Excess return and tracking error can be valuable tools when trying to measure the performance of an index ETF. But what do these terms mean, exactly? And how can they help you to make better investment choices?

Active investing strategies are designed to outperform their respective benchmarks over the long term. To measure their success, they use metrics such as alpha (a fund’s performance above that of its benchmark), its Sharpe ratio and information ratio.

In contrast, index investing strategies are designed to closely mimic their underlying index and are measured by excess return (also known as tracking difference) and tracking error.

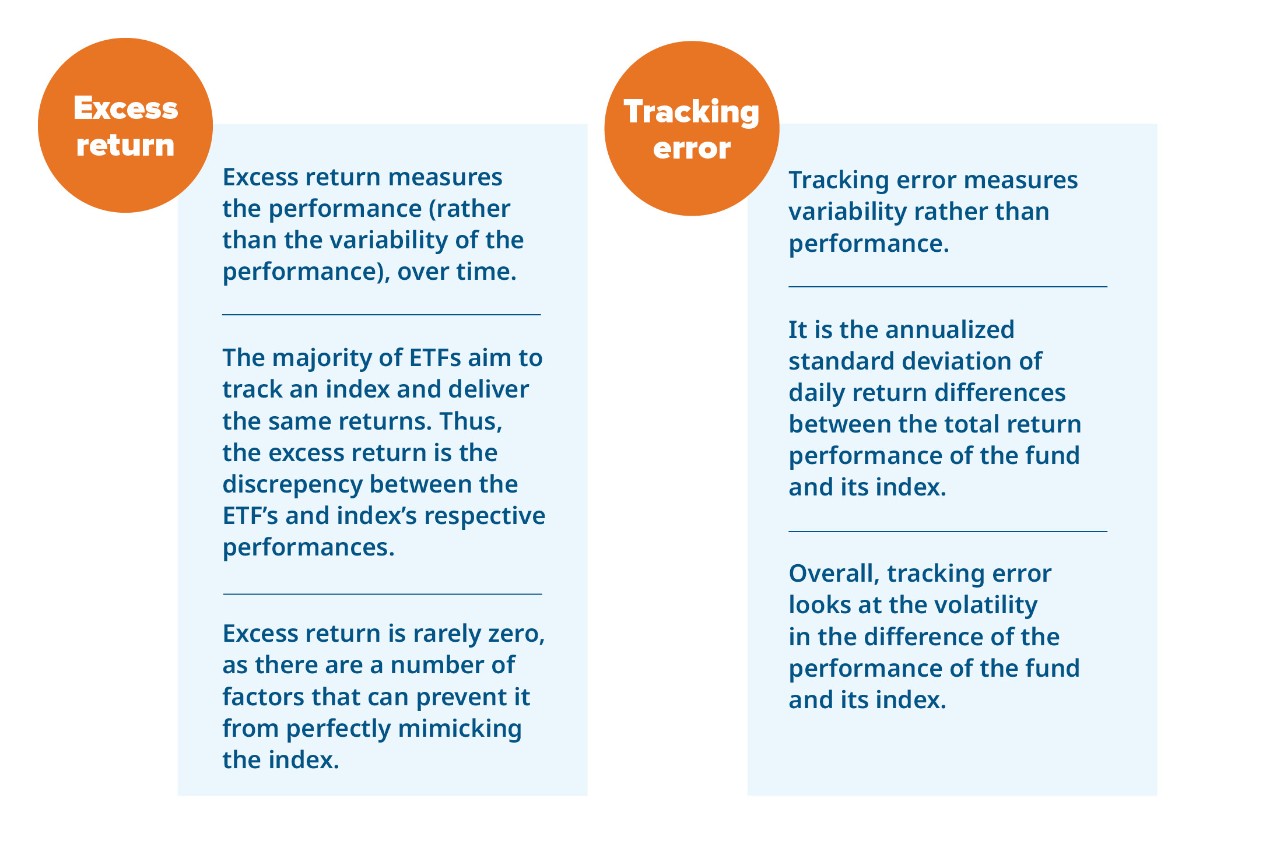

Excess return measures the performance of a fund or ETF compared to its index, over a period of time. It’s calculated by taking a fund’s net asset value (NAV) total return and subtracting the index’s total return. Since a fund’s NAV total return includes expenses, excess return is usually negative for index funds.

