Highlights

- The US government’s deep pockets were the main force behind the US economy’s blockbuster performance last year and should again save the country from a recession in 2024.

- The federal government is running massive deficits as the economy is overheating. That won’t change over the next few years.

- Washington can keep borrowing at its current pace for a long time. It won’t hit a brick wall, but that doesn’t mean its spending habits are innocuous.

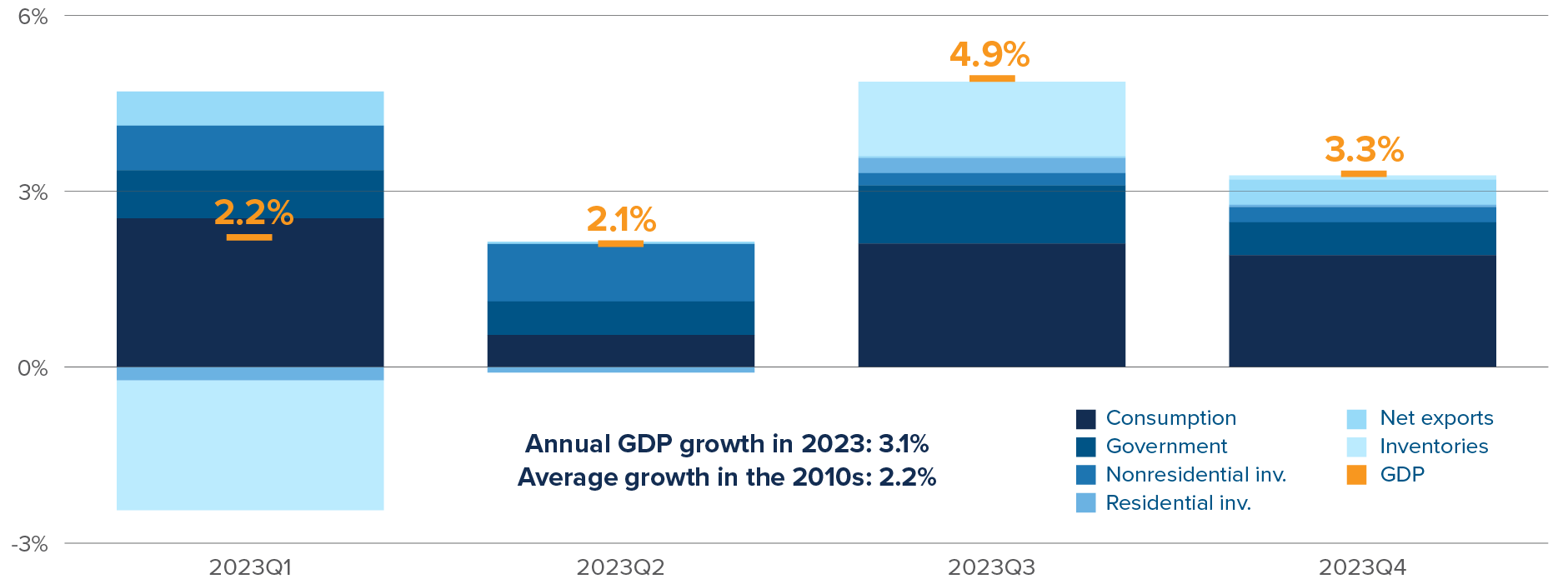

Most analysts misfired on their forecasts for the US economy last year. The widely announced recession never came. Far from sliding into a recession in 2023, the US economy grew at a solid pace. US gross domestic product (GDP) grew 3.1% last year, well above its 2.2% average growth in the 2010s, a decade coinciding with the longest uninterrupted economic expansion in history. We estimate that the average rate at which US GDP can expand in the long run — known as “potential growth” in economists’ jargon — is around 1.8%. We usually see above-potential growth in recoveries following recessions, not in a year that was “supposed” to mark the onset of a downturn.

What recession? The US economy experienced balanced growth in 2023

Contributions to US GDP growth

These recession forecasts didn’t pan out because the average analyst paid too little attention to a chief driver of short-term economic growth: government spending. Public authorities have two major tools with which they can affect the business cycle. First, the central bank — the Federal Reserve (Fed) in the US — controls monetary policy, which mostly consists of setting interest rates. Markets and analysts spend plenty of time analyzing Fed actions in minute detail. But they tend to overlook the second tool, fiscal policy, which can be just as pivotal for the economy. The government implements a loose fiscal policy by borrowing money that it channels — directly or indirectly — to consumers or businesses. All else equal, a larger deficit boosts short-term growth, while a tighter budget works to cool the economy. For the past few years, the US government has been borrowing and spending, fanning the flames of a hot US economy. In 2023, tax credits and loan forgiveness supported consumer spending, while industrial policies stimulated business investment, especially in the manufacturing sector.

