Highlights

- The Canadian economy has been weakening since the Bank of Canada’s last rate hike in July 2023, distinctly underperforming most other advanced economies.

- Inflation is still trending above the Bank of Canada’s 2% target, but should stabilize below the 3% upper bound of the BoC’s tolerance band in the coming months.

- Rates are too high for the sputtering economy. The Bank will need to progressively lower them, likely starting in April.

The Bank of Canada (BoC) considers a slew of variables when it sets interest rates. All but one — inflation — are currently screaming for cuts. The economy has weakened across the board since the last rate hike in July 2023. The BoC now estimates the economy is operating with excess capacity (“slack”), a reversal from a few quarters ago when it was severely overheating. An optimist would say the Canadian labour market has flatlined; a pessimist would say it has deteriorated. The BoC’s own surveys — the Business Outlook Survey and the Survey of Consumer Expectations — highlight sliding confidence and easing inflation expectations. Finally, the federal government has adopted a cautious tone around public spending, a negative omen for short-term economic growth.

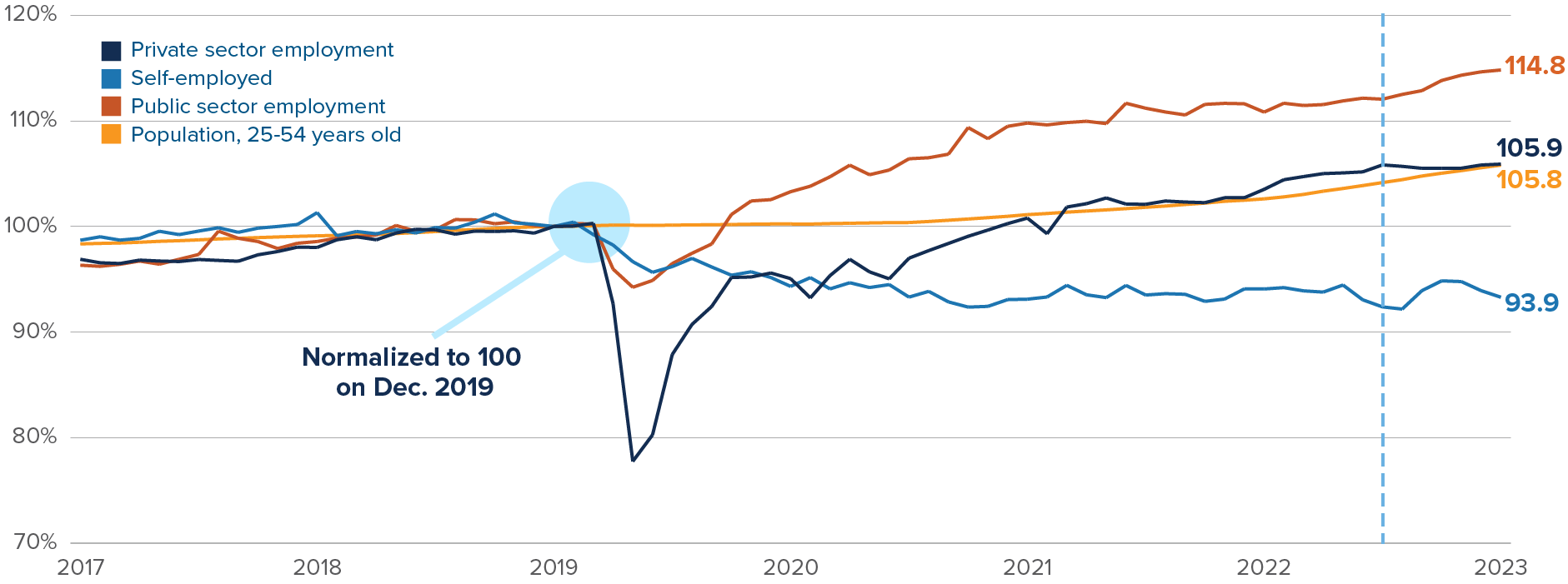

Canadian labour market data is particularly tricky to navigate these days. Two factors — government employment and immigration — have masked clear underlying weakness in the job market. First, while we haven’t seen outright job losses over recent quarters, we’ve seen far fewer job gains than we should have given population growth. Employment grew 1.4% annualized over the past six months, while the prime-age population — Canadians between 25 and 54 years old — grew 3.2%, more than double the rate. Second, the majority of net job growth in Canada over the past six months has come from government hiring. Canada created 104.3k jobs in the public sector (+4.9% annualized growth), versus only 35.6k in the non-public sector (+0.4% annualized growth).

