Unconventional investing: Mackenzie Ivy’s long-term focus

IN THIS ARTICLE

Trade wars, geopolitical turmoil, daily US policy announcements, Liberation Day, election day — all can leave markets skittish, with investors on a roller coaster of highs and lows: the epitome of volatility.

The Mackenzie Ivy Team understands how anxious volatile markets can make investors. Alleviating that anxiety and delivering steady long-term returns is core to the Ivy investment approach, as it has been for over 30 years.

While some managers measure success solely on beating the index and their peers, the Ivy Team also emphasizes helping investors achieve their goals. That means not only aiming to achieve solid returns but also seeking to prevent investors from engaging in counterproductive investment behaviours, like selling in downturns and buying at market peaks. This reinforcement of good investment practices is a logical extension of how the team carefully builds and manages its portfolios, particularly when markets get choppy.

When other managers run for cover, Ivy steps in

It is during volatile times that the Ivy Team’s approach can run against the convention of some other managers, who may run for cover by moving into defense at the expense of offense.

Guided by a deep knowledge of companies identified as attractive long-term investments and coupled with a philosophy of building concentrated portfolios, the Ivy Team is poised and ready to act when the price of a desired company falls amid volatility. During the recent volatile environment, the team has sought to do just that, adding quality companies with impressive economics — successful businesses that know their edge and that the team believes can consistently leverage that edge under a variety of economic conditions.

Those perceived qualities — strong economics and a defined, well-understood market advantage — are the hallmarks of the Ivy approach to buying world class businesses with enduring value. The team is confident that adding those types of companies when prices fall on sagging market sentiment will, over the long term, likely add value for investors in Ivy funds.

Careful and cautious but able to strike quickly

This process highlights a key feature of the Ivy approach: the team’s tactical flexibility. Although a common perception is that Ivy is careful and cautious — the team’s long and thorough research process can provide a strong investment edge that can be leveraged when the opportunity arises. In those cases, there is no need to scramble to research that company on the fly — that work is done well ahead of time.

That’s the essence of the Ivy difference in volatile times: when others are back-pedaling, the Ivy Team is squarely on its front foot ready to deploy capital for the long-term benefit of investors.

This is Ivy’s time to shine

In many ways this is Ivy’s time to shine. Being careful when the market is buoyant means that the Ivy Team is prepared to take advantage of opportunities when volatility strikes. The wisdom of the approach is evident in the numbers: over three years, Mackenzie Ivy Foreign Equity Fund has delivered positive returns 99% of the time; and over seven- and 10-year periods, that number is 100%, far better than the 10-year index figure of 85%.

Source: Morningstar Direct, as at June 30, 2026.

Ten years can be a long time in market cycles, with multiple downturns and periods of volatility. That’s exactly the timeframe Ivy uses when assessing a company’s ability to deliver the kind of steady earnings required to generate consistent fund returns for investors. It’s also the time period investors should consider in the midst of volatility like we’re experiencing today. Because during those 10 years, that kind of volatility may very likely happen again.

