Active fixed income ETFs: Managing risk in an inefficient market

About the author

IN THIS ARTICLE min read

Active fixed income ETFs can offer a structural advantage over passive strategies in an inefficient bond market. Passive approaches are often forced to hold the most indebted issuers and react to credit deterioration, while active managers can proactively manage risk, avoid weakening credits, and exploit pricing inefficiencies – improving downside protection and long-term risk-adjusted outcomes. Over the past 10 years, this approach has been tested across market cycles, reinforcing the value of active management in fixed income.

This year, Mackenzie Investments is proud to celebrate the 10-year anniversary of four of our core actively managed fixed income ETFs:

ETF Name | Ticker | Management Fee |

MKB | 0.40% | |

MUB | 0.50% | |

MGB | 0.50% | |

MFT | 0.60% |

Mackenzie Investments started its journey as an ETF provider with the launch of innovative actively managed fixed income ETFs in April 2016.

On April 19, 2026, MKB, MUB, MGB and MFT reached their 10-year anniversaries since inception. These ETFs have navigated changing market cycles, demonstrating the tangible benefits of an active approach. Their continued success stands as a testament to our investment management expertise and our commitment to delivering value for our partners and their clients.

Why active management has an advantage in fixed income

In today's dynamic market, advisors are increasingly turning to fixed income to provide stability and income for client portfolios. As the investment landscape evolves, the age-old debate of active versus passive management has given way to a more critical strategic question: In which asset class is the value proposition of active management not just marginal, but structurally essential?

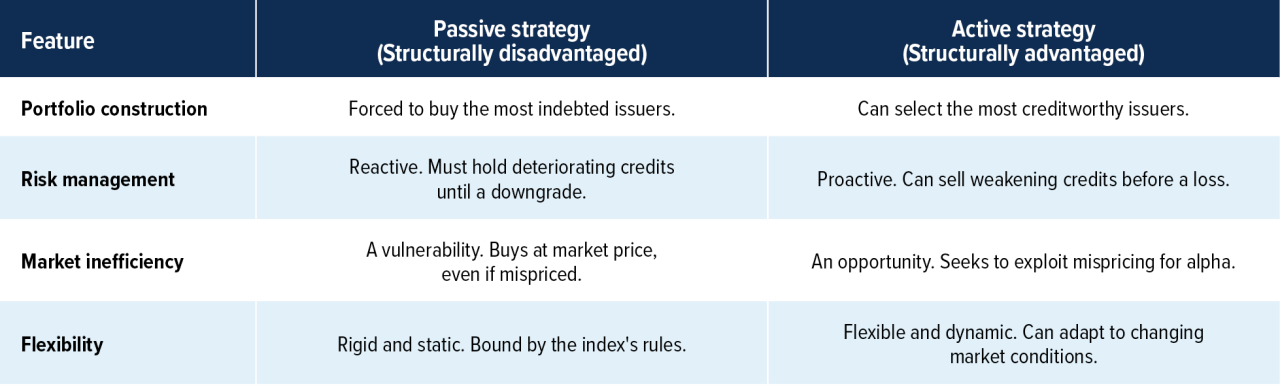

While the active versus passive debate is less pronounced in the equity world, the very structure of the fixed income market gives active management a fundamental and inherent advantage. Passive strategies, which are designed to mirror an index, are often structurally disadvantaged by the unique characteristics of bonds. Active management, in contrast, is designed to exploit these characteristics.

Active managers have the flexibility to:

- Navigate changing interest rate environments: In a world of shifting monetary policy, the ability to dynamically adjust duration and credit exposure is paramount.

- Capitalize on market inefficiencies: The vast and complex nature of the bond market creates pricing inefficiencies that skilled managers can exploit.

- Manage risk proactively: Active managers can sidestep overvalued sectors or issuers and position portfolios defensively when market conditions warrant.

While passive fixed income strategies can play a role in portfolio construction, particularly for broad market exposure, they are subject to certain structural limitations:

- Flawed methodology: Many passive funds are debt-weighted, forcing them to allocate the most capital to the most indebted companies and governments. In contrast, active managers can focus on credit quality and fundamentals.