Public sector employment has driven per-capita job gains in Canada since the pandemic

Employment by type, December 2019 = 100

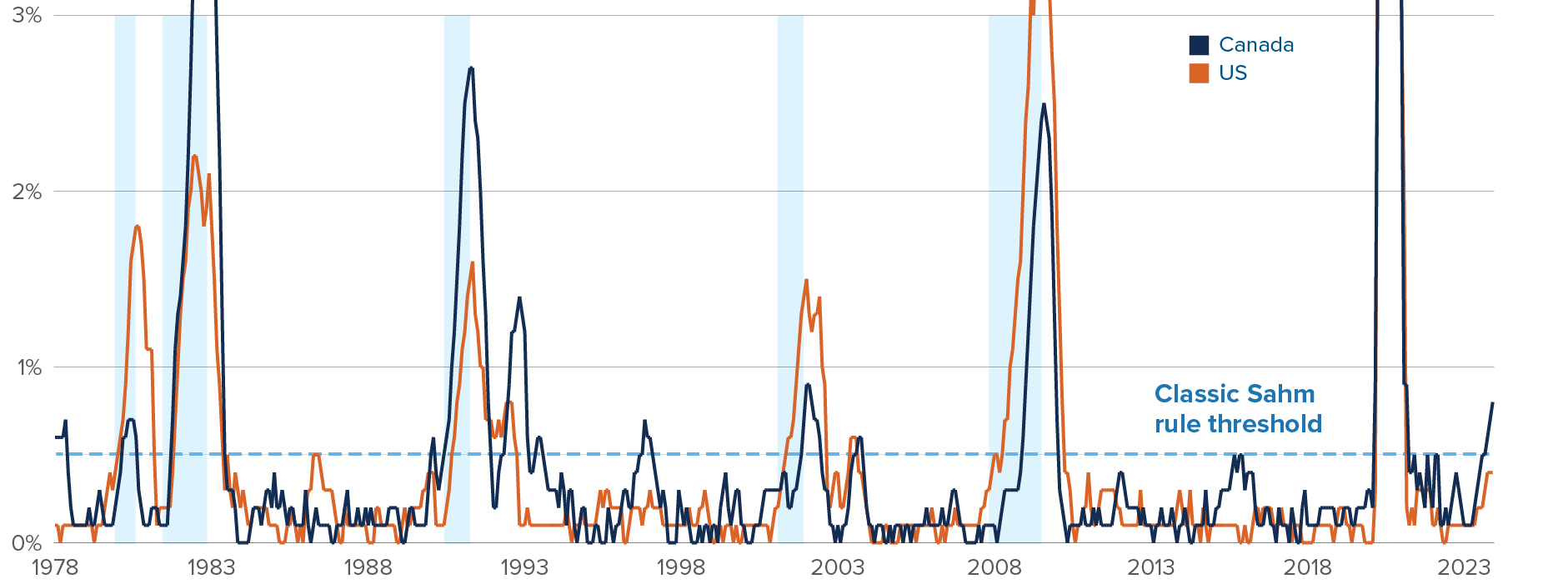

While the US labour market has held up admirably, Canada’s has shown no signs of breaking from its months-long weakening trend. The Sahm Rule recession indicator — the difference between the unemployment rate’s three-month average and its low point over the past 12 months — has interrupted its march towards recessionary territory in the US. But it has blown through the recession threshold in Canada.

