ETFs’ popularity continues to grow among Canadian investors: a record-breaking $53 billion was invested in ETFs in Canada in 2021.1 As a result, many investors are now aware of the advantages that ETFs bring, such as:

- Low-cost diversification

- Easy availability of previously inaccessible markets

- Daily liquidity and transparency

In our recent blog, “What are ETFs and why should I care?” we covered a range of ETF basics, including how ETFs work and the different strategies they use. For this blog, however, we wanted to dig deeper and answer some of the more complex ETF questions found on investing forums such as Reddit.

In this first part of a two-part series, we delve into questions that are rarely answered by ETF providers.

How are expenses charged on an ETF?

ETF providers don’t take money from your brokerage account to collect fees. Instead, management fees are reflected in the end of day net asset value (NAV) of the ETF. Management fees are reflected in the performance of the ETF, so you might expect an index ETF to underperform its benchmark by the annual management fee charged. However, other factors, such as the trading expense ratio, securities lending and sampling at the fund level can lead to greater or lesser performance differences beyond the fees charged.

Is there anything other than management fees to consider in terms of cost?

Some of the costs embedded in ETFs include the management expense ratio (MER), portfolio turnover expenses, capital gains/losses and withholding taxes. The management fee and other operating expenses, such as audit or legal fees, as well as sales taxes, where applicable, are all included in the MER, which is readily available on issuers’ websites. These costs will vary between ETFs depending on numerous factors including whether the ETF is an active or index strategy, the asset class, structure of the ETF etc.

There are also trading expenses, which include commissions, the spread between the bid and ask price, and NAV premiums/discounts (considered indirect costs). Mutual funds also have trading expenses, but they are embedded within the fund itself, as the portfolio manager buys and sells securities to deal with investor cash flows. In contrast, ETF trading costs are transparent, and ETF investors generally pay them when they buy or sell the fund.

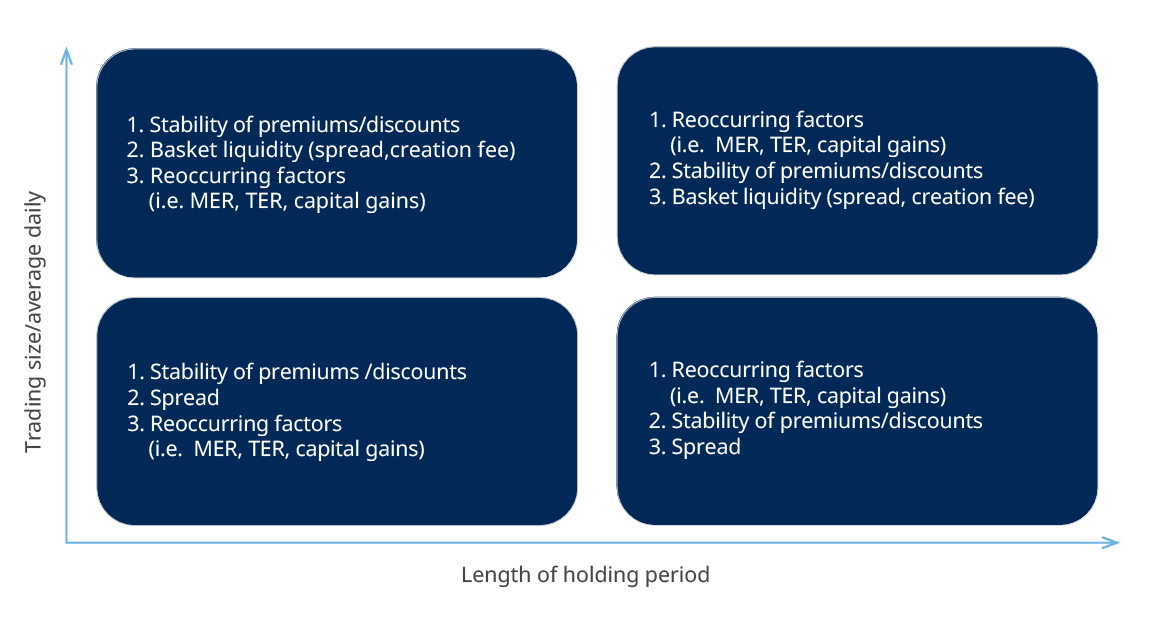

How to weigh up the different cost considerations

These considerations will mostly depend on how long you intend to hold the ETF and how much of it you intend to buy. The longer you hold an ETF, the more the spread cost and commission expenses will decrease as a portion of the total cost of ETF ownership. These transaction costs only happen when you buy or sell an ETF, so these considerations are more of an issue for short-term tactical traders.