- Market inefficiency: The bond market's over-the-counter (OTC) nature and the complex features of its securities create pricing anomalies. Active managers can exploit these anomalies through expert analysis, while passive funds cannot.

- Poor risk management: Given the asymmetric risk of bonds (more downside than upside), passive funds can be structurally limited because they must hold deteriorating securities until a formal downgrade. Active managers can proactively sell to protect capital from these predictable losses.

Fixed income's crucial function

Fixed income's core function is to anchor a portfolio with stability and income, not necessarily to drive its growth; it also serves to diversify against equity risk, preserve capital, and ultimately improve overall risk-adjusted performance.

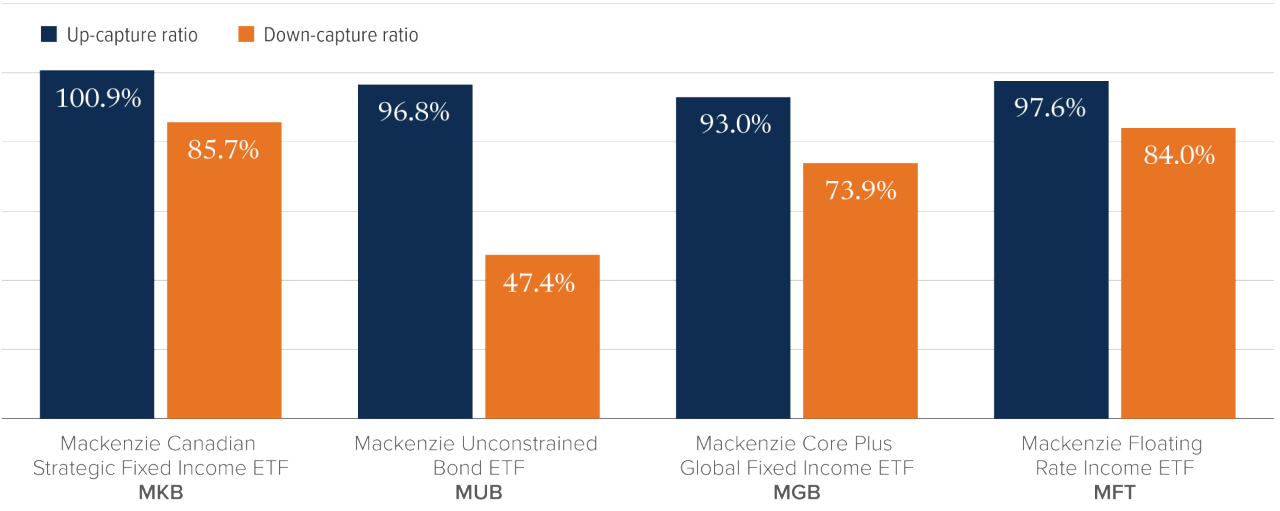

An actively managed fixed income strategy might choose to try to outperform its benchmark by adopting an approach that does not maximize its upside capture, but rather to minimize downside capture (versus the index). By focusing on risk management, capital preservation and downside protection – while still capturing index beta on the upside – the strategy can, if successful, outperform its benchmark with lower downside capture. In other words, it can deliver better returns with less risk, with behaviour resembling the index.

For example, below we show the upside and downside capture rate of MKB, MUB, MGB and MFT. These actively managed ETFs capture close to 100% of the benchmark’s upside and capture between 47% and 86% of the downside trend of the benchmark.

Up and down capture ratios

Source: Mackenzie Investments, Morningstar Direct for the period since inception (April 19, 2016) to April 30, 2026. Average upside and downside capture ratios calculated on gross monthly returns vs. the respective benchmarks (FTSE Canada Universe Bond Index, Bloomberg Multiverse TR CADH, ICE BofA Global Broad Market TR CADH, and Morningstar LSTA Leveraged Loan TR CADH).