Sahm Rule is flashing red in Canada, light yellow in the US

Unemployment rate, three-month average minus low point in past 12 months

The BoC’s policy rate is too high for the sputtering economy. The real interest rate — the policy rate minus inflation expectations — sits at a very restrictive level, above 2% by most measures. The level of real rates is what ultimately matters for the path of the economy; if a consumer is faced with a 5% nominal rate, but believes inflation will be 6% over the loan period (that is, a -1% real interest rate) they’ll likely keep on borrowing. But once nominal rates are above inflation expectations, borrowing becomes less attractive and consumption slows. Rates weren’t particularly restrictive a year ago, when the BoC did its first rate pause in January 2023. Today they obviously are.

Real rates are high with the economy running below capacity

Bank of Canada overnight rate minus forecasters’ average year-ahead inflation expectations

The BoC’s surprise rate increase in June and follow-up hike in July had a major impact on the Canadian economy. House prices are down around 7% since the resumption of hikes, fully reversing their first-half gains triggered by the BoC’s initial pause in January. In the second half of 2023, consumer and business confidence deteriorated as macro uncertainty rose. Inflation expectations have been normalizing, resulting in higher effective real interest rates. In this environment, rates can’t stay at 5% for long. The question is when they’ll come down.

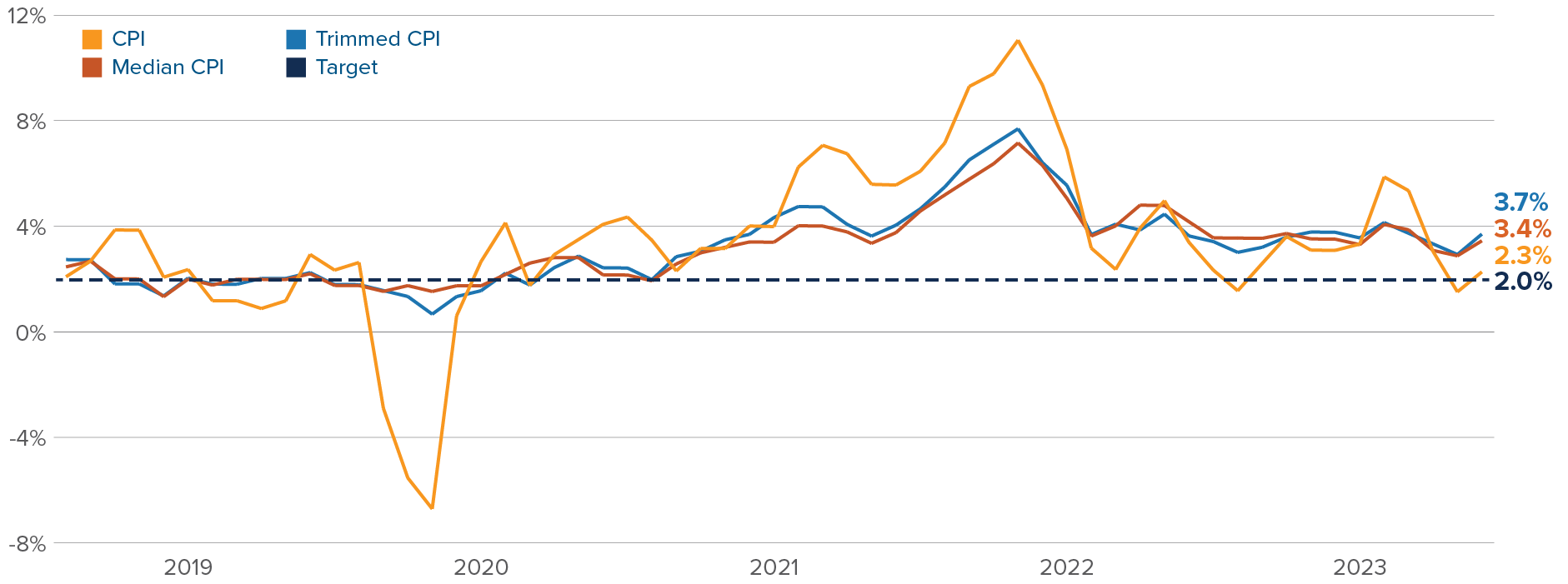

Core inflation is stubbornly sticking above the 3% upper bound of the BoC’s target range

Canada inflation, three-month annualized

While the weak macro environment suggests inflation slowing to 2% soon, current inflation is too high for the BoC to cut. Tiff Macklem and company won’t budge from 5% with three-month annualized core inflation above 3%. But they won’t wait for core inflation to stabilize at 2% either. The most recent Monetary Policy Report emphasized the weakness in the Canadian economy and Macklem’s press conference on January 24 made clear that the BoC is ready to pivot. The March decision date is unlikely to see a cut, given sticky inflation. We see April as the most likely date for a start to the rate-cutting cycle. And with such a weak economy, once the BoC starts cutting, a one-cut-per-meeting pace is very possible.