Tracking error measures the consistency of a product’s excess return over the same period. This represents the annualized standard deviation of excess return for a stated period. This measure can be used to assess the consistency of a fund’s average excess return.

Excess return and tracking error broken down

If your primary focus is on total return, then excess return is more important than tracking error when assessing index ETFs. If performance consistency is an important consideration, then tracking error may be more relevant.

Factors affecting an index ETF’s performance

While index ETFs attempt to match the index’s performance as closely as possible, the excess return is rarely flat. There are several factors that can mean an ETF doesn’t perfectly copy the performance of its index, including:

- Fees: Management expense ratios can be the best measure of future excess return (or tracking) differences. Even the lowest management fee can contribute to tracking difference.

- Rebalancing and trading costs: The trading costs associated with rebalancing will have an impact on the excess return and tracking error of an ETF. Trading costs can vary across different markets and types of securities, with some being more expensive than others. The timing of rebalancing trades can also contribute to tracking error. Raising cash for distributions from the ETF can further contribute to trading costs.

- Diversification rules: For example, in the US, ETFs cannot hold more than 25% of a single stock, which can make it impossible to truly replicate certain indices.

- Degree of replication: Sometimes it’s not practical to invest in every single security within an index. Portfolio managers regularly consider the trade-offs between trade costs and the performance contribution of investing in all securities within the index.

- Cash flow management: An ETF’s performance may be impacted by cash. An ETF can receive dividends and/or coupons, which may or may not be reinvested immediately. There can also be residual cash as part of creation or redemption activity that occurs in the ETF.

- Pricing and withholding tax differences: There can be differences between the timing of spot rates and foreign exchange rates in an index, compared to the ETF. There are also differences in withholding tax rates used in the index versus the rates impacting the ETF.

- Securities lending: Some ETFs lend their securities to borrowers, who pay interest in return. This can create additional revenue for the ETF, ultimately reducing the costs within the ETF and improving excess return.

How differences in methodologies can have an impact

Comparisons between ETFs and the indices they track can be problematic because of differences in indexing methodologies and data calculation approaches across various ETF providers and index providers. These differences include:

- Using NAV pricing versus market pricing of ETFs

- Fair-value pricing of securities when foreign markets are closed

- Timing differences on exchange rates

- Closing prices using last recorded trade versus a midpoint between market bid and ask

It’s wise to track excess return and tracking error data over longer time periods. Data comparisons over short time periods can be a challenge due to differences in index construction and data calculations that can exhibit more variant behaviour in the short-term.

How to consider tracking error when choosing ETFs

When buying an index-tracking ETF, you typically want it to closely mimic the performance of its underlying index. You can calculate excess return by using the data provided by each index provider on their website and comparing it to a fund’s performance. On Mackenzie’s website, for example, we provide details on both a fund’s NAV returns and its index return. The fund’s NAV return subtracted by the index return equals the excess return.

Tracking error is a little trickier to calculate. Investors would have to manually calculate this information by pulling daily, weekly or monthly fund NAV returns and corresponding index returns. Advisors can ask for this information from their ETF provider.

Investors should discuss excess return and tracking error with their financial advisors. For advisors, contact your Mackenzie sales team to discuss how our ETFs perform compared to their indices.

Commissions, management fees, brokerage fees and expenses all may be associated with Exchange Traded Funds. Please read the prospectus before investing. Exchange Traded Funds are not guaranteed, their values change frequently and past performance may not be repeated. The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of February 23, 2022. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.