Currency management: global fixed income opportunities

IN THIS ARTICLE min read

Fixed income fund performance is primarily driven by two key factors: the portfolio’s exposure to credit risk and interest rate risk. What gets less attention is the overlay and impact of currency management within an active solution, as part of the fund’s investment process and philosophy. We briefly covered this subject in our previous article, Optimizing bond portfolios with global fixed income, which highlighted currency as a strategic lever in global fixed income.

Imagine you buy a US-dollar bond as a Canadian investor. Your return in Canadian dollars depends on two factors: the bond’s return in US dollars and any change in the USD/CAD exchange rate. If the bond earns 10% in USD, and the US dollar strengthens by 5% against the Canadian dollar, your return would be about [(1+10%) (1+5%)] −1 = 15.5%. But if the US dollar weakens by 5%, your return drops to about 4.5%. That’s why currency swings can significantly impact your portfolio, and why some investors choose to hedge. In this article, we do a further deep dive into the catalysts that drive our exchange rate views, as well as the operational cost of hedging these exposures back to CAD.

Drivers of currency exchange rates

An exchange rate simply reflects how much one currency is worth compared to another. But it’s not just about a country’s own economic strength, it’s about relative performance. For example, Canada’s growth outlook matters, but so does how it stacks up against the US or Europe. While increasing money supply can lead to inflation and in extreme cases, hyperinflation, as seen in Zimbabwe, that’s only part of the story. Argentina’s repeated currency crises are an example of how chronic fiscal deficits and reliance on money printing to finance spending, erodes confidence in pesos, fueling inflation and driving investors toward a safer currency. Modern currencies are influenced by a complex mix of factors, including interest rate differentials, inflation expectations, trade balances, current account positions, and political and policy credibility.

Interest rate differentials between countries play a meaningful role in shaping currency movements. At a basic level, higher interest rates in a country can attract foreign capital, as investors seek better returns, and this demand for local assets often supports the domestic currency in the short term. Some academic models, suggest that currencies with higher interest rates should depreciate over time to offset the yield advantage. But in practice, this theory often breaks down. Many investors pursue carry trades, where they borrow in low-yielding currencies and invest in high-yielding ones, betting that the higher-rate currency will appreciate or at least remain stable. However, they are vulnerable to sudden reversals, if the high-yielding currency weakens or global risk sentiment shifts, investors may unwind positions quickly, leading to sharp currency moves.

So, while central banks may raise interest rates to defend a weakening currency, especially during periods of capital flight or inflation, the outcome depends on broader macroeconomic conditions, investor sentiment and credibility of the monetary authority. Rate hikes can be supportive, but they’re not a guaranteed fix.

In short, currency values are shaped by relative fundamentals and global capital flows, and not just domestic money printing. Understanding this interplay is key to active currency management.

Drivers of exchange rate dynamics

Factor | Action | Impact on currency | Rationale | |

Interest rate differentials | Higher rates | → | Appreciates | Attracts foreign capital seeking yield; boosts demand for the currency. |

Inflation rate | Higher inflation | → | Depreciates | Erodes purchasing power; central banks may tighten or loosen policy accordingly. |

Trade balance | Surplus | → | Appreciates | Net exports increase demand for domestic currency; deficit does the opposite. |

Fiscal policy and debt levels | Expansionary policy | → | Depreciation | Rising debt may raise default risk or inflation expectations. |

Monetary policy stance | Hawkish | → | Appreciates | Signals tighter liquidity and higher future rates; dovish stance weakens currency. |

Political stability and governance | Stability | → | Appreciates | Reduces risk premium; attracts long-term foreign investment. |

Commodity prices (for exporters) | Commodity prices | → | Appreciates | For commodity-linked currencies (CAD, AUD, etc.), higher prices boost terms of trade. |

Capital flows (FDI and portfolio) | Inflows | → | Appreciates | Reflects investor confidence and demand for domestic assets. |

Global risk sentiment | Risk-on | → | EM currencies appreciate | Investors seek yield in risk-on; flee to safe havens (USD, CHF, JPY) in risk-off. |

Central bank intervention | Intervention | → | Mixed impact | Can stabilize or distort currency depending on credibility and scale. |