Capital markets update

What we’ll be watching in February

February 9: Canada January jobs report

- As discussed earlier, Canada’s job market has been deteriorating steadily over the past six months, even though population growth and government hiring have partially concealed the weakness in the labour market.

- Outright job losses in January would probably ratchet up bets on a BoC rate cut in April. As of end of January, markets see two-thirds probability that the BoC cuts by April.

February 14: Japan fourth quarter GDP

- Fourth quarter GDP growth will factor in the Bank of Japan’s (BoJ) monetary policy decision over the coming months.

- Positive real GDP growth would clearly calm some nerves at the BoJ, where officials are getting ready to hike rates for the first time in more than a decade. But we’ll mostly focus on the details of the report. First, will household spending show signs of acceleration? Second, will nominal GDP (not adjusted for inflation) maintain its torrid pace?

February 29: Canada fourth quarter GDP

- A second consecutive quarter of negative GDP growth would confirm Canada’s recessionary trajectory.

- We’ll be keeping an eye on the household consumption component of GDP, which stagnated in the second and third quarter of 2023. While spending on services grew slightly in the third quarter, spending on goods has been declining for a few quarters, weighed down by high interest rates.

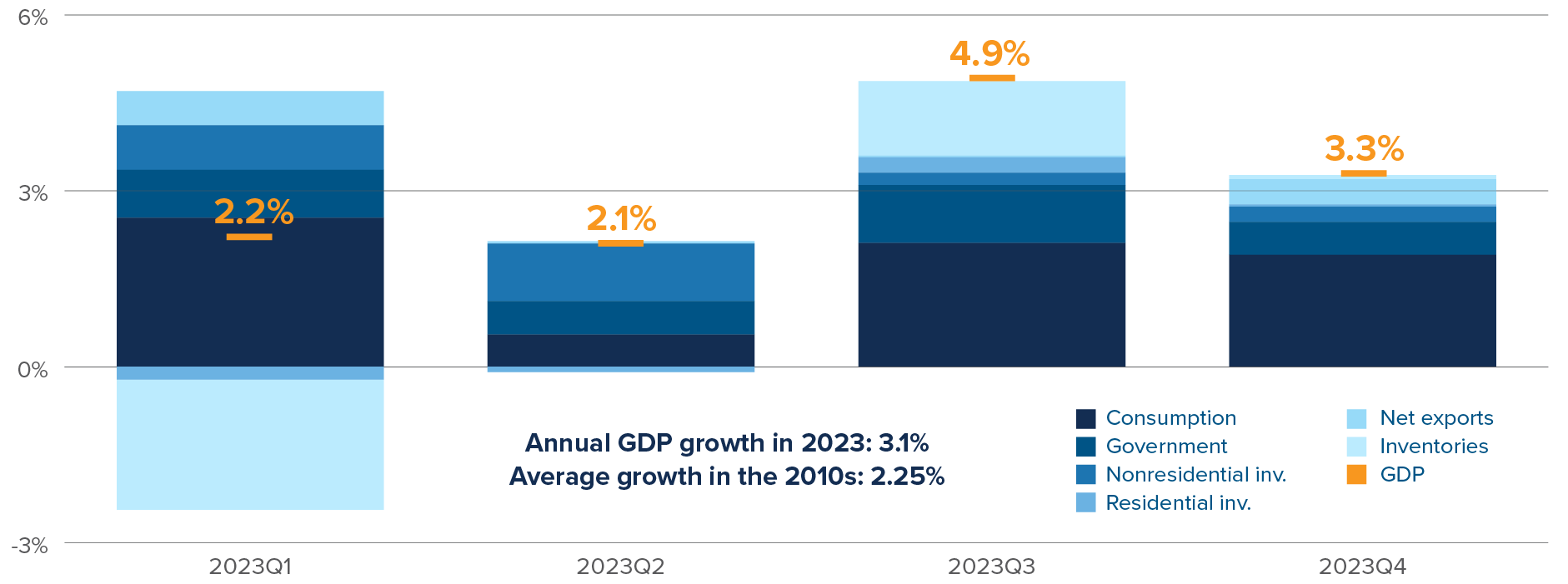

Emerging theme: Be careful betting against the US economy

US real GDP growth exceeded the average economist’s forecasts in every quarter last year. The US economy’s resilience in the face of rising rates has been remarkable. We always expected the US economy to avoid a recession in 2023, but even we didn’t expect such rapid growth. Real consumer spending grew 2.6%, accelerating from 2022’s 1.2% growth rate, a truly exceptional outcome.

What explains the US economy’s strong all-around growth and resilient job market? If we had to pick three main factors:

- Government spending. The federal government’s deficit, clocking in at 6.7% of GDP, boosted non-residential investment and supported household consumption.

- Supply-side healing. Repaired supply chains and cooling energy markets improved productivity and freed up disposable income.

- Interest rates. Real interest rates were only mildly restrictive in the first half of 2023.

At the risk of sounding repetitive, we don’t see the US economy sliding into a recession in 2024 either. While real interest rates are now solidly restrictive, the Fed has stopped hiking and consumer confidence is about to pick up, with Americans experiencing cooling inflation and juicy investment returns. Government spending, the main force behind 2023’s economic growth, will still be a major growth driver in 2024. We project a deficit around 7% GDP in this election year.

US GDP growth was perfectly balanced in Q4, setting up 2024 nicely

Source: Bloomberg, as of 2023 Q4.

Source: Bloomberg, as of 2023 Q4.