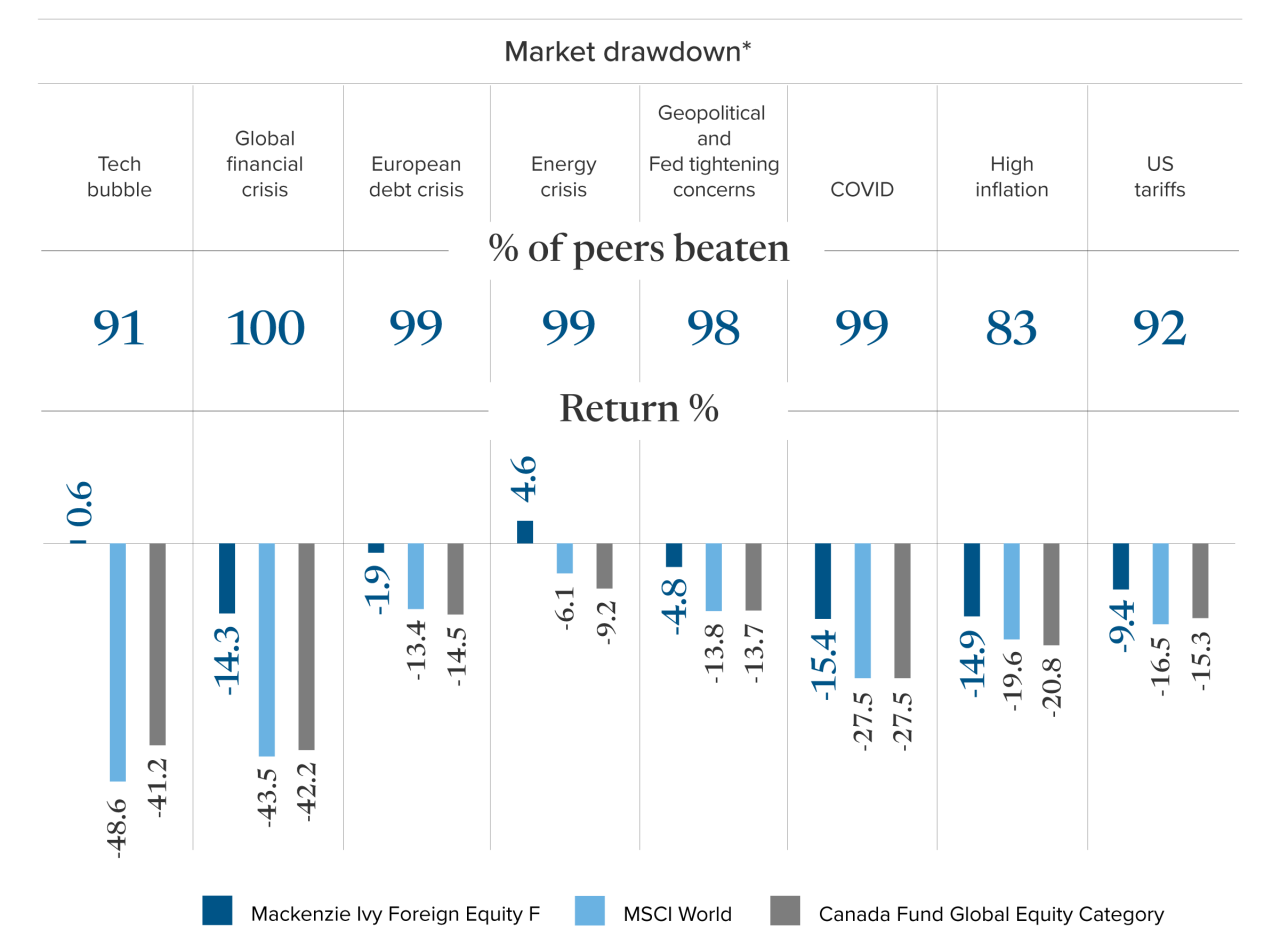

Mackenzie Ivy Foreign Equity Fund – Top quartile in every drawdown

The MSCI World returns in this chart are displayed in Canadian dollars to ensure comparability with the Mackenzie Ivy Foreign Equity Fund and other Canadian-domiciled global equity peers. Index performance does not include the impact of fees, commissions, and expenses that would be payable by investors in the investment products that seek to track an index.

The question then that investors should be asking themselves isn’t, “where do I hide in volatile markets?” Instead, they should view volatility the way Ivy does and ask, “is this an opportunity to add long-term value?”

Meet the team

* Tech bubble - 04/27/2000 – 03/12/2003, global financial crisis - 10/14/2007 – 03/09/2009, European debt crisis - 05/02/2011 – 10/04/2011, energy crisis – 05/21/2015 – 02/11/2016, geopolitical and fed tightening concerns – 09/23/2018 – 12/25/2018, COVID – 02/19/2020 – 03/23/2020, high inflation 01/04/2022 – 09/30/2022, US tariffs 02/18/2025 – 04/08/2025.

Commissions, trailing commissions, management fees, and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. The indicated rates of return are the historical annual compounded total returns as at June 30, 2026, including changes in unit value and reinvestment of all distributions and do not take into account sales, redemption, distribution, or optional charges or income taxes payable by any securityholder that would have reduced returns.

Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. The content of this page (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of June 30, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.

©2026 Morningstar. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.