Whether to hedge or not is a question that most Canadian investors face at some point. Given the relatively small size of our economy (1.86% of global GDP) and stock market (3.13% of the MSCI World Developed Markets Index), diversification is essential. However, buying foreign assets leads to currency risk.

At least 30% of all Canadian-listed ETFs are hedged back to the Canadian dollar.1 If we were to also consider actively managed ETFs, in which portfolio managers often hedge foreign currency exposure, that number would be higher.

Why hedge foreign currency exposure in an equity ETF?

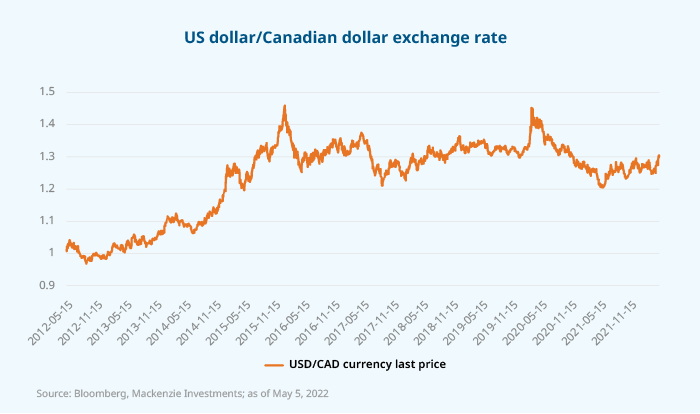

Hedging is designed to neutralize changes in value due to currency fluctuations, as these can significantly impact investment returns. Over the last 10 years, the US dollar has strengthened considerably against the Canadian dollar, so hedging currency risk would not have generally worked in your favour.

Here’s an example: imagine you bought a stock for US$100 in early 2013. At the time, the exchange rate was approximately at parity, so it would have roughly cost you C$100 to buy US$100.

Fast forward to today: even if your stock returned 0%, by converting it back into Canadian dollars at today’s exchange rate, (roughly US$1 = C$1.28)2 you’d have C$128. In other words, the currency alone returned 28% on your investment. Obviously, this can also move in the opposite direction.

Most index ETFs that provide exposure to non-domestic fixed income assets are hedged. This is because, when buying fixed income, investors generally tend to expect lower returns but higher certainties on the outcome, when compared to equities.

Let’s take an example of a Canadian investor who holds US Treasuries (yielding 3%), to diversify the US equities risk in their portfolio. Assuming US Treasuries remain stable and pay out their coupon, the investor would receive a 3% yield on that part of the portfolio.

However, imagine that their exposure to US dollars is not hedged and that the loonie strengthens against the US dollar by 10%. This currency move would more than dwarf the 3% yield, leading to a considerable loss. This explains why currency hedging is far more prevalent among non-domestic fixed income ETFs than equity ETFs.

How does hedging work?

Hedging is generally done once a month (at the month’s end), by buying forward contracts on the notional amount to be hedged.

The hedged amount is adjusted for the fund’s inflows and outflows intra-month, but not adjusted for performance, because of the costs involved. It’s impossible to know what the underlying securities’ value will be at the end of the month, because of market fluctuations. The hedge which is put in place at the start of the month will therefore almost never end up being perfect, due to the subsequent performance of the underlying assets.

Hedging currency is never perfect, with a trade-off between accuracy and cost. While adjusting the hedge daily would ensure accuracy, it would also be too costly. Adjusting quarterly or yearly would lower trading costs, but this would render the hedge too stale, so the widely accepted compromise is to adjust on a monthly basis.

This example will illustrate the issue: we need to hedge $1 million of US equities back to the Canadian dollar. We buy one-month currency forwards to hedge a notional value of US$1 million. During that month, US equities increase in value by 10%, so their value is now US$1.1 million. While this is great news, the hedge was only put in place on US$1 million notional value, so the extra $100,000 in appreciation is not hedged.

The timing of the underlying performance will also have an impact on the imperfection of the hedging. A sudden spike in the underlying value right after the hedge was put in place will result in the extra value being unhedged for almost an entire month, potentially leading to more slippage when compared to a situation where the change in value happened closer to the reset date.

Whether the effect of the over/under hedging will be positive or negative will depend on the exchange rate movement during that period. To help summarize the impact of imperfect hedging see the table below:

How have Canadian-hedged US equity ETFs performed in the past?