Spending on factory construction doubled with subsidies from the Inflation Reduction Act

Manufacturing structures construction, inflation-adjusted

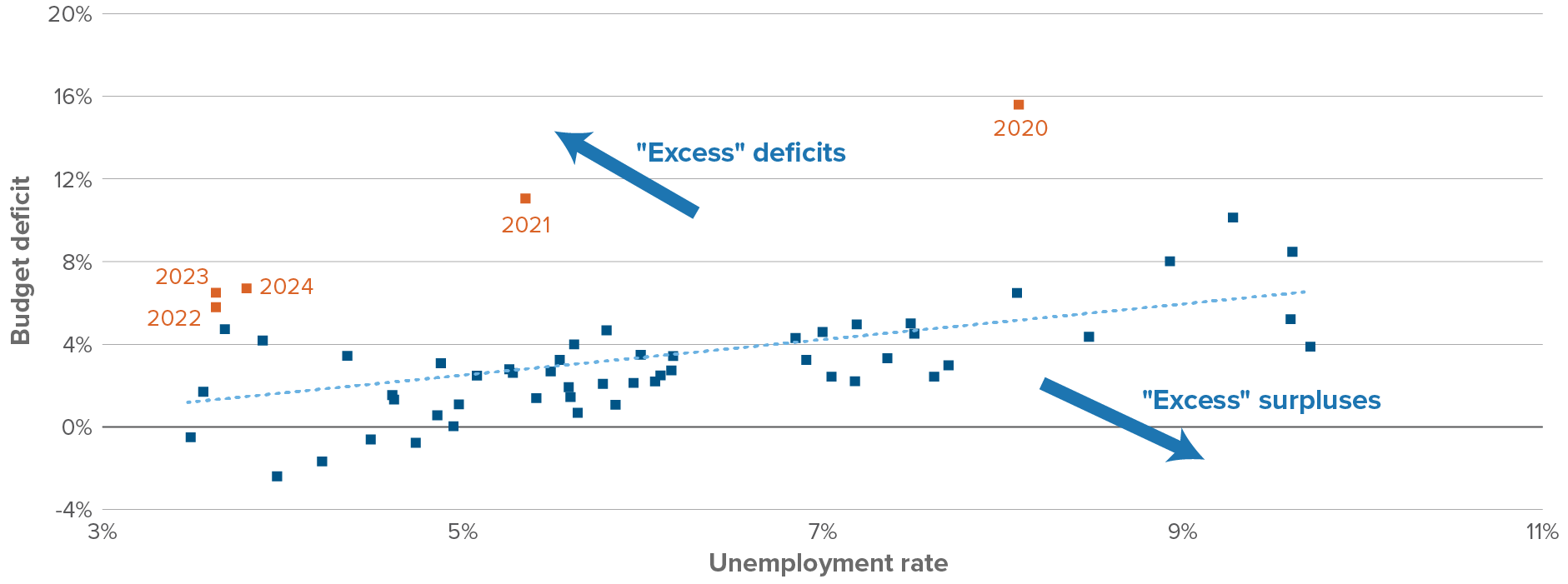

The US federal government ran a deficit of 6.5% of GDP in 2023. Pre-2020, we’d see the government run comparable deficits when it needed to stimulate the country out of a recession. Today’s economic backdrop is very different. The chart below highlights how unorthodox fiscal policy has been in recent years. We’ve seen serial deficits alongside a booming US economy with a sub-4% unemployment rate.

Massive deficits used to be the exception. Now they’re the norm.

US government calendar-year budget deficit vs. US unemployment rate

As explained in last month’s Emerging theme (“Be careful betting against the US economy”), we expect the US to once again avoid a recession in 2024. Those same forces that bolstered the US economy last year haven’t faded, especially the loose fiscal policy of the Biden administration. We expect the federal government to run a 6.7% deficit in calendar 2024, juicing growth and keeping inflation above 3%. Prior to 2020, the last time we saw such a large deficit was in 2012, when the US unemployment rate was around 9%. We expect it to stay below 4% in 2024.