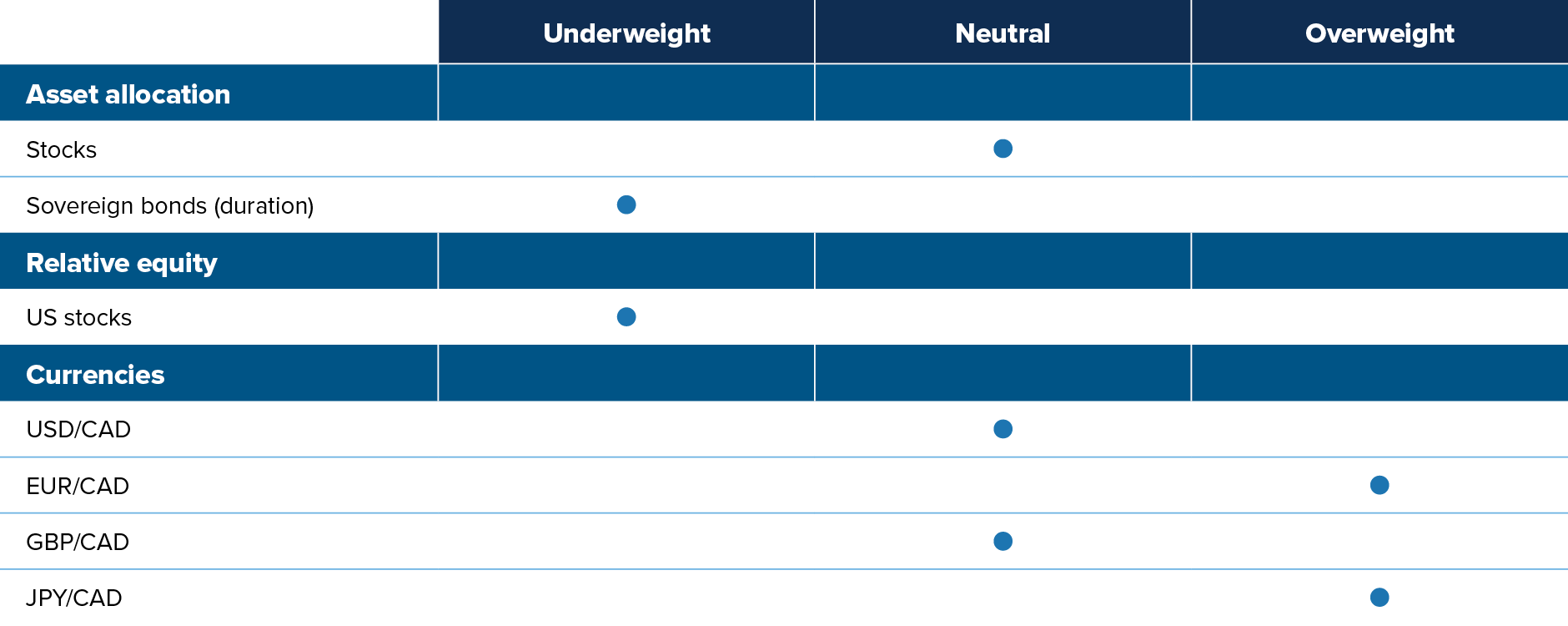

Multi-Asset Strategies Team’s investment views

Tactical summary

Note: The views expressed in this piece apply to products that are actively managed by the Multi-Asset Strategies Team.

Positioning highlights

Fed pricing reversal: At the start of the year, markets were expecting six Fed rate cuts in 2024. That was a stretch in our view, given the hot economy and the “transitory” forces behind recent disinflation. After upside surprises in economic releases, markets are now betting on five 2024 cuts. This is more reasonable, but we'll still take the under. While the disinflationary trend is clear, we don't see inflation stabilizing at 2% over the next few months. We also think the Fed will err towards keeping rates tighter than what a classic monetary policy rule would suggest. FOMC members understand that the recent market action suggests financial conditions have loosened significantly in recent weeks, in effect substituting for rate cuts.

Overvalued US assets: We generally don’t like US assets in early 2024, whether equities, stocks or the US dollar, as covered at the beginning of this commentary. Within US equity markets, we prefer small-cap stocks: valuations are more attractive than large caps, and market sentiment is improving quickly. In terms of sectors, we like energy (cheap, positively exposed to our bullish view on oil) and dislike utilities (declining profitability, poor macro backdrop).

Canadian landing: The macro situation in Canada appears much more dire than in the US. Data has already started turning. The Sahm Rule, which uses changes in the unemployment rate to date recessions, is flashing red. We dislike the Canadian dollar against most currencies.

