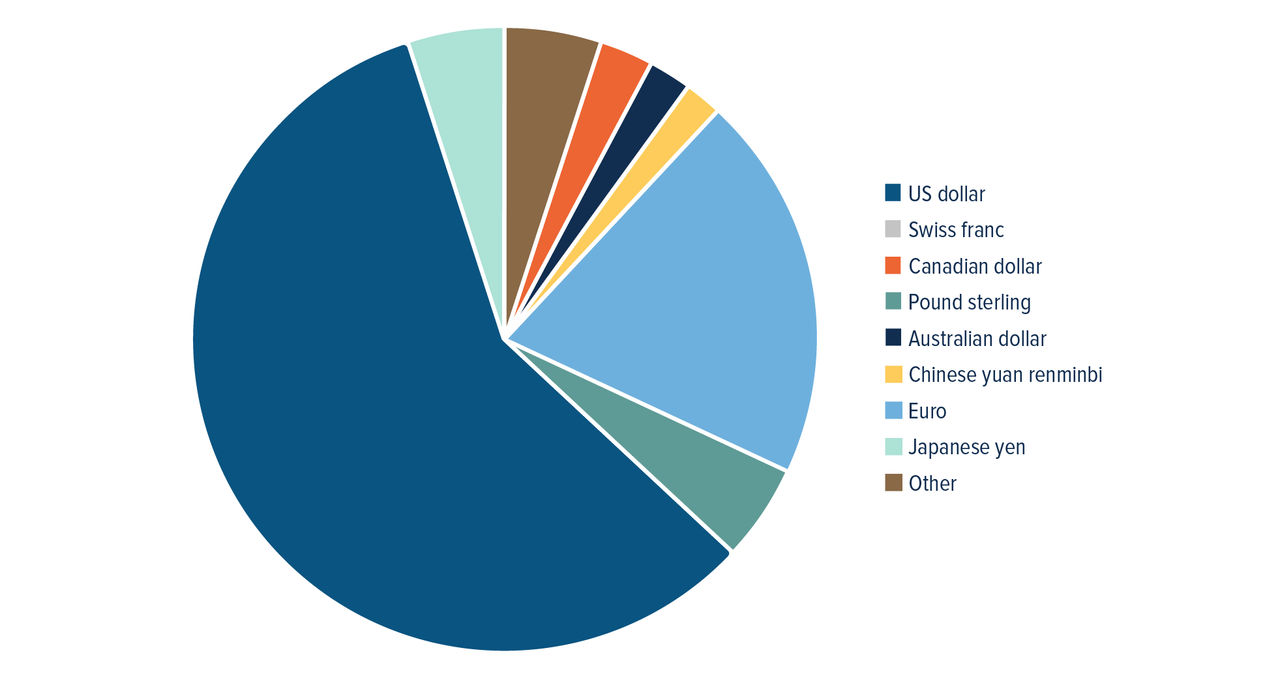

Noteworthy to highlight: we believe the US dollar is likely to retain its status as the world’s primary reserve currency for the near future. This resilience stems from the unparalleled depth and liquidity of US Treasury markets, the dominance of the dollar in global trade and the institutional strength of the US financial system. While fiscal imbalances and geopolitical tensions have raised legitimate concerns, no viable alternative currently matches the dollar’s scale, convertibility and legal protections. While the dollar’s current share of international reserves is the lowest it has been in decades, its 58% tally is still well above the euro’s 20% share (Figure 5).1

As global investors rebalance and reassess their hedging strategies, we are seeing increased volatility and dispersion in FX markets which is an important consideration for fixed income managers with global mandates. For fixed income investors, FX exposure management is becoming an increasingly strategic lever — both for risk mitigation and for alpha generation.

Figure 5: Currency composition of global foreign exchange reserve

Source: Bloomberg, Mackenzie Investments as at June 30, 2025.

Source: Bloomberg, Mackenzie Investments as at June 30, 2025.