Net interest payments on government bonds will probably account for half of the government’s net deficit in 2024. Interest payments don’t contribute as directly to short-term growth and inflation as primary deficits. Their likely recipients — savers — typically spend a lower proportion of their income than the average American consumer or business. But if the government doesn’t react to rising Fed rates by tightening its budget to keep overall deficits constant, the resulting higher payments to bondholders could somewhat counteract the Fed’s actions by juicing private spending.

How long can the US government keep spending borrowed money like this? The Congressional Budget Office expects the US federal deficit to stay above 5% for the foreseeable future. In our view, deficits will stay at elevated levels for at least the next Presidential term, as neither Biden nor Trump would act to tighten the budget.

Mandatory spending and net interest payments

US government deficit by fiscal year

The US government’s deficit-financed spending won’t cause it to hit a brick wall. Because it issues debt in its own currency, there’s no hard limit on its borrowing. Essentially, it can borrow forever, but it can’t borrow forever without consequences. We don’t have to wait decades for the repercussions of excess spending to show up. We’ve already experienced those effects in recent years: high inflation, surging interest rates, and the resulting degradation in Americans’ confidence in their government. The 20% growth in US consumer prices over the past few years is a direct result of that government borrowing and spending.

Elevated US government deficits and an unstable debt path are part of the reason we don’t love long-term Treasury bonds, and remain short bonds in the Mackenzie Global Macro Fund. Three things can happen to stabilize a government’s debt burden following a string of large deficits: a switch to primary budget surpluses in the future, faster economic growth or higher inflation. The first outcome would be positive for long-term bonds, the latter two negative. Over the next few years, we think a mix of solid growth and above-target inflation is a more likely scenario than the US government embarking on a 1990s-style crusade to balance the budget. Political trends reverse quickly, but it sure looks like deficit-fuelled growth is on the agenda for the next few years, regardless of who occupies the Oval Office.

Capital markets update

What we’ll be watching in March

March 19: Canadian CPI for January

- January CPI inflation came in well below consensus expectations (2.9% vs. 3.3% expected). The disinflationary surprise was seemingly not due to seasonal quirks, in contrast to the unreliable January CPI print in the US.

- With the various three-month annualized core inflation measures currently in a range between 2.4% and 3.3%, a tame print for February should bring all measures below the Bank of Canada’s 3% tolerance band, opening the door for a rate cut in April.

March 20: Federal Reserve rate decision

- Hard to believe that barely two months ago markets were pricing in a Fed rate cut in March.

- The economy is still humming along, and, even if the hot January CPI print might be due to seasonal adjustment quirks, inflation is still sticking well above the Fed’s 2% target. Tough to see the Fed cutting rates in the first half of 2024.