Long-term investors should prioritize recurring costs (such as management fees), how the structure of the ETF may influence withholding taxes and portfolio turnover expenses.

When comparing similar ETFs, this chart can be helpful:

How do ETF prices work?

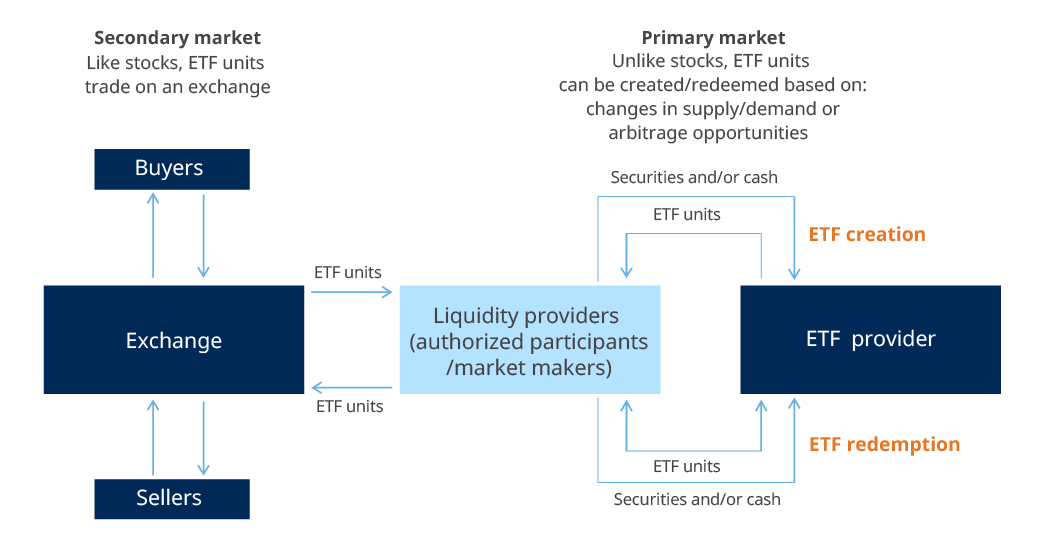

ETFs trade on an exchange, in much the same way as a stock does. However, a key difference is that an ETF has an additional level of liquidity, due to what is called the creation and redemption mechanism. This mechanism helps to ensure the ETF price (which changes every second, as it’s bought and sold on an exchange) stays close to the actual value of all the securities that are held within it (the NAV).

If lots of people buy an ETF, will its price become inflated above the index value?

The creation/redemption mechanism mentioned above is used by market makers to keep the ETF trading at or near fair value, and so its role is to prevent the ETF price from becoming inflated.

If the ETF price did rise substantially above its fair value, market makers could add new ETF shares into circulation to bring its price back in line with the underlying NAV. Conversely, if the ETF were to trade at a discount to its NAV (at a price below it’s fair value), then the mechanism would work in reverse. Market makers would take ETF shares out of circulation via the primary market and exchange those shares with the ETF provider for the underlying securities. These transactions are often made in-kind, and in these cases no buying or selling of the underlying securities would take place at the portfolio level.

The secondary market and primary market, where market makers create and redeem shares at the NAV, help increase overall pricing efficiency and also enhance liquidity.

How are index ETFs tax efficient?

Firstly, ETFs that aim to closely track the performance of an underlying index would typically have less turnover than other funds, such as an actively managed mutual fund. Lower turnover (the buying and selling of securities) leads to less capital gains distributions and therefore fewer tax implications.

Secondly, ETFs are listed on exchanges. This means investors can buy and sell ETF shares without causing turnover in the underlying portfolio (this turnover can bring tax costs). In contrast, mutual fund units are bought and sold through a mutual fund company, and this does result in turnover in the underlying portfolio.

Finally, inflows and outflows from the ETF are often transacted in-kind, which protects existing unitholders and avoids a taxable event.

ETF resources

To further help in your ETF research, there are several resources you can tap into:

- The ETF fund page on the provider’s website, which includes the end-of-day NAV price, management fee, holdings and more. For an example, see the Mackenzie Growth Allocation ETF page.

- The NEO Exchange ETF Screener page

- The TMX ETF Screener page

Stay tuned for part two in this series of “ETFs 201: The top ETF questions answered”, when we will look at what you need to consider regarding ETF trading volumes, market crashes and the importance of trading. If you have any other questions about ETFs, talk to your financial advisor.

Source:

1 National Bank: Canadian ETF flows

Commissions, management fees, brokerage fees and expenses all may be associated with Exchange Traded Funds. Please read the prospectus before investing. Exchange Traded Funds are not guaranteed, their values change frequently and past performance may not be repeated. The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of March 23, 2022. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.