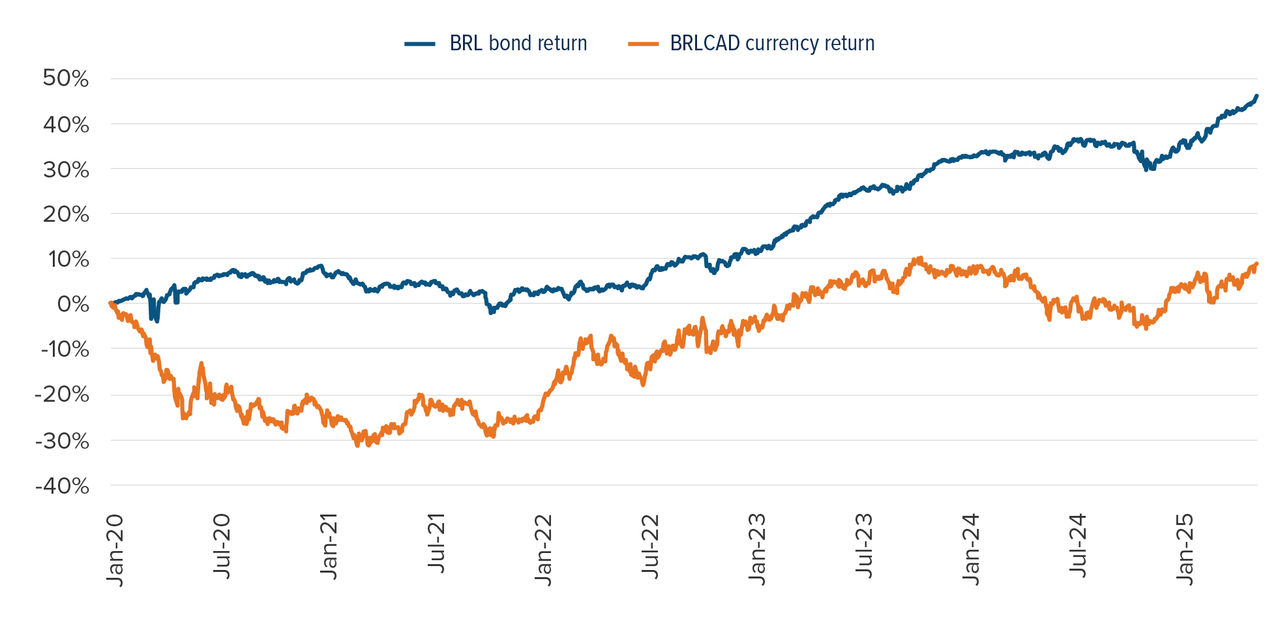

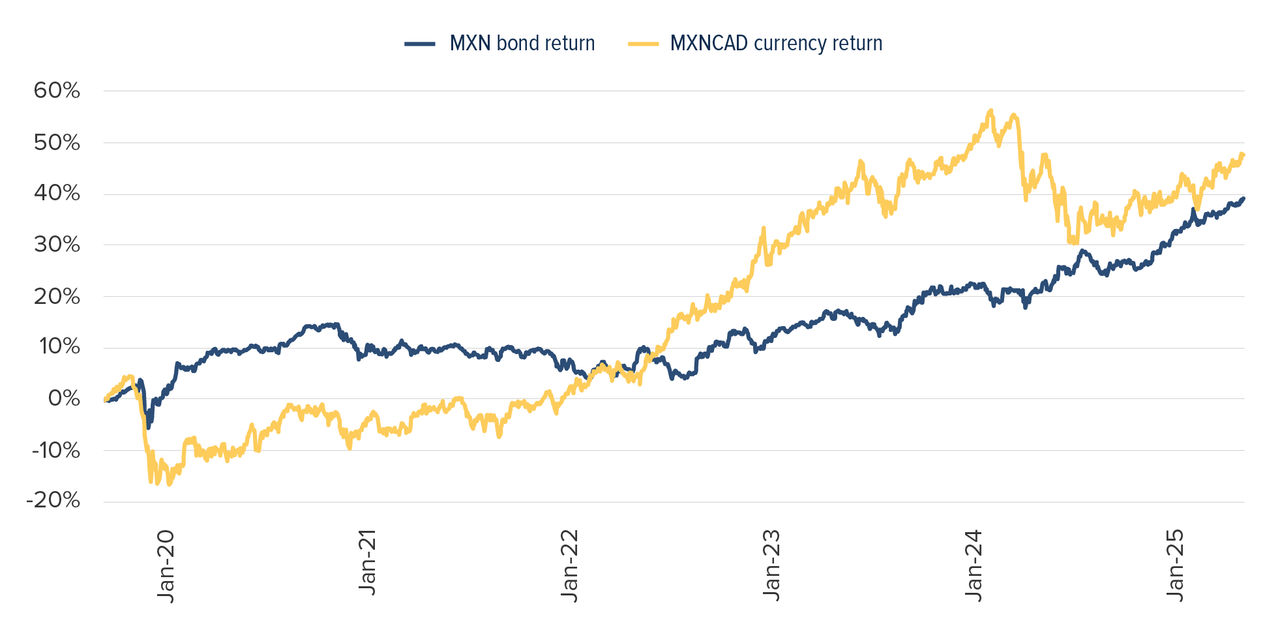

As we enter the second half of 2025, the case for allocating to emerging market (EM) bonds has rarely been stronger. With global disinflation gaining traction, the US dollar weakening, and some EM central banks ahead of the curve, investors are being rewarded with high real yields, currency tailwinds and improving macro fundamentals. One of the most compelling reasons to own EM local debt today is the real yield differential. Countries like Brazil and Mexico are offering real yields north of 5%-8%, a stark contrast to developed markets where inflation-adjusted returns remain subdued (Figure 6). These levels are not only attractive in absolute terms but also provide a significant cushion against volatility and inflation surprises. The US dollar decline has been a key driver of performance for EM local currency bonds. The Brazilian real and Mexican peso have both appreciated, enhancing unhedged returns for global investors. Moreover, hedge ratios have improved, making it more cost-effective for USD-based investors to manage currency risk while still capturing the yield advantage. EM bonds’ ability to have idiosyncratic drivers, high carry and higher yields compared to developed market, make them a powerful diversifier. With US rates stabilizing and global inflation moderating, there is room for spread compression, highlighting the alpha potential in EM debt. As always, selectivity is key. We continue to favour Latin America, particularly Brazil and Mexico where policy credibility, real yields and macro stability are aligned in investor’s favour.

Figure 6: Emerging markets - resilience amid trade wars

Source: Bloomberg, Mackenzie Investments as at June 30, 2025.

The new global order: politics over economics

Global politics are increasingly shaping the economic landscape, and 2025 has brought this into sharper focus. With the US shifting toward more inward-looking policies under its new administration, we are seeing a rise in trade barriers and a more confrontational approach to international relations. This is not entirely new, as protectionist trends have been building for years, but what is different now is the scale and intensity. Recent US actions, including sharp tariff hikes and broader trade restrictions, have reignited a full-blown trade war. Tariffs are