Emerging theme: A slightly disappointing GDP report for Canada

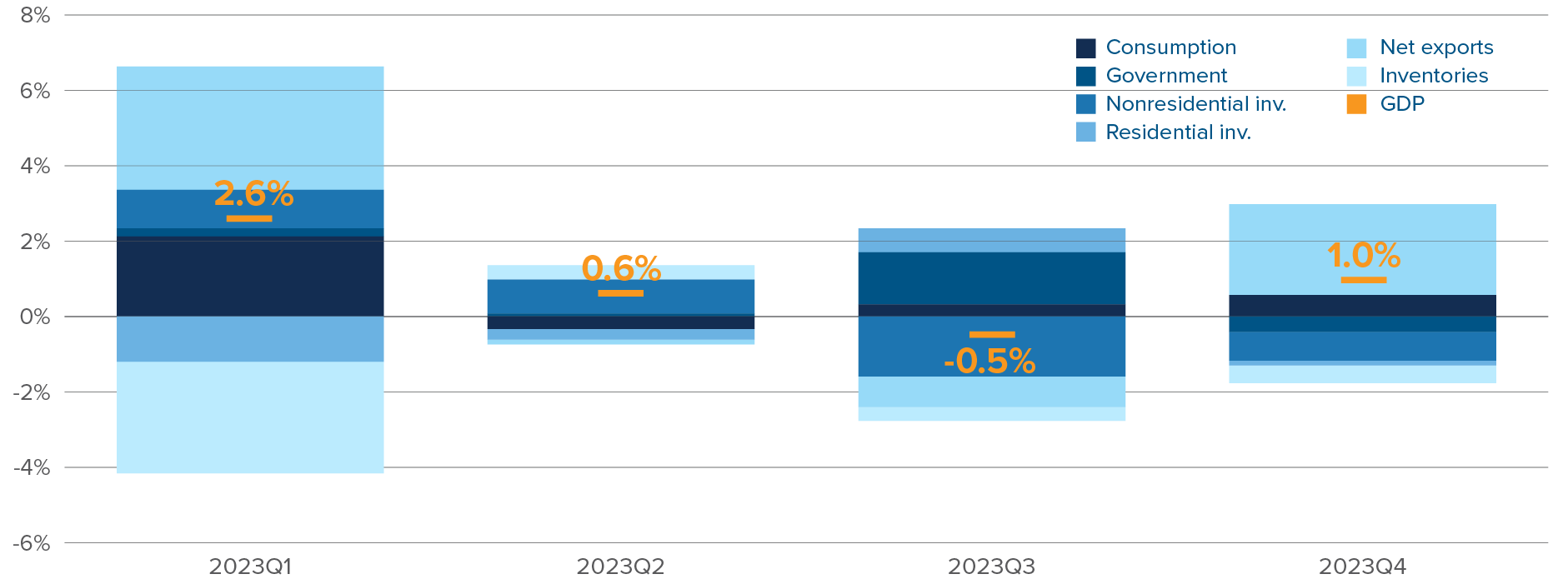

The recently released Canadian GDP data for Q4 sends mixed signals about the economy’s health and the Bank of Canada’s next actions. There is some good news. The print itself (+1.0%) is a bit higher than was expected by the average economist (+0.8%). And it keeps us solidly out of “technical recession” territory. Plus, consumer spending bounced from a dreadful third quarter, a welcome sight.

But the increase in consumer spending is coming solely from spending on durables, interest-sensitive purchases on which consumers are “catching up” now that the Bank of Canada has finished hiking. More broad-based strength in consumption would’ve been a stronger signal of a stabilization of the economy. The other positive surprise was a bounce in exports, which likely has much to do with slumping commodity prices and a delayed rebound from this summer’s wildfires, and little with the underlying strength of the Canadian economy.

The canary in the coal mine is business investment, which contracted for the second quarter in a row. Some will probably use the data to tell a story about the lack of long-term dynamism of the Canadian economy, but weak Q4 investment is mainly a short-term story about an economy that is slowing down quickly after large interest hikes and the ramping down of government largesse. With public spending set to stagnate over the coming year (unless we get a big surprise in the upcoming federal budget), it feels like the only thing that can jumpstart the economy is a few rate cuts.

In last month’s commentary we explained why we expected to see a first Bank of Canada rate cut in April. Since then, we’ve seen a low inflation print and a slightly disappointing GDP print. That has only increased our conviction towards an April cut.

Rebound in exports saves Canada from a technical recession

Source: Statistics Canada, as of 2023 Q4. Shows the contribution of gross domestic product (GDP) components to annualized quarterly GDP growth. By construction, there is a statistical discrepancy between GDP growth and the component contributions.

Source: Statistics Canada, as of 2023 Q4. Shows the contribution of gross domestic product (GDP) components to annualized quarterly GDP growth. By construction, there is a statistical discrepancy between GDP growth and the component contributions.