Commodity-exporting EM currencies: Commodity-exporting EMs are well situated to outperform in this macro environment. Their budgetary and external balances have improved amid high global nominal growth and high commodity prices. Their central banks started raising rates much earlier than the rest of the world. As a result, they have generally reached the end of their tightening cycle, reducing the risk of overtightening into a recession. But the level of rates remains high, offering positive carry over most other currencies. On the other hand, we hold a negative view on the currencies of Asian EM countries. Their external positions have severely deteriorated, and their interest rates are relatively low.

Oil market tightness: The physical oil market is tight, especially with the ongoing one-million-barrel-per-day Saudi production cut and upcoming refill program for the US Strategic Petroleum Reserve. In the absence of a global recession, which we don’t expect to occur anytime soon given the positive momentum in the US and the expansionary deficits from governments around the world, oil should remain undersupplied. A stabilization of the Chinese economy will trim risks around oil demand. Positioning is also constructive for the oil complex. For much of 2023, investors were expressing recession bets through short oil derivatives positions. These bets have been coming off, with room to run.

Japan policy divergence: The BoJ widened the tolerance band around its 10-year yield target by 25bps back in December 2022, and by an additional 50bps in July 2023, before adding flexibility around the band in October. With the yen still undervalued and core inflation sticking above 2%, the BoJ will likely tighten further in 2024. We expect the BoJ to finally abandon its negative rate policy in April. We are short Japanese government bonds in our Global Macro Fund. We also have a long discretionary position in the Japanese yen (versus both the euro and the US dollar) to take advantage of Japan policy normalization and the yen’s undervaluation. We like long JPY/EUR because (1) the yen is more undervalued than the euro, (2) the ECB has overtightened and (3) growth is already slowing in the euro zone while it continues to chug along in Japan.