Outsourcing fixed income to focus on areas that generate alpha

For the modern IIROC advisor, the highest-value use of their time is not in the granular, time-consuming task of managing the fixed income sleeve. The fixed income landscape is a vast and notoriously complex arena, requiring dedicated resources, specialized expertise, and a significant operational burden that can detract from an advisor's core focus. By strategically outsourcing fixed income management to a dedicated team of experts, advisors can liberate their time and resources to concentrate on the high-impact activities that truly define their value proposition and generate alpha: holistic financial planning, strategic asset allocation, tax optimization, and crucial behavioral coaching that keeps clients on track to meet their goals.

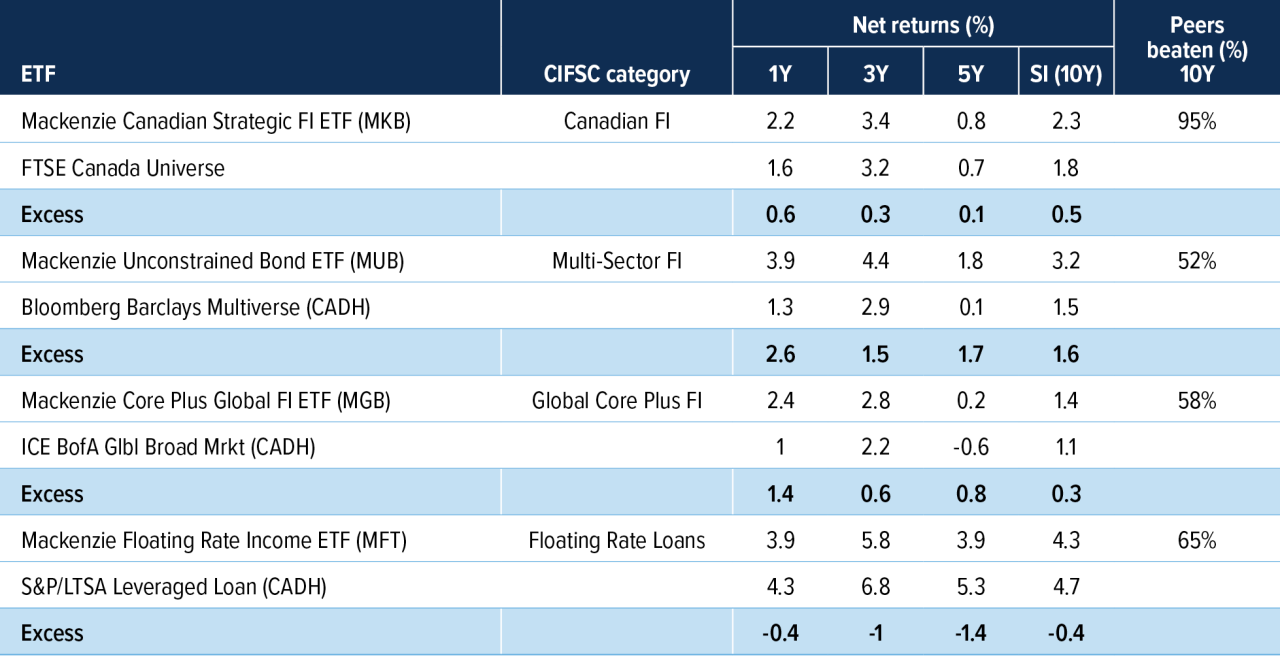

Celebrating a decade of active excellence

The table below shows performance and excess returns versus respective benchmarks, highlighting the value of fixed income active management.

Source: Mackenzie Investments. As of April 30, 2026. *Since inception: April 19, 2016.

This 10-year anniversary of our pioneering active fixed income ETFs is more than a milestone; it is a testament to our core belief that active management is a powerful tool for securing long-term financial success.

We invite you to learn more about how our suite of active fixed income solutions can help you build more resilient and opportunistic portfolios for your clients.

For more information about Mackenzie active ETFs, explore our product roadmap.

Commissions, management fees, brokerage fees and expenses may all be associated with Exchange Traded Funds. Please read the prospectus before investing. Exchange Traded Funds are not guaranteed, their values change frequently and past performance may not be repeated.

Index performance does not include the impact of fees, commissions and expenses that would be payable by investors in the investment products that seek to track an index.

The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This article may contain forward-looking information which reflect our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of April 30, 2026. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.