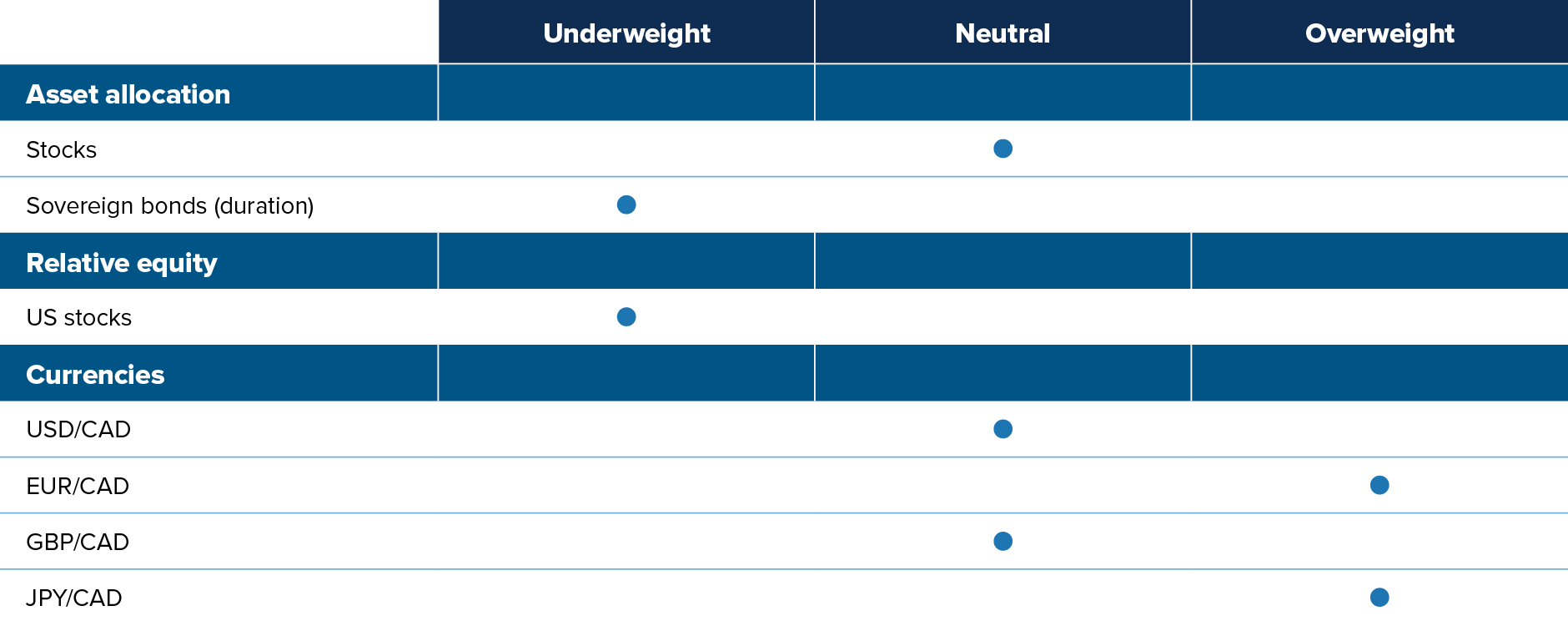

Multi-Asset Strategies Team’s investment views

Tactical summary

Note: The views expressed in this piece apply to products that are actively managed by the Multi-Asset Strategies Team.

Positioning highlights

Fed pricing reversal: At the start of the year, markets were expecting six Fed rate cuts in 2024. That was a stretch in our view, given the hot economy and the “transitory” forces behind recent disinflation. After upside surprises in economic releases, markets trimmed those expectations down to five cuts at the end of January, and now down to four cuts. This is more reasonable, but we'll still take the under. While the disinflationary trend is clear, we don't see inflation stabilizing at 2% over the next few months. We also think the Fed will err towards keeping rates tighter than what a classic monetary policy rule would suggest. FOMC members understand that the recent market action suggests financial conditions have loosened significantly in recent weeks, in effect substituting for rate cuts.

Overvalued US assets: We generally don’t like US assets, whether equities, bonds or the US dollar. Within US equity markets, we prefer small-cap stocks: valuations are more attractive than large caps, and market sentiment is improving quickly. In terms of sectors, we like health care (pricing power in inflationary environment, bullish trends) and dislike utilities (declining profitability, poor macro backdrop).

Canadian landing: The macro situation in Canada appears much more dire than in the US. Data has already started turning. The Sahm Rule, which uses changes in the unemployment rate to date recessions, is flashing red. We dislike the Canadian dollar against most currencies.

Commodity-exporting EM currencies: Commodity-exporting EMs are well situated to outperform in this macro environment. Their budgetary and external balances have improved amid high global nominal growth and high commodity prices. Their central banks started raising rates much earlier than the rest of the world. As a result, they have generally reached the end of their tightening cycle, reducing the risk of overtightening into a recession. But the level of rates remains high, offering positive carry over most other currencies. On the other hand, we hold a negative view on the currencies of Asian EM countries. Their external positions have severely deteriorated, and their interest rates are relatively low.

Oil market tightness: The physical oil market is tight, especially with the ongoing one-million-barrel-per-day Saudi production cut and upcoming refill program for the US Strategic Petroleum Reserve. In the absence of a global recession, which we don’t expect to occur any time soon given the positive momentum in the US and the expansionary deficits from governments around the world, oil should remain undersupplied. A stabilization of the Chinese economy will trim risks around oil demand. Positioning is also constructive for the oil complex. For much of 2023, investors were expressing recession bets through short oil derivatives positions. These bets have been coming off, with room to run.