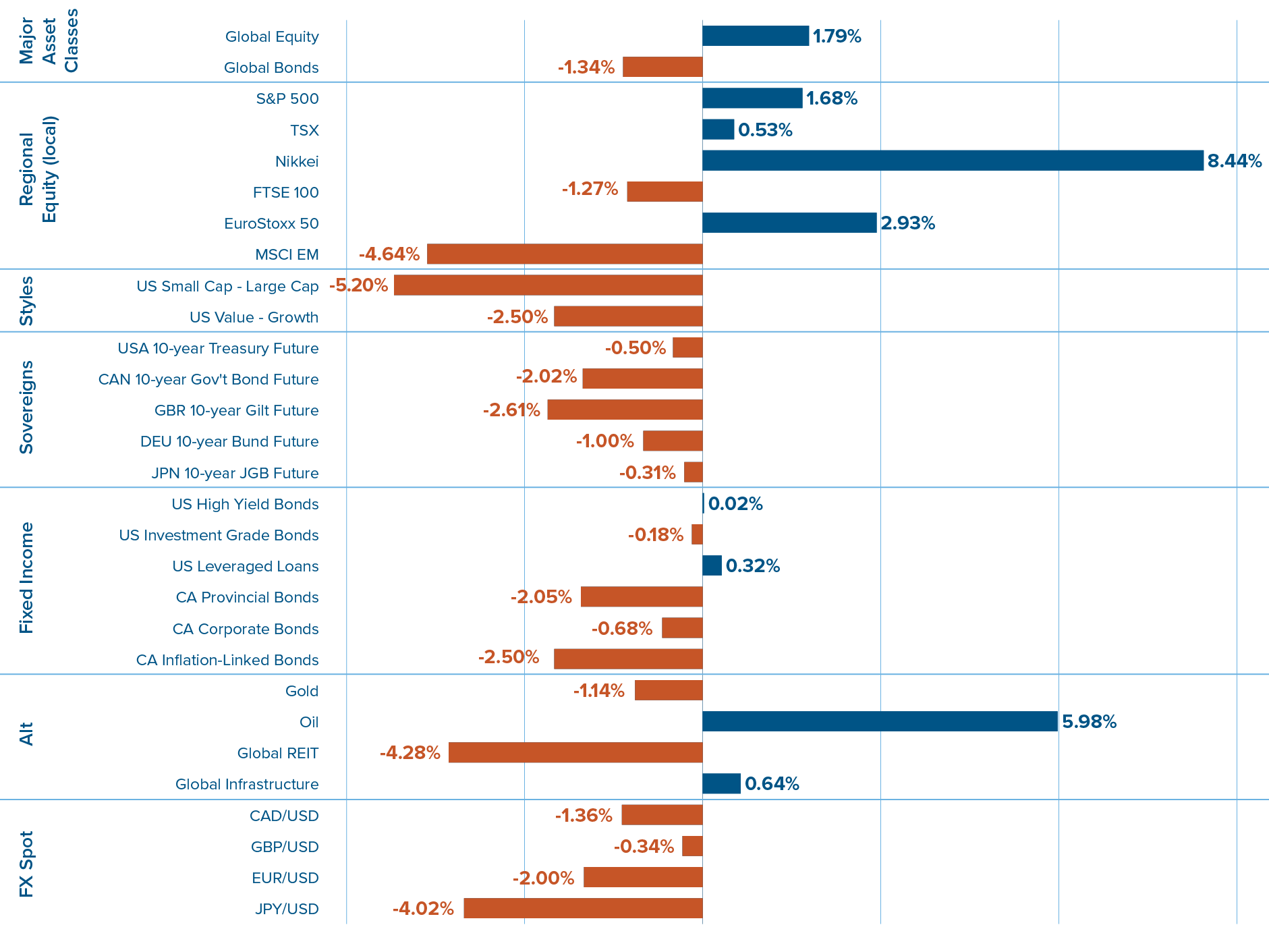

Capital market returns in January