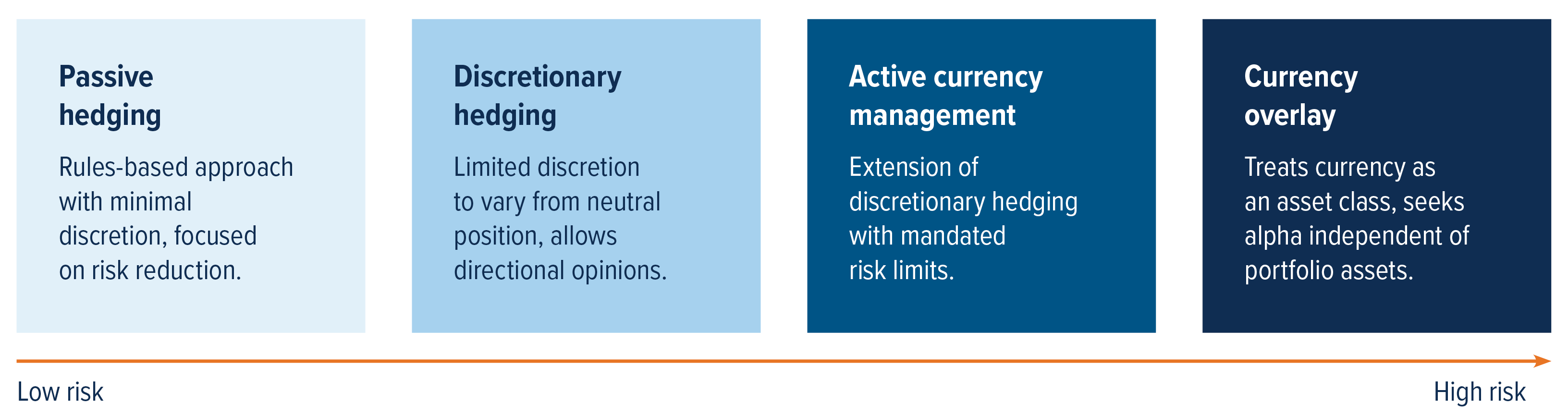

Currency management: turning volatility into opportunity

Currency markets can be volatile in the short term, and sometimes currencies are mispriced. Active currency management aims to take advantage of these inefficiencies to boost portfolio returns. Strategies range from conservative approaches that aim to reduce risk, to more aggressive ones that seek to profit from currency movements.

Hedging: a safety net for investors

Currency hedging is a strategy used to separate the impact of foreign exchange (FX) swings from the performance of the actual investment. In fixed income portfolios, currency and bond returns often move together because both are sensitive to interest rate changes. This makes carrying open currency exposure more relevant in global portfolios.

Our fund invests globally, so we often hold US dollar bonds. To protect Canadian investors from currency swings, we hedge the US dollar exposure using 1-month USD/CAD forward contracts, a standard approach used by most global bond indices. The cost of hedging stems from the difference in interest rates between Canada and the US. As at the time of writing, the CAD is trading at a discount. For example, at the end of October, the spot price for USD/CAD was 1.401 and 1-month forward contracts priced at 1.3989 (a discount of 0.002148). This discount translates into an annualized hedging cost of about 1.8% Today, that cost is higher because US interest rates are above Canadian rates. Before rate hikes, hedging was almost free. Now, it can shave off nearly 1.8% annually. So, managers must weigh the trade-off: hedge for stability or leave some exposure open to capture potential gains.

Global portfolios will typically have exposure to more than one foreign currency. The mandates will generally hedge back a substantial amount of foreign currency exposure to Canadian dollars. Our team has strong capabilities in FX markets and maintains the flexibility to leave the foreign currency exposure open (unhedged or partially unhedged) based on a favourable FX valuation or as a risk mitigation tool. Managing emerging market currency exposure involves unique challenges with higher trading costs under normal market conditions and severe illiquidity under stressed market condition. The liquidity issue is especially important when trades in these less-liquid currencies get “crowded,” and can occasionally be subject to panicked unwinds as market conditions suddenly turn. (reference: Fixed Income Team Quarterly Report)

Global fund positioning | US (%) | Euro (%) | Select EM (%) | |||

Gross | Open | Gross | Open | Gross | Open | |

25.5 | 3.2 | 40.9 | 0.6 | 6.0 | 6.0 | |

46.4 | 3.2 | 18.1 | 0.2 | 6.6 | 6.6 | |

45.6 | 2.9 | 15.4 | 0.1 | 7.3 | 7.3 | |

62.6 | 3.4 | 0.8 | 0.0 | 2.8 | 2.8 | |

60.9 | 3.2 | 0.0 | 0.0 | 0.0 | 0.0 | |

97.0 | 7.3 | 0.4 | 0.0 | 0.0 | 0.0 | |

Source: Mackenzie Investments, as at December 31, 2025. “Gross” reflects full currency exposure before hedging and “open” reflects residual currency exposure after hedging. Select EM includes local currency exposure to Mexico and Brazil.

In global investing, managing currency isn’t optional, it’s essential. Active currency management isn’t about predicting every move, but it’s reducing surprises and finding opportunities. Currencies move for reasons beyond our control such as interest rates, trade flows, even global risk sentiment. In a world where currencies can swing as much, smart management can turn volatility into value. Active currency management helps protect your portfolio and, at times, can unlock extra gains.

Disclaimer

Commissions, trailing commissions, management fees and expenses all may be associated with mutual fund investments. Please read the prospectus before investing. Mutual funds are not guaranteed, their values change frequently and past performance may not be repeated. The indicated rates of return are the historical annual compounded total returns including changes in share or unit value and reinvestment of all dividends or distributions and does not take into account sales, redemption, distribution, or optional charges or income taxes payable by any securityholder that would have reduced returns. Mutual funds and Exchange Traded Funds are not guaranteed, their values change frequently and past performance may not be repeated.

The content of this document (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document may contain forward-looking information which reflect our or third-party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of January 12, 2025. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.