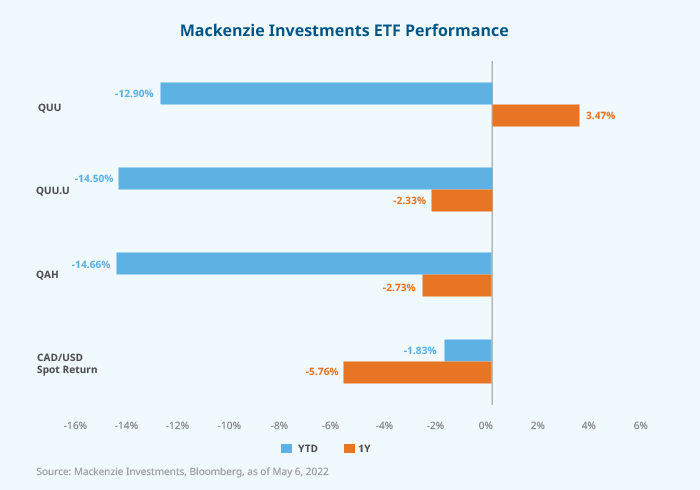

The US dollar has been among the best-performing assets so far this year (up to May 2022), with the euro down -7.2% and the yen down over -11.9% (both compared to the US dollar).

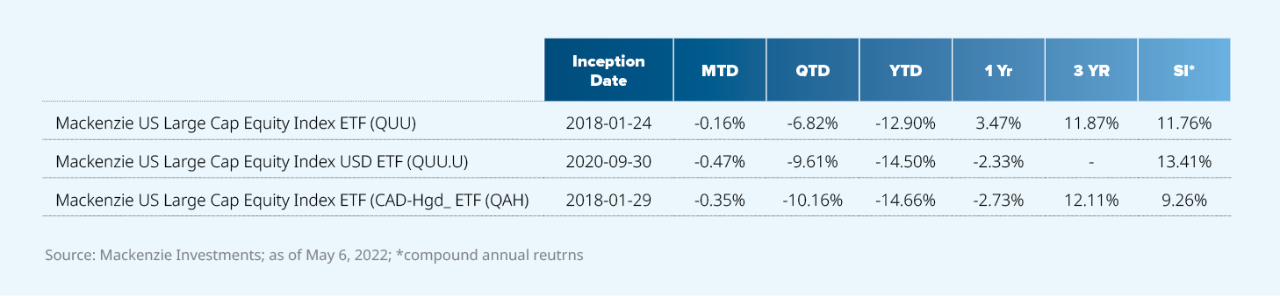

The Canadian dollar has done comparatively well but is still down -1.8%.3 As a result of this, year-to-date, QAH, the Mackenzie US Large Cap Equity Index ETF (CAD-Hedged) has underperformed the unhedged QUU, the Mackenzie US Large Cap Equity Index ETF (see below):

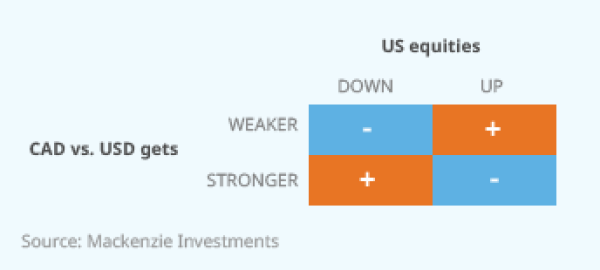

This is consistent with other periods where market volatility has typically been accompanied by US dollar strength. Conversely, the Canadian dollar has often been positively correlated to world stock markets, making Canadian dollar-hedged US equity ETFs typically more pro-cyclical (meaning that they perform better during periods of economic expansion).

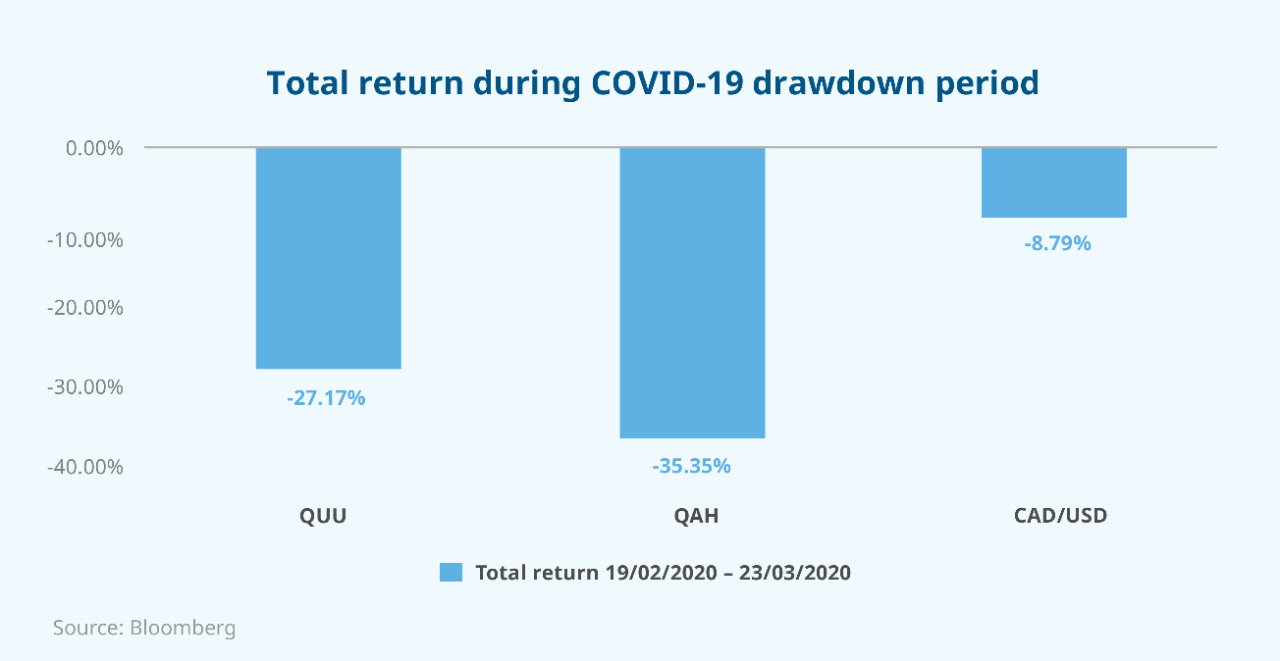

For instance, QAH similarly underperformed the unhedged QUU in March of 2020, as the US dollar dramatically strengthened during that period.

Should I use a CAD-hedged US equity ETF?

Long-term exposure to unhedged US equity ETFs may help lower portfolio volatility, as the US dollar has historically been less pro-cyclical than the Canadian dollar. However, this will ultimately depend on asset allocation. Therefore, a blended approach of Canadian dollar-hedged and unhedged US equity exposure could be an optimal solution.

Investors looking to maintain their exposure to US equities, but who are concerned about a depreciating US dollar, may want to consider QAH, the Mackenzie US Large Cap Equity Index ETF (CAD-Hedged).

Canadian investors holding US dollars may want to consider QUU.U, the Mackenzie US Large Cap Equity Index ETF.

To find out more about Canadian-hedged US ETFs, investors, please speak to your advisor; advisors, please contact your Mackenzie Sales Team.

Source:

1 Bloomberg, as of May 10, 2022.

2 Bank of Canada, as of May 24, 2022.

3 Bloomberg, as of May 6, 2022.

Commissions, management fees, brokerage fees and expenses all may be associated with Exchange Traded Funds. Please read the prospectus before investing. Exchange Traded Funds are not guaranteed, their values change frequently and past performance may not be repeated. The content of this article (including facts, views, opinions, recommendations, descriptions of or references to, products or securities) is not to be used or construed as investment advice, as an offer to sell or the solicitation of an offer to buy, or an endorsement, recommendation or sponsorship of any entity or security cited. Although we endeavour to ensure its accuracy and completeness, we assume no responsibility for any reliance upon it.

This document may contain forward-looking information which reflect our or third party current expectations or forecasts of future events. Forward-looking information is inherently subject to, among other things, risks, uncertainties and assumptions that could cause actual results to differ materially from those expressed herein. These risks, uncertainties and assumptions include, without limitation, general economic, political and market factors, interest and foreign exchange rates, the volatility of equity and capital markets, business competition, technological change, changes in government regulations, changes in tax laws, unexpected judicial or regulatory proceedings and catastrophic events. Please consider these and other factors carefully and not place undue reliance on forward-looking information. The forward-looking information contained herein is current only as of May 31, 2022. There should be no expectation that such information will in all circumstances be updated, supplemented or revised whether as a result of new information, changing circumstances, future events or otherwise.