Japan policy divergence: The BoJ widened the tolerance band around its 10-year yield target by 25bps back in December 2022, and by an additional 50bps in July 2023, before adding flexibility around the band in October. With the yen still undervalued and core inflation sticking above 2%, the BoJ will likely tighten further in 2024. We expect the BoJ to finally abandon its negative rate policy in April. We are short Japanese government bonds in our Global Macro Fund. We also have a long position in the Japanese yen (versus both the euro and the US dollar) to take advantage of Japan policy normalization and the yen’s undervaluation. We like long JPY/EUR because the yen is more undervalued than the euro, and the ECB has overtightened.

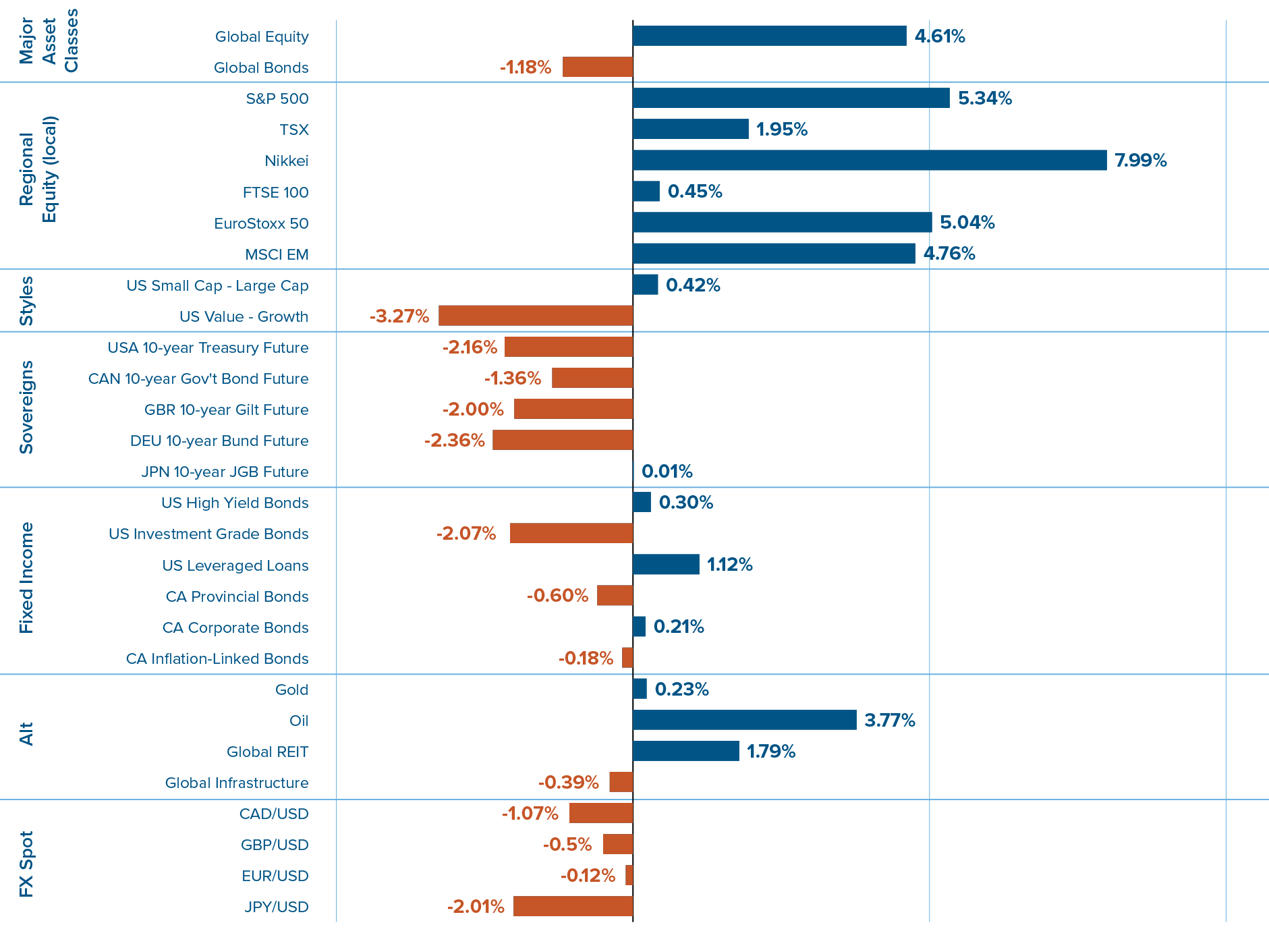

Capital market returns in February