rising, trade tensions are escalating, and global supply chains are being restructured based on political alliances rather than economic logic. For investors, this means higher costs for goods and services, as global trade becomes less efficient, slower growth in both developed and emerging markets, reduced productivity and innovation, and greater uncertainty, which can lead to more volatility in bond markets.

Diverging policy paths, shifting economic data and geopolitical uncertainty have made this a more complex environment for investors. For fixed income investors, this means staying nimble. Understanding where we are in the cycle and how policy decisions ripple through markets will be key to navigating what comes next.

As fixed income investors, it is important to stay focused on quality, diversification and flexibility. These geopolitical shifts may create headwinds, but they also open opportunities for active managers who can navigate the evolving landscape.

Mackenzie global solutions that adapt: tailored for Canadians

The unique and diversified opportunities within the global fixed income landscape are actively captured across our suite of strategies, including:

- Mackenzie Global Core Plus Bond Fund

- Mackenzie Unconstrained Fixed Income Fund

- Mackenzie Global Corporate Fixed Income Fund

- Mackenzie Global High Yield Fixed Income ETF

We actively harness unique opportunities created by policy divergence, FX volatility and credit dislocations. Our process integrates dynamic currency management, curve positioning and credit selection to deliver enhanced risk-adjusted returns for CAD-based investors.

1 Source: IMF as of Q1 2025.

Commissions, trailing commissions, management fees, brokerage fees and expenses all may be associated with mutual fund investments and Exchange Traded Funds. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns as of June 30, 2025 including changes in share or unit value and reinvestment of all dividends or distributions and does not take into account sales, redemption, distribution, or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds and Exchange Traded Funds are not guaranteed, their values change frequently and past performance may not be repeated.

The content of this document (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of August 30